Morningstar’s latest Global Investor Experience (GIE) Study found that Canadian investors continue to experience a tax and regulatory environment that ranks ‘Below Average’.

Earlier today, Morningstar published the second chapter of its sixth biennial GIE report, which grades the experiences of mutual fund investors on a five-point scale – ('Top', 'Above Average', 'Average', 'Below Average' and 'Bottom'). This chapter of the report, authored by Andy Pettit, Aron Szapiro, Grant Kennaway, Christina West, Wing Chan, Matias Möttölä, Germaine Share and Natalia Wolfstetter, with inputs from Morningstar Canada’s director of investment research Ian Tam, covers 26 markets and has four independent chapters on Fees and Expenses, Regulation and Taxation, Disclosures, and Sales. The other chapters will be released later in 2020. You can find the second chapter here.

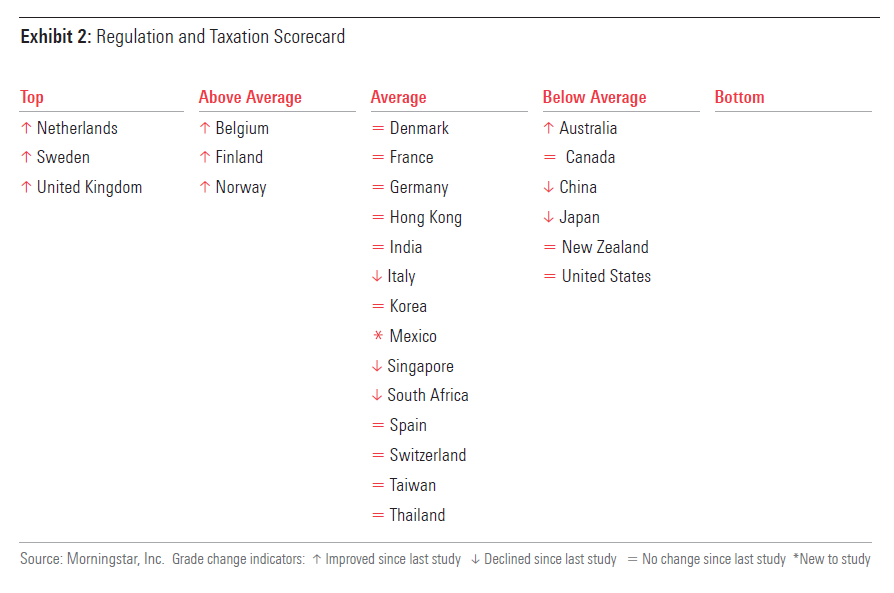

Here’s a look at how countries scored:

Before we discuss key findings, let’s address the pandemic.

COVID-19

This chapter of the study was concluded prior to the COVID-19 pandemic. However, we’ve seen governments and regulators take a variety of different approaches to maintain market stability as well as assist businesses and protect investors during these times. Liquidity was already an issue high on many regulators’ agendas, and the volatile markets have put it back in the spotlight for many countries. We found that most impose limits on how much a product can invest in illiquid or unquoted securities and this reduces risks of forced sales and fund suspensions.

Morningstar.ca has continued exhaustive coverage of the impact of COVID-19 on your money and investments. You can find details here.

Global key findings

The report finds that regulation is not the sole driver of a market’s investment landscape, with aspects like competition and market-focusing events playing a big role. The authors note that markets vary in their policies to give people incentive to invest, but many markets have taken important steps to motivate large numbers of ordinary people to invest for their futures, from creating special tax wrappers to automatically enrolling workers in defined-contribution retirement systems. The most problematic tax policies are when arcane elements of the tax rules prompt investors to choose one product over another without a rationalized policy justification.

The Netherlands, Sweden, and the UK topped the table, in part because they provide strong incentives for ordinary people to invest, although the authors note that none has the best tax systems for ordinary investors. The four markets that performed poorly in previous iterations of this chapter—Australia, Canada, New Zealand, and the United States—continued to score poorly relative to other markets. “It may be that there was no focusing event or crisis to spur an overhaul of a legacy regulatory system that has worked well but has been eclipsed by other markets,” the authors explain.

Oh Canada

For the categories of regulation and taxation, Canada receives a grade of 'Below Average'.

While Canadian investors can access a variety of tax-advantaged retirement plans, supplemental retirement savings are not mandated. In taxable accounts, realized capital gains and dividend income are typically additive to the investor's income for the year. Additionally, investors in Canada typically pay the costs of distribution out of fund assets.

In general, the regulatory framework for investors in Canada is sound and robust. For example, retail investors are made aware of what type of fund they are purchasing and how they are being charged through a mandatory fund facts document, which also includes a standardized risk rating. Recent amendments to regulation have further enhanced client suitability provisions.

Funds in Canada have robust disclosure, liquidity, and governance rules that have generally been effective at providing protection and information to retail investors. Fund companies are required to deliver a fund facts document to the investor upon purchase. The contents of this fact sheet are standardized and in a format that is easy for retail consumers to understand.

In December 2019, approvals were made to a key regulation that requires advisers to address material conflicts of interest, put the client's interests first when making a suitability determination, and do more to clarify what clients should expect from their registrants. These core elements were supported with the introduction of a know-your-product provision and enhancements to the know-your-client suitability, conflict of interest, and relationship disclosure information requirements.

Similar to the U.S. market, soft-dollar arrangements are common practice, but regulations around these arrangements are well-defined and disclosed at the fund company level, but not attributed down to the individual investment level.

The structure of the Canadian fund industry revolves largely around a handful of Schedule I banks that also control the largest distribution networks of advisers. The costs for distribution of funds are charged back to the investor and made transparent in the fund issuer's regulatory filings as well as in the fund facts document, which includes both the management fee and management expense ratio inclusive of distribution charges.

In December 2019, the practice of using deferred sales charges was banned in all provinces except Ontario. The Ontario Securities Commission has proposed a modified set of rules, which is currently out for comment, for the use of deferred sales charges in Ontario.

Morningstar launched the Global Investor Experience study (GIE) in 2009 to encourage a dialogue about global best practices for mutual funds from the perspective of fund shareholders.

How are investors treated around the world?

Get the latest Global Investor Experience Study on regulation and taxation here