Many North American households are behind when it comes to saving for retirement. And while it seems obvious that making more money could solve the problem, the reality is far messier: Raises--and how we spend them--can actually make it more difficult to retire comfortably. How? It comes down to three main factors:

1. Lifestyle creep

2. Fixed assets

3. Constant saving rates

The problem: Lifestyle creep and static existing assets

Most of us tend to increase our standard of living as our income increases: That’s to be expected. But that new standard of living translates into a new level of expenses, which stays with us over time. What starts off as a weekend splurge on dining out soon becomes a weekly affair. That nice place that once seemed out of reach is now your home--and the mortgage comes with it. That’s lifestyle creep.

With increased income, our retirement need increases proportionally--we’d like to maintain (at least part) of our new standard of living in retirement. And, if we maintain a constant savings rate, increased income also means increased savings. So, the good news is that we’re saving more money.

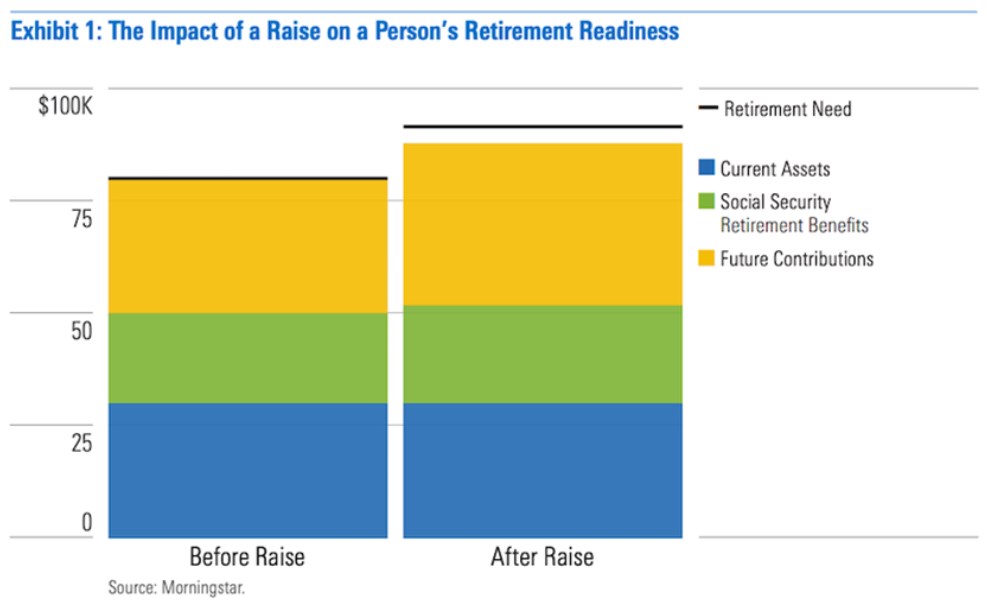

Exhibit 1 shows what happens for a 47 year old who received a big salary bump from $100,000 to $120,000 and saved a constant 11% of her salary. Although she had been on track to meet her retirement need before the raise, she is now falling behind.

Thankfully, this is fixable.

The solution: Save more. How much more depends on your personal characteristics

We wanted to determine how much of a raise a person needs to save in order to fund an equivalent raise in retirement. For example, if one’s current standard of living increases by $5,000 per year, how much is needed to fund a similar raise in retirement?

Using a nationally representative sample of American households from the 2016 Survey of Consumer Finances, we created a model to determine how much of a 5% raise a person should save to ensure his retirement income continues that lifestyle change. We used this model to test the effectiveness of three guidelines:

1. Spend twice your years to retirement. If you are going to retire in 15 years, spend 30% of your raise and save the remaining 70% for retirement.

2. Save your age as a percentage of the raise. If you are 50 years old, save 50% of the raise.

3. Save at least 33% of your raise. If your take-home income increased by $1,000, save $333 of that new income.

The “spend twice your years to retirement” rule has the highest success rate overall. However, it also requires the most saving and may be difficult for those with little discretionary income. On the other hand, both the “save your age” rule and “save at least 33%” rule are good for investors under 45, but they fall short as the person ages. Not surprisingly, older investors must save more than their raise to fund their new standard of living in retirement. Because they are closer to retirement, these investors have less time to accumulate savings and less time in the market to generate returns--the “spend twice your years to retirement” rule is up to the challenge; the others aren’t.

More money, more problems

The primary lesson from this research is clear: After celebrating your new income, think about how that higher income may impact your expectations in retirement and, thus, your financial plan. Most investors may need to increase their savings rate to avoid a drop in their standard of living in retirement. Although these guidelines are good starting points for investors, getting a raise is a perfect time to meet with a financial advisor or do a detailed analysis yourself, making the necessary changes to your financial plan based on our personal situation.

Are you getting the right returns?

Get our free equity indexes to benchmark your portfolio here