Editor's note: Read the latest on how the coronavirus is rattling the markets and what you can do to navigate it.

In this update of our COVID-19 research, we dive further into the United States' mitigation strategies on a monthly basis for the remainder of 2020. We also provide analysis of recent data for drug treatments and updates on the status of the most promising programs.

In our base-case scenario, we assume full implementation of aggressive social distancing measures (including closures of schools and nonessential businesses) through most of the second quarter. After that, we think these measures will recede along with the first wave of the outbreak. Secondary waves of the virus are likely in 2020, but they should be much less deadly, thanks largely to new drug treatments. The key driver of our bear-case scenario is inefficacy of new treatments. While a few countries like South Korea and Singapore appear to have brought the virus under control using aggressive but not economically destructive nonpharmaceutical methods, we believe this may be beyond the U.S.' ability.

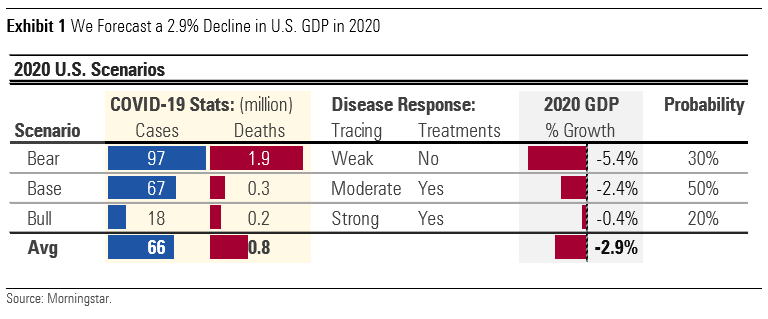

We now forecast U.S. real GDP growth of negative 2.9% in 2020 (after deducting a COVID-19 impact of 5%). For global GDP, we expect a decline of 1.4%, implying a recession on par with 2008-09. Our U.S. forecast is based on our detailed scenarios as we project the industry-level impact of mitigation strategies. We think the scope of shutdown orders to disrupt the U.S. economy is probably overrated, as large swaths of the U.S. economy are exempt from the orders. Meanwhile, historically large fiscal stimulus should prevent a collapse in the demand side of the economy.

Overall, we still expect a modest long-run economic impact, with GDP down 0.9%. This is much less than what is implied by the 20%-plus drop in global equities since February. In our view, a COVID-19 recession doesn't fit the mold of a 2008-style recession with longer-lasting economic impact.

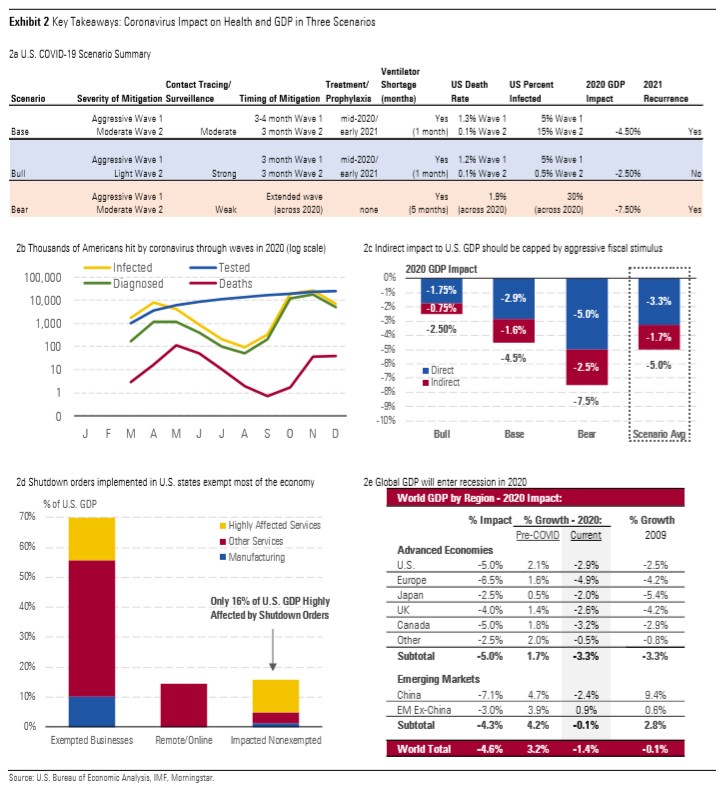

Epidemiology and Society's Response in Three Scenarios (Exhibit 2a)

In our base case, we assume that the first wave in the U.S. subsides by the end of May, after which many social distancing measures (such as closures of schools and nonessential businesses) can be eased due to the existence of at least one effective treatment.

We still assume 20% of the population is infected over the course of the year in our base case, with a slightly higher average death rate of 0.4% (up from 0.3% in our March 9 analysis) and a roughly 1% death rate during the first wave.

