Two Dividend Stock Picks for 2023

Bristol Gates' Achilleas Taxildaris likes two dividend growers - one from Canada, and one from the U.S.

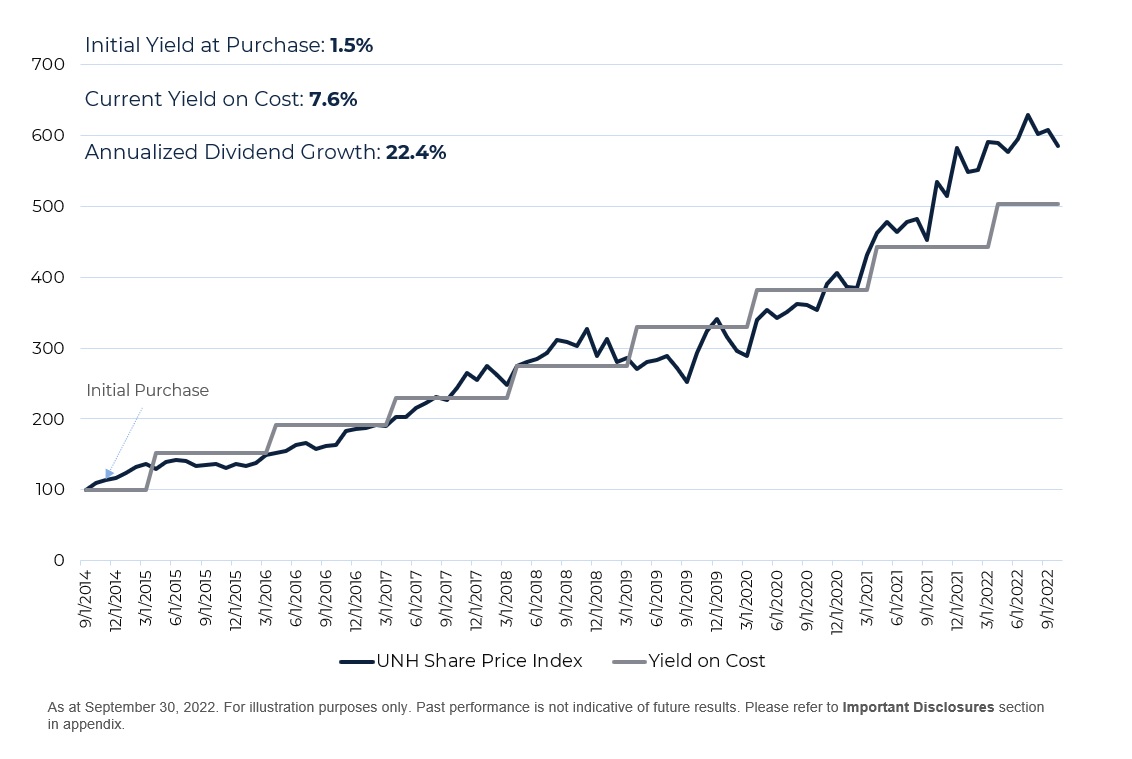

Ruth Saldanha: Dividends are a hot favorite for Canadian investors. And to start off 2023, we have a couple of ideas from Bristol Gate. The firm focuses on dividend growth, not yield, and portfolio manager, Achilleas Taxildaris, is here to tell us why and to highlight two companies that he likes. Achilleas, thank you so much for being here today. Achilleas Taxildaris: Thank you for having me. We Prefer Dividend Growth Over High Dividend Yields Saldanha: To start with, why do you like dividend growth over yield? Taxildaris: Yes, there's a lot of empirical evidence that have demonstrated that dividend-growing companies collectively outperform over the long term. Why is that? We believe the reason is that dividend growth can be a proxy for the rate which these companies can grow their true earnings. So, the key there is to have sustainable dividend growth that is supported by the fundamentals of the companies. So, we try to avoid low to no growth and even worse, the dividend cuts. And typically, dividend growth strategies employ a minimum yield threshold. We don't have that, because that process tends to miss out on companies that may have lower absolute yield, but they're growing their dividend at fast rates. So, we are aiming to achieve a high yield on cost. So, our core belief is that if you can build a concentrated yet well balanced portfolio of high-quality, high dividend growing companies and you pay a fair price for them, you're setting your odds for success in your favor. Bristol Gate is Not Worried About Dividend Cuts in 2023 Saldanha: Well, you mentioned dividend cuts. How worried are you about dividend cuts in 2023? Taxildaris: By focusing on high dividend growth companies, we tend to avoid most instances of dividend cuts regardless of the macroeconomic backdrop. And even in an environment where there might be many dividend cuts, a small dividend growth is still relatively attractive. The fast dividend growers that we typically look after, they tend to have pristine balance sheets. So, we have a filter that only looks at investment grade rated balance sheets. They generate a lot of free cash flow. And they tend to have low payout ratios. So, these characteristics in combination sealed us in the past from having any dividend cuts in most environments, in most situations, with the exception of the pandemic-induced lockdowns that affected even temporarily some of our retail and travel-related companies. In terms of the 2023, our quantitative model is predicting a continuation of the trend that we saw in 2022 of declining dividend growth in our universe. But there's still a healthy breadth of dividend-growing companies overall. Dividend Stock Pick One: Intact Financial Saldanha: Well, you mentioned healthy growing dividend companies and there's two that you want to highlight today, one Canadian and one U.S.-based. Let's talk about the Canadian one first – Intact Financial (IFC). Why do you like this company? Taxildaris: Yes. So, Intact Financial is a leading property and casualty insurer in Canada that has also expanded internationally in the specialty business. We like it because management has a proven track record in growing the company through both organically and through M&A and have successfully managed to consolidate a good part of the Canadian property and casualty insurance market. Right now, they have a market share of over 20%. They are really good operators. They have constantly maintained ratios of about 90% – combined ratio in the low 90s, and they're also doing an excellent job on the investment management side of the business. So, that successful, let's say, performance have allowed them to gain scale that comes with additional competitive advantages. So, now, they have the ability to diversify both on geographies, businesses and different business lines and channels. They have the ability to leverage data throughout their business and help them underwrite better. And it also allows for some vertical integration. They own an in-house restoration service that helps to improve claims expertise but also improve the customer experience. It has done pretty well from a valuation standpoint. It significantly outperformed the TSX in 2022. It trades at a premium to its historical value. From a price to book value, it's now around 2.5 times whereas historical average is about 2.2, let's say. And it also trades at a premium versus most of its peers, both in Canada and in the U.S. We think some of that premium is warranted given the high profitability and its growth profile. It has consistently returned numbers that are above the industry as a whole. And they recently did a major acquisition of a company that had both the Canadian presence