Bonds were about the only place to hide last week as most world equity markets declined meaningfully, especially emerging markets, in addition to commodity markets. Although the bulk of U.S. economic news was positive, the negative first-quarter GDP report frightened investors on Friday, hitting any sector that depends on a healthy world growth rate. Conversely, bonds, which do better in a weak economic environment, showed healthy gains.

Emerging markets were down almost 4% for the week as Chinese brokerage firms imposed higher margin requirements. That drove the Shanghai index down by over 6% on Thursday, which had knock-on effects on other emerging markets. The decline in emerging markets was far worse than the 1%-2% declines in most world equity markets and a 1.6% decline in commodity markets. On-again off-again debt negotiations between Greece and the EU seemed to move stocks around a lot during a week without a lot of other news. Heavy merger activity continued this week with  Broadcom (BRCM) the biggest target. This activity did little to get markets very excited, though.

Broadcom (BRCM) the biggest target. This activity did little to get markets very excited, though.

In economic news, investors were mainly worried about the first-quarter U.S. GDP revision showing negative 0.7% growth. Weather, port strikes and a shifting energy market made a modestly slowing economy look worse than it really was. Second-quarter growth should look more like 2.5%-3%, as consumers rebound and net exports weigh less heavily on the data.

Secondarily, growth investors fretted over a Chicago Purchasing Managers report that showed continued declines and was below the level that separates growth from contraction. We have basically given up on the regional reports because they have proven to be volatile, contradictory and bearing little resemblance to the national reports. Still, it's not good news for the U.S. economy.

On the other hand, the durable goods report this week contradicted the Chicago report and seemed to suggest that maybe the worst was over for the manufacturing economy. The housing news was surprisingly good and uniform with new home sales, pending existing-home sales and home prices all showing meaningful growth.

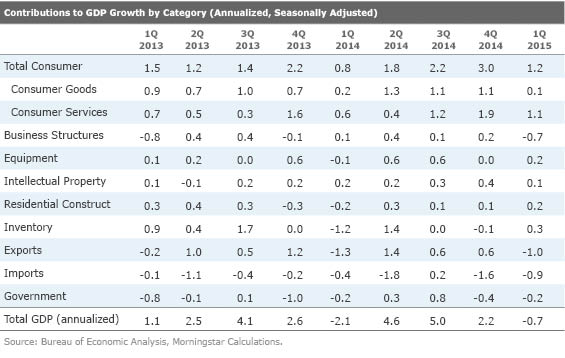

First-quarter GDP down; no surprise to our readers

As widely expected, the first-quarter GDP growth rate was reduced from a measly 0.2% to an outright decline of 0.7% on Friday. As bad as the revision seemed, it was widely anticipated and could be easily predicted by looking at recently released data revisions.

In fact, the official decline was modestly better than the consensus forecast of a 1% contraction. Even Federal Reserve Chairwoman Janet Yellen alluded to the fact in recent speeches that a first-quarter GDP revision to a loss from a gain was a possibility.

Besides the usual small and offsetting revisions, the really large revisions were relatively equally divided between a higher-than-expected estimated surge in imports and a reduction in the inventory buildup that was smaller than originally reported. (The "P" in GDP, production, is not measured directly. Instead, the government counts sales and adds the changes in inventories. More inventory than sales means that production was higher than sales.) Conversely, foreign goods that were not produced in the United States end up in retail stores; therefore, they have to be subtracted from GDP.

The revisions were not really a game-changer with the broad contours of the report little changed from the previous one. If anything, we were more pleased with the report versus the previous ones because we despise seeing a huge contribution from inventories, which means production may have been excessive relative to sales levels. In a weak sales environment, it likely means a reduction in production in subsequent quarters, depressing future GDP reports. So GDP gains from inventories are often a pyrrhic victory, boosting short-term GDP at the expense of future quarters. Over the course of a full year, not just one quarter, the inventory contribution changes little and is relatively close to zero.

Likewise, huge import changes in one quarter tend to be self-correcting over the course of a full year, with a big quarter often followed by small ones. However, in a recovery, imports will trend upward and will hurt the full-year GDP calculation, unlike full-year inventory adjustments, which tend to be relatively small and trendless.

The key takeaways for the quarter are unchanged. Consumers continued to be the key driver of the economy, net exports were a huge detractor as was a rapidly declining oil sector (fewer oil wells show up in the business structures category). Most other categories didn't change enough to make a big difference. Somewhat surprisingly, government spending continued to decline.

Although consumers remained the biggest contributor, that growth rate was more than cut in half between the first and second quarter. Weather weighed on consumers' ability to spend, though I confess that the slowdown was rather broad-based. In the weather-affected category, restaurants, hotels, clothing and autos were some of the harder-hit sectors. Still, health-care, groceries and the other categories weren't so hot, either. Nevertheless, better weather is already helping some categories (autos and restaurants in April), and should bode well for a better consumption number in the June quarter.

