Earlier this month, we talked about how investing has a role to play in ending systemic racism. We also talked about how proxy voting is beneficial, and how investors can vote for change with their money. Most importantly perhaps, we talked about how now is the time for companies, and more crucially investors, to take action.

There is no doubt that bias – around race, around gender, around ableism – contributes to the uneven distribution of opportunities, protections, and wealth across society, resulting in systemic, institutionalized discrimination. This issue lurks in investment portfolios and explains much of the observed inequality between the haves- and have-nots.

Morningstar’s director of sustainability stewardship research Jackie Cook points out that while shareholder resolutions are a key way for investors to move the needle within companies on issues of social justice, they often don't garner much support, and adds that if the system through which we invest perpetuates racial discrimination, we investors have a responsibility to be part of the change.

Power in Numbers

In markets like the U.S., investor mobilization has been instrumental in driving democratic changes and tackling injustices for years. For example, Cook points to the first-ever social resolution on a corporate ballot, shareholders asked chemical company Dow (DOW) to halt production of napalm that the U.S. government used in the Vietnam War. Shareholder resolutions also had an important role to play in the anti-apartheid movement, as investors advocated for divestment from South Africa.

Nearer home, and more recently, in a first for Canadian businesses, investors in Waste Connections (WCN) voted in favour of a shareholder proposal that asked the company to establish a plan to increase the representation of women across the workforce, not just in executive positions. The proposal received almost 65% of the vote.

And shareholder activists and investors expect this tradition to continue.

Proposals Incoming in 2020

Cook points to close to 30 resolutions in the U.S., that in one way or another, address racial diversity, inclusivity, and discrimination. In Canada, where fewer resolutions are filed by shareholders, several also address indigenous rights and workers’ rights.

“Resolutions asking for workforce, executive management, and board diversity disclosures continue to receive relatively strong support in 2020--about 43% on average so far this proxy season. Most resolutions ask for a workforce breakdown by race and gender across job categories, and for an explanation of efforts to promote inclusivity,” Cook said.

After the effects of the pandemic and the protests around police brutality in the U.S., shareholder activists expect that the focus of proposals in the next few seasons is likely to be around race, discrimination and equality. In Canada, much of the focus going ahead is likely to be on indigenous rights, health and safety of workers, and general worker rights.

“Investors are beginning to recognize that an economy that systematically excludes whole groups of people is both wrong and fundamentally unstable. This is driving investors to seek more concrete information from companies – to move beyond lip service to building in real accountability to all of their stakeholders, including their workers, contractors, consumers and the communities where they operate,” pointed out Shannon Rohan, chief strategy officer at shareholder advocacy group SHARE.

U.S. Resolutions

Amazon.com’s (AMZN) second-highest supported shareholder resolution of the year (35%) asked the company to “report on its efforts to address hate speech and the sale or promotion of offensive products throughout its businesses.” It argued that failure to adequately enforce its own policies that are intended to prohibit “products that promote, incite or glorify hatred, violence, racial, sexual or religious intolerance or promote organizations with such views” could “…expose Amazon to reputational damage and impair relationships with key stakeholders.”

Another proposed resolution at Amazon--which received far lower shareholder support, a paltry 6%--asked the company to report on efforts to “…identify and reduce disproportionate environmental and health harms to communities of color, associated with past, present and future pollution from its delivery logistics and other operations.” The disproportionate accumulation of pollution in communities of color across the United States and known health consequences of exposure to pollutants, especially pollutants from heavy vehicle traffic, links environmental impacts to social justice.

Facebook (FB) was asked to report on the civil and human rights implications of racial targeting in advertising algorithms, noting that a Russian influence campaign was able to use this feature to target black Americans in the 2016 election. This resolution earned 7% support.

Canadian Resolutions Around Indigenous Rights

Harrington Investments filed a vote in April this year around Scotiabank’s (BNS) consideration of potential impacts on human and Indigenous peoples’ rights, including respect for free, prior and informed consent of Indigenous communities affected by Scotiabank’s financing.