and the U.K., and we believe once they show a bit of progress on the integration side, that will unlock some value that perhaps may not be priced in yet. Dividend Stock Pick Two: UnitedHealth Group Saldanha: The other stock that you like is in the U.S., and this one is also trading at a bit of a premium. That one is UnitedHealthcare Group (UNH). Can you tell us a little bit more about that? Taxildaris: Yes. UnitedHealth is a very big company. Its market cap is close to 0.5 trillion and yet still manages to grow at double-digit rates. So, they are a large vertically-integrated healthcare provider in the U.S. And it's one of the rare success stories of diversification via vertical integration. They leverage their leading position in the insurance and benefits business to get into services in terms of healthcare services such as physicians, ambulatory services, and pharmacy benefits, and so on. And couple that with a very profitable and fast-growing segment that's centered around data and insights that is being used both internally to improve the operations of the company, but also consulting on government and hospitals in the U.S. So, it has significant competitive advantages. Some of it is via its scale and through networking effect. It touches a lot of the healthcare system in the U.S. and that allows them to utilize their position and harness this data and use it as a competitive differentiator, particularly in a value-based care context. So, the U.S. healthcare is a massive market. We're talking about 18% of the U.S. GDP, and that's about twice the size or the percentage of the GDP in the EU. So, it's not just big, it's also inefficient. So, there's a lot of effort to try to improve that, and one of it is the trend towards value-based care. And that's a significant opportunity the way UnitedHealth is set up to take advantage and continue expanding its market share. As a context, value-based care is a risk-based model that healthcare providers are incentivized to provide the best care at the lowest possible cost and the best results. And it's much more preventative and compliance-based and that has proven over the long term to be more efficient but also improve the patients' outcome. On the insurance side, the industry has also become more rational on the pricing. In the past, peers have tried to increase their market share and got in trouble in the underwriting side. It has a lot of traditional competitive advantages or moat. So, it's really hard for new entrants to come into the market, the top players dominate the market and it's really hard for, let's say, Amazon to come in. It's a very sticky business. The retention rates are over 90%. So, once an employer adopts UnitedHealthcare health benefits, it's really hard to just decide to move on. So, they tend to retain clients over the long term. And a lot of peers have tried to copy United's vertical integration model by expanding in other healthcare services, but none have the head start that UnitedHealth has and the integration of the data and insights component that they have done in their business. So, again, it generates a lot of free cash flow, has a pristine balance sheet. And given the market size, it still has a runway to continue growing despite its massive size. There are some risks, of course. The biggest one might be regulatory. But given its size and scale and importance in the healthcare system as well as how it's well-positioned to help on the value-based care, they're going to be part of the solution no matter what the regulation will be. It's not a cheap name, of course, as you mentioned. It trades at a premium to the market, and it had a positive return in 2022 where the market was down by a lot. But at 6% free cash flow yield, it's still reasonably priced given both the growth profile and the profitability of the business. They've increased their dividend for over 10 years at rates over 20%. So, to go back on the yield on cost concept that we are looking for, we own UnitedHealth since 2014. Back then, it was having a dividend yield of about 1.5, so nothing significant. But because they were growing their dividend in that time period until, let's say, now, they've increased their dividend over 5 times, that's like over 20% or 22% annualized. So, today, the dividend yield is actually 1.3%. That's because the price managed to increase even faster than its dividend, and that's something we see when that dividend growth is actually supported by the fundamentals and is sustainable. So, our yield on initial cost is over 7.5% right now. So, that's the concept we believe in. If we can identify these companies and keep them in our portfolio, we believe we're setting up for success. Saldanha: Great. Thank you so much for joining us today with your perspectives, Achilleas. Taxildaris: Thank you for having me. Saldanha: For Morningstar, I'm Ruth Saldanha.

{kind=link}