The reaction of dividend funds and stocks during the recent correction caused by the COVID-19 pandemic is good reason for investors to stop and think about whether dividend investing makes sense as an investment strategy. Here are four facts that will help you decide:

1. The Fundamentals: A Tale of Two Companies

Financial theory tells us that as an investor purely concerned with growth of financial capital, one should be indifferent between receiving a dividend, or receiving capital gains. For illustrative purposes, let’s assume that you are looking at two theoretical companies with identical businesses and somehow magically identical management teams, but with different policies on dividends (a Black Mirror-type scenario, if you will).

Company A does not pay a dividend and opts to re-invest its earnings to fuel growth by expanding business lines, increase efficiencies, and conduct R&D to innovate and bring new products to market. The eventual investment return provided by Company A comes when you sell the stock, if the company is successful at deploying that capital and turning a profit, thus commanding a higher company valuation. By investing in Company A, you are taking a calculated risk by assuming the management team can effectively deploy that capital to fuel growth.

In the alternate universe, Company B opts to pay out a percentage of its earnings in the form of dividends on a regular basis. You receive this amount in cash, and you are now responsible for doing something with that cash. You may choose to take that cash and purchase more of the same stock, which will increase your stake in the company and entitle you to more wealth when you eventually sell. In turn, company B will likely take that additional investment and deploy it much like Company A did. In other words, if you re-invest your dividend back, the wealth in your pocket will be similar to Company A. If you do not re-invest, Company B’s growth rate will be lower than Company A’s because it now has less capital to deploy (since they paid you a dividend). This said, they will still grow but likely without your re-investment they will not grow as fast as Company A.

Over the long term, both conceptual companies will provide the same amount of pre-tax wealth to you. The difference is in the timing of when you receive the cash. Company A pays you when you sell the company while Company B pays you along the way and will sell for less than Company A.

2. Taxes: Why All Things are Not Equal

With some exceptions, Canadians pay the highest amounts of tax on interest income (such as income from bonds), followed by dividends, then capital gains. The exception is for those who are in lower tax brackets, where dividends are taxed less than capital gains. Here is a great resource to know the marginal tax rates in your province.

For those saving for retirement (and are more likely in higher income tax brackets) capital gains will often provide better tax treatment and more wealth in your pocket at retirement. For those in lower income tax brackets, dividend income may make more sense over capital gains.

It’s also important to remember that the effect of a higher tax rate on dividends is two-fold: the higher tax rate itself, and the effect of compounding. Paying taxes out of dividends received means that you are stifling the amount being re-invested and are reducing the effects of compounding.

3. Income Requirements: There is Another Way

Some investors require a steady, or fixed, income stream. Traditionally, this income comes from the aptly named ‘fixed income’ portion of a portfolio. However, with interest rates at near-zero levels, low yielding bonds are driving many investors to look for dividend-paying companies to supplement the income requirement.

But dividends are not the only way an investor can derive income from a stock investment. We can achieve this through a ‘synthetic’ dividend which may include a covered call option strategy (talk to an options-licensed investment advisor for this) or simply by selling off some portion of your equity in a disciplined manner. Doing so has the same effect as a dividend paid by the company and allows you to de-couple the income requirement from the type of stocks that you pick. Additionally, depending on your tax bracket, this may offer tax advantages too.