Exports were influenced by lower growth in energy-related products as well as a general malaise due to a strong dollar, weak world growth and lack of interest in anything broadly related to the production of commodities. The West Coast port strike certainly didn't help exports, but the bigger impact was on imports. Imports that had been cruising the Pacific Ocean emptied their cargo bays en masse in March, artificially inflating imports. Although the exact timing of when those imports completely clear the harbours is unknown, surely imports will take at least a one-month dive in the near future. That import dip will turn into a huge benefit for the GDP calculation at some point.

We are holding firm for a 2.0%-2.5% growth rate for the full year. That implies that growth over the next three quarters will average around 3%. With a stronger world economy and a more well-off consumer (due to labour scarcity and wage gains), growth next year could accelerate modestly to 2.25%-2.75%. Demographics will keep a lid on many spending categories but may help the housing market slightly.

The housing market finally catches a break

For a big change, all of the housing data this week showed a housing market that is accelerating across the board. Home price data, pending sales of existing homes and new home sales all showed surprising strength and generally exceeded analysts' expectations.

Before we discuss these individual reports, we want to remind readers that an improving housing market is the linchpin to the economy maintaining its 2.0%-2.5% growth rate in 2015, even in the face of a decline in real GDP in the first quarter. A 3% direct impact on GDP may seem small, but if the sector can manage 15% overall growth, that would amount to a 0.5% contribution to GDP. While that may not sound like a lot, a 0.5% contribution in a world of 2.0%-2.5% growth is a big deal. (Housing's contribution in 2014 was a mere 0.1%.)

In addition, besides the direct effect on builders, real estate brokers and remodelers, there are knock-on effects from real estate in the furniture, appliance, mortgage broker and landscaper industries that should follow the housing market up with a three- to six-month lag. The housing market has the potential to help offset some of the weakness in the manufacturing sector and keep it from performing even more poorly. Recall that manufacturing had a banner year in 2014 and is now suffering from a weaker export market and a falloff in energy-related manufacturing.

Demographics finally moving in the right direction for new homes

In last week's column, we noted that the market for apartments was nearly back to normal while single-family home sales were still about two thirds below their previous highs. A lot of readers correctly noted that consumer preferences and diminished finances have pushed more consumers into apartments. They further noted that this trend might not reverse itself. That wouldn't be the greatest news for the economy, since single-family home construction generates more jobs and economic activity than an apartment unit.

I share some of those concerns but also note that demographics have played a role in surging apartment demand, hurting new single-family home sales. Some of that is about to reverse itself. The table below shows a surge over the last several years in young people who are between 24 and 31, a prime age category for apartment living. That surge in potential renters could be behind the relatively strong demand for more rental units. However, over the next several years that pool begins to grow more slowly and by 2019 actually shrinks.

Meanwhile, the number of people turning 31 in any given year has been slowly improving, which should begin to drive increased single-family home activity.

New home sales are beginning to reflect improved demographics

The new home sales report for April seems to be reflecting some of those demographic improvements.

Headline figures showed new home sales jumped 6.8% month to month to 517,000 annualized units. The strong results come despite a massive seasonal adjustment factor that provided a huge headwind (there were more than 588,000 annualized units sold in April without the seasonal factor). That is the third month out of the past four with sales of over 500,000, and the fourth month was close at 484,000 units. For all of 2014, units sales averaged 437,000 units per month.

Part of April's strong rebound was a large, most likely weather-related bounce in the Midwest. Still, it is not all about the weather when we look at year-over-year averaged growth rates, as shown below. The trend has been outstanding with year-over-year averaged growth around 24%.

Stage of construction data explains why starts and permits aren't as strong

The new home sales report provides some interesting insights on the housing market, showing whether buyers bought completely finished homes, homes that were started but not finished, or homes that were finished, waiting for a buyer. Each is approximately equal at the moment, with about 170,000 homes purchased in each category. For the single month of April, buyers were interested in either homes that were finished and available for immediate move-in or ones that were still on the drawing board. Those homes still on the drawing board should provide fuel for the starts and permits reports in the months ahead. This also explains why starts and permits growth for single-family homes have been less robust than new home sales (for April, single-family permit growth was just 11% versus 26% new home sales growth).

Pending existing-home sales rebound

At a reading of 112.4, the pending home sales level is higher than any time back to 2006.

Although the deterioration that was occurring in 2006 would tend to make the numbers difficult to compare, it's still fascinating that existing-home sales were running at over 6 million units versus just 5.2 million currently, suggesting a lot of upside to the existing-homes figure, if the current level can be sustained.

Month to month the index is up 3.4% on a single-month basis, and 14% year over year. The strong pending report also takes away some of the sting of last month's relatively poor existing-homes data, which was reported last week and seems to indicate a big jump in existing-home sales is possible and/or revisions to previous months are likely. The year-over-year averaged trends also look quite good.