“Violations of human rights can expose a company to liability for those abuses, even if the company does not participate directly in those abuses and tries to distance itself from them. Scotiabank has exposed itself to this liability by providing financing for oil, gas and coal development projects entangled in Indigenous rights violations, including the failure to obtain their free, prior and informed consent about projects on their land., through various project- and corporate-level loan agreements,” the filers pointed out in their proposal.

The bank rejected the assertion, saying, “As part of our ongoing discussions with the shareholder over the last four years on these topics, we have continued to evolve our practices including revising our human rights statement in 2019 to be more explicit about how we acknowledge and respect the rights of Indigenous Peoples. We also revised the statement to reflect the extensive due diligence requirements in our policies and procedures to address these issues. After years of ongoing dialogue and considerable work by Scotiabank, the proposal has been substantially implemented and therefore, the board recommends voting against it.”

The shareholders voted on the issue on the 7th of April, and it received close to 9% of the vote.

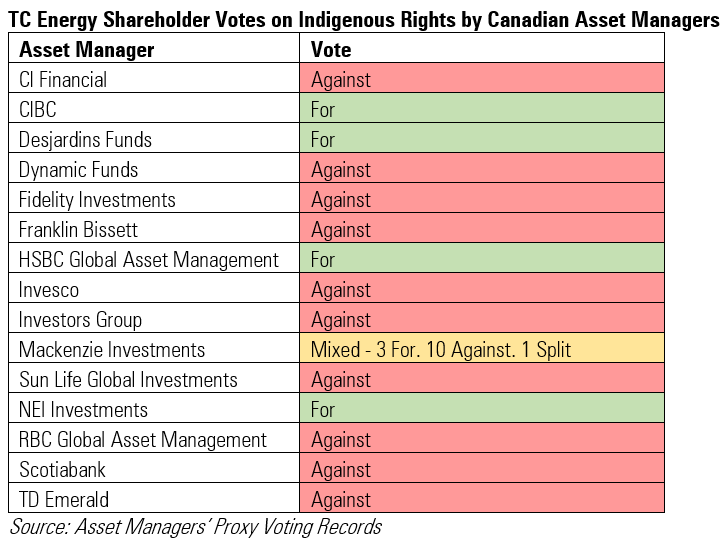

Another Canadian vote on indigenous rights was the 2019 TC Energy (TRP) vote. Shareholders asked for a report, within six months following the 2019 Annual General Meeting and annually thereafter, outlining how TransCanada respects internationally recognized standards for the rights of Indigenous Peoples in its business activities.

The company asked that shareholders vote against the resolution, saying that additional reporting would impose significant administrative burden without providing material new information to our shareholders. The proposal won a little over 10% support, with several Canadian asset managers voting against the proposal. Here’s a look at how the asset managers voted:

Asset Managers Must Act

Cook points out that in an increasingly connected world, reputation is becoming more and more important for businesses, both as a potential asset and a potential liability. At the company level, businesses that contribute to institutionalized discrimination by failing to tackle racial discrimination and bias in their products, workplaces, supply chains, and marketing practices risk losing their social license to operate.

The wave of protests calling for racial equality will likely lead to stronger investor action beyond the 2020 proxy season, addressing the investment and reputational risks of racism in its many forms. On a bigger scale, social unrest and a general erosion of trust could have significant consequences for the economy.

But without much support from large asset managers, vote outcomes on many shareholder resolutions addressing institutionalized discrimination remain relatively low.

“Fund investors need to take a close look at their funds’ voting records around discrimination and inequality and call for stronger alignment between recent statements supporting racial equality and proxy votes. The institutions representing individual investors in the proxy process are stewards of capital markets--markets that are inherently racially biased. These institutions could be using their voting power and advocacy to reduce the appalling differentials that taint investors’ portfolios,” Cook says.