4. Downside Protection: Yes, but let’s not exaggerate.

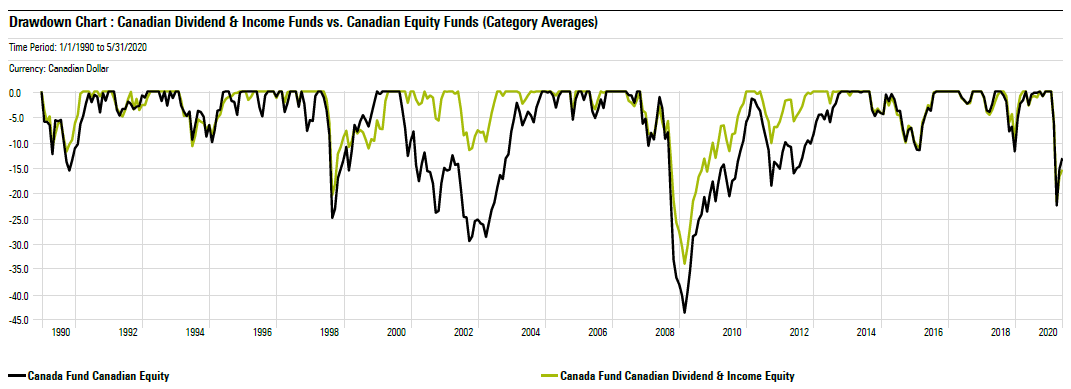

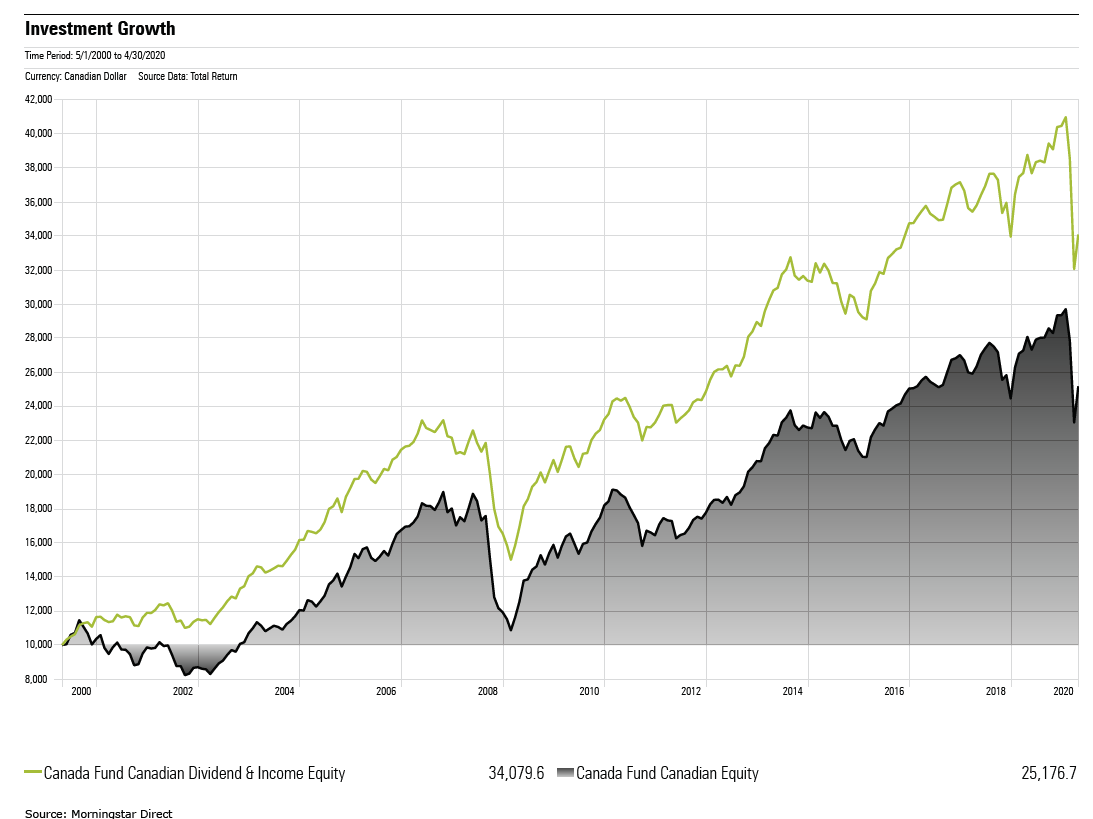

An often-cited statement is that dividend paying companies offer more protection than those that don’t pay dividends. There is certainly some truth to this, as we can see in the following charts that compare the performance of the average Canadian dividend and income fund against the average Canadian equity fund.

During the technology bubble, dividend funds offered significant protection, because technology companies didn’t pay dividends. However, during the Asian currency crisis, the global financial crisis, and the recent COVID-19 pandemic (which affected multiple sectors), they did not offer nearly as much protection. Remember, dividend paying investments are still stocks, and will exhibit volatile characteristics similar to the rest of the asset class. In times of economic hardship, the decision to maintain or cut dividends rests solely on the shoulders of company management. When dividends do get cut, not only does the fundamental valuation of the company get reduced, but so too does market sentiment which will cause short term fluctuation in the stock’s price.

Over the long term, the Canadian dividend and income category has shown merit by outperforming the Canadian equity category, but with significant bumps along the way.

Are you getting the right returns?

Get our free equity indexes to benchmark your portfolio here