The pendings data suggest that May and June existing-home sales should be at least as good as in April. That implies some really nice improvement in existing-home unit sales for the second quarter. That in turn implies a huge potential upgrading of the brokerage commissions component to the GDP calculation. In the government's annualization of quarterly numbers, commissions could grow well over 30% first quarter to second quarter. That would follow two quarters in a row when brokerage commissions fell quarter to quarter and were a net subtraction from the GDP calculation.

Home prices reflect rebounding housing market (by Roland Czerniawski)

Prices of existing homes continued to increase as all three indexes we track posted positive gains in March. On a year-over-year, three-month average methodology, the pace of price increases stayed at a similar level compared with February. On that basis, the price growth ranged from 5.0% to 5.2% among FHFA, Case-Shiller and CoreLogic (CLGX) in March. That is a meaningful pickup from the much slower sub-5.0% growth rate recorded in fourth quarter 2014.

One of the reasons behind the increase in price growth is accelerated demand, which has now been reinforced by strong data released in new, existing, and pending home sales reports over the past two weeks. The worries caused by low inventory levels have now begun to ease too, as the number of available homes picked up just a notch despite the greatly improved sales figures. We expect year-over-year home prices to grow 5%to 6% this year, a rate that would support an accelerating housing market, without causing a severe dent in affordability.

Manufacturing pokes its head up

The manufacturing sector is more important than many people realize and has been one of the most important contributors to this economic recovery. Manufacturing accounts for about 10% of all private employment and 12% of all wages. The hours worked and average hourly wage are both substantially higher than in many other sectors. And because of outsize volatility, its impact on the economy is even greater than these numbers suggest.

The manufacturing sector had a great year in 2014, at least until the fall, when things began to fray at the seams. Industrial production growth that almost reached 5% in late 2014 has now slowed to just 3%. The good news is that it's still above the long-term average of 2.6%, but the month-to-month data was even more worrisome, showing several months of outright declines.

However, we may have turned the corner. Manufacturing industrial production has been up for two months in a row, and the ISM Purchasing Manager Index has stopped going down.

This week's report on durable goods provided some additional positive news. New orders for durable goods increased 0.5% after growing a very healthy 0.6% the prior month. When averaged over three months, the growth rates in the month-to-month data are still negative but trending in the right direction.

Because these goods typically have longer lead times, the outright growth in the single-month order growth rate and an improving trend in the averaged month-to-month data bode well for industrial production and manufacturing employment in the months ahead. Still, the year-over-year numbers are eroding a bit, weighed down by a period of poor growth from November to January. I am less worried about that given that the month-to-month numbers are looking better and the United States will lap a string of great numbers (due to a weather-related bounce and not fundamentals) from 2014 by midsummer. So things are looking a little better currently and the decline has been halted for now. However, getting back to 5%-type growth rates for industrial production looks improbable.

![]()

Consumption, autos, trade and employment lead a busy week of economic data

We will get a lot of economic data next week, but it won't likely shed much light on where the economy really is. Some reports will be quite stale and others will be quirky enough to question their usefulness.

On the stale side, the consumption report is likely to show a very modest growth rate of 0.2% for April compared with a better 0.4% increase in March. But a lot of that deceleration is due to poor auto sales in April that are likely to come back sharply in May. Deflation in a couple of key categories (clothing and groceries) could help the inflation-adjusted consumption figures from being even worse.

Auto sales are expected to rebound sharply to 17.1 million units, up from an anemic 16.5 million units in April. Most of the industry trade rags are expecting even better news, estimating unit sales of as much as 17.3 million units on a seasonally adjusted annual rate basis. That seasonal factor could provide a bit of a tailwind to the report as whatever the sales report shows will be boosted by 5% to factor in one less selling day. Given Internet sales and more auto dealerships open on Sundays and holidays, this adjustment seem a bit dubious to us.

The trade data absolutely killed the GDP report for the first quarter, and we suspect that April may erase some of those terrible deficits as the import glut finally cleared the docks. The key issue is, in which month did those imports clear the docks? March, April--or not yet? The assumption seems to be that most of the clean-out happened in March, and that April should show a large reduction in imports. The consensus is for the deficit to fall from US$51.4 billion to just US$43 billion. If sustained, that would be great news for the second-quarter GDP report.

The estimates I have seen for the U.S. employment report for May are in a much wider range than I have seen in some time. The April report was 223,000 jobs added, and I have seen May estimates as high as 288,000 but also below 200,000. I can't really see much support for the high end, other than we have been weak for several months and could revert to the mean. Stable initial unemployment claims and some poor data from the purchasing managers' reports would seem to favour a report of flat to slightly down employment. My talks with companies seem to suggest that hiring might have hit a wall in May, but that is an incredibly small sample set. Still, I am going with a forecast of 200,000 for the month.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/54RIEB5NTVG73FNGCTH6TGQMWU.png)