The relaxation of social distancing in our base case means that one or more additional wave is likely later in 2020. However, these secondary waves will see a much lower fatality rate (around 0.1%, on par with seasonal flu) thanks to new drug treatments plus quick diagnosis via prolific testing.

Our bull case (20% probability) is distinguished by a much lower infection rate, just 5% of the U.S. population. This accounts for the possibility that the U.S. successfully mimics the tactics used in South Korea and Singapore (massive testing and contact tracing) to halt the spread of the virus. In this scenario, most social distancing measures are lifted by the second quarter.

In our bear case (30% probability), we assume that current social distancing measures are only modestly effective, and development of new drug treatments is disappointing. This necessitates the maintenance of business closures and other stringent measures throughout most of 2020.

2020 GDP Impact, Industry Level Analysis, and Long-Run Impact

- We forecast a 5% impact to U.S. real GDP in 2020 from COVID-19, taking the probability-weighted average across our scenarios (Exhibit 2c). Deducting this from our pre-COVID expectation results in a forecast of a 2.9% decline in U.S. real GDP in 2020. This U.S. recession slightly exceeds what we saw in 2009, though it isn't unprecedented in the post-World War II era.

- Overall, we think the main driver of lower U.S. GDP will be the direct impact from COVID-19 on certain industries via business closures and voluntary social distancing.

- We expect the indirect impact to be substantial at 170 basis points of GDP, thanks to reduced spending power and economic confidence, but we don't think aggregate demand will collapse. Critically, the U.S. has passed historically large fiscal stimulus, eclipsing post-Great Recession or New Deal-era stimulus.

- Our analysis of U.S. GDP at the industry level suggests that even if stay-at-home/shutdown orders are implemented in all 50 states, no more than about 16% of GDP will be highly affected (Exhibit 2d). About 70% of GDP consists of businesses largely exempted from orders as implemented in most states. Among the remaining 30%, around half may be able to continue normal economic activity via remote operations.

- We use our detailed U.S. analysis as a benchmark for our updated global GDP estimates. We now forecast 460 basis points of impact to world GDP in 2020, yielding our updated forecast of negative 1.4% real GDP growth in 2020. We think Europe is likely to be hit somewhat harder than the U.S. due to the possibility that its fiscal response is inadequate.

- Even with global GDP likely to enter a recession in 2020, we still forecast a modest long-run impact on GDP (0.9%, up from our prior forecast of 0.3%). We still think COVID-19 largely fits the mold of a V-shaped recovery.

For a higher resolution image of the above exhibit, please click here.

Morningstar's coronavirus analysis: epidemiology and society's response

In our first deep dive into the coronavirus, we discussed the potential duration and severity of impact on health and the economy at a higher level, with background on the disease characteristics as well as the burgeoning pipeline of vaccines and treatments. In this update, we dive further into the U.S.' mitigation strategies on a monthly basis for the remainder of 2020, with updated assumptions on severity and spread, as well as how lessons from other countries can be adapted in the U.S. We also provide analysis of recent data for drug treatments and updates on the status of the most promising programs.

With roughly 120,000 Americans diagnosed with COVID-19 by March 28, up from 25,000 as of March 21 and only 70 at the start of the month, the U.S. is now seeing thousands of new diagnoses each day, and many more are probably infected but undiagnosed. Washington was the first state to report a case in January and has been hit hard, although New York and California are also seeing rapid increases in cases and other states could be just days behind their trajectory. For its COVID-19 pandemic preparations, the U.S. government now assumes a pandemic of 18 months with multiple waves,1 and President Donald Trump has extended the expiration of national social distancing guidelines (avoid nonessential travel, restaurants, and gatherings of 10 or more) from 15 days (through March 30) to 45 days (through April 30). Given the grim statistics, many states have moved rapidly to enforce aggressive mitigation efforts well beyond what we initially envisioned as part of our March 9 report. We have moved from containment efforts to community mitigation and suppression of current outbreaks, which includes canceling public gatherings and closing schools for most of the U.S. by mid-March. However, many parts of the country are also working from home, and some are closing nonessential businesses, led by the hardest-hit states like Washington, California, and New York. Many states are activating crisis standards at hospitals in another effort to slow the spread of the disease and reduce the peak number of cases which, without such steps, would overwhelm our healthcare system.

We think the percentage of Americans who will be infected with this first wave of the virus will be relatively low by pandemic standards, at 5%, due to aggressive social distancing measures, and that this wave will last roughly three months. We do expect waves of outbreaks in our base case, not because of weather patterns but because of waves of mitigation efforts that will be applied and relaxed as authorities fine-tune their efforts to contain the disease while minimizing the economic disruption. We think more moderate restrictions during a second wave, when potential treatments as well as diagnostics could be more widely available, could mean an additional 0%-25% of the population infected during that time across our scenarios, beginning when students return to school in September. In all scenarios, we assume that the health impact of the coronavirus in 2021 will be minimal, either due to an effective vaccine or eradication of the virus.

.jpg)