Earlier this week, Vanguard Investments Canada listed a new single-ticket, low-cost retirement income exchange-traded fund called the Vanguard Retirement Income ETF Portfolio (VRIF).

The Canadian dollar hedged ETF is a fund of funds and is the latest addition to its line-up of asset allocation ETFs. It is made up of eight existing Vanguard index ETFs, four equity, and four fixed income. It has a targeted annual payout of 4% and has a management fee of 0.29%.

The product was in response to a market need for a product that investors could use for steady income in retirement, said Scott Johnston, Head of Product, Vanguard Investments Canada. “While Canadian investors are saving for retirement, we found that once they get to the retirement stage, they don’t have too many choices of products and so we launched this one.”

Vanguard conducted a recent investor poll that found that retirement is the number one investing objective for Canadians, with 78% listing it among their top two choices. Johnston also pointed to a report by the World Economic Forum that estimated that Canadians are expected to outlive their savings by an average of 10 years, which indicates the need for prudent, low-cost and well-diversified portfolios that can provide dependable income.

The fund is targeted at retirees and soon-to-be retirees, or anyone who wants a steady income. “Retirement is not a binary decision anymore, so we found that the investors close-to-retirement are also of interest for this product. It offers a fixed dollar amount each month for any given year, so it targets anyone who wants a steady income to support their lifestyle,” Johnston said.

What Does it Hold?

In terms of its underlying portfolio, the fund will hold 24% of its assets in the Vanguard Canadian Corporate Bond ETF, 22% each in the gold-rated Vanguard FTSE Developed All Cap ex North America Index and Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged), 18% in the gold-rated Vanguard U.S. Total Market Index ETF, 9% in the gold-rated Vanguard FTSE Canada All Cap Index ETF, 2% each in the silver-rated Vanguard Canadian Aggregate Bond Index ETF and the Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) and 1% in the bronze-rated Vanguard FTSE Emerging Markets All Cap Index ETF.

The fund has started with a 50:50 equity and fixed income spread. In terms of geography, 35% of its assets are based in Canada, and 64% in developed markets outside Canada (20% in the U.S.) Investors in the fund also get a 1% allocation to emerging markets.

“The focus of the fund has been a total return, which allows us to make up the difference in case dividends or yield don’t provide the income we seek. At present, the income comes 60% from dividends and fixed income, and 40% from capital appreciation – though this could change,” Johnston said.

Payouts

For many of the investors in the fund, the payout is the most important part, and Johnston agrees.

“The focus of the fund is the payout, and we pay close attention to how the payout is funded. Any changes in asset allocation or sale of assets will be tailored to funding a steady payout,” he said.

This does not mean that a 4% return is guaranteed. Johnston notes that the 4% target is an initial one, and this could be revisited. The fund will adjust the return target annually, which means investors could expect the payouts to be higher – or lower – than 4% going ahead.

The fund can be held in both tax-sheltered, and taxable accounts. The total-return approach means it can distribute from capital appreciation, while also holding taxable dividends and income products. It is intended to be a single ticket retirement solution.

Like the Asset Allocation ETFs

Vanguard Canada says that the ETF is a complement to the existing suite of five all-in-one asset allocation ETFs, which have gathered more than $3.5 billion in assets since the initial launch in 2018. This brings the total number of Vanguard ETFs in Canada to 37, with $26 billion in ETF assets under management.

The firm points out that asset allocation ETFs are one of the fastest-growing investment categories in Canada, and have attracted $4.5 billion in under three years. It calls the products “a game-changer for investors”.

“For financial advisors, this provides a scalable and transparent solution for clients as a complement to their retirement strategy. For investors, this is a one-stop globally diversified and turnkey option that provides capital appreciation and monthly tax-efficient income,” Johnston said.

The Risky Hunt for Yield

Johnston agreed that recently, investors have moved into risker asset classes in the hunt for yield. He also notes that investors moved to fixed income to protect themselves, so it seems like they are seeking both risk and returns.

“The hunt for yield sometimes comes at the cost of ignoring risk, and that could lead to a bad outcome,” he said.

As always, he guides caution. “Ask yourself, what are your goals? And know that if you are actively seeking higher yield, you are taking higher risk, can you afford it?”

He points out that though investing in higher-yielding products like higher dividend payers, or higher risk corporate bonds might be appealing in the short term, investors who build portfolios exclusively around these are too niche, and it could lead to capital loss over the longer term.

Instead, he recommends that investors consider total return focused portfolios, and not just chasing yield. He also recommends that investors leave the heavy lifting to the experts.

A Word on All-in-One ETFs

Morningstar Canada’s Director of Investment Research, Ian Tam, says that all-in-one ETFs can be an excellent choice for do-it-yourself investors who are conscious of transaction costs and other fees and are willing to do a bit of leg work to understand what mix of assets (stocks, bonds, cash) is appropriate for their risk tolerance.

“Though the concept of an allocation fund is not new, providing access to multiple asset classes through other low-cost index ETFs and traded through a single ticker is appealing, especially for those who use a discount brokerage. For investors with small starting amounts, this is a very good value. The fact that these products automatically re-balance is also a useful feature and ensures that the mix of assets is within limits which otherwise would require quite a bit of discipline for an investor to do on her own,” Tam says.

But how do you pick the right one?

Well, if you don’t know what to do, or if you don’t want to research funds, routinely monitor your portfolio, and rebalance regularly, then Tam recommends all-in-one ETFs, especially if you don’t have an advisor.

“The first step would be to understand how much risk you can handle. This is often tied to how long your time horizon is, and what your financial situation is. The longer your time horizon and the stronger your finances, the more risk you can handle which would correlate to the percentage of stocks (as opposed to bonds and cash) held in your portfolio,” Tam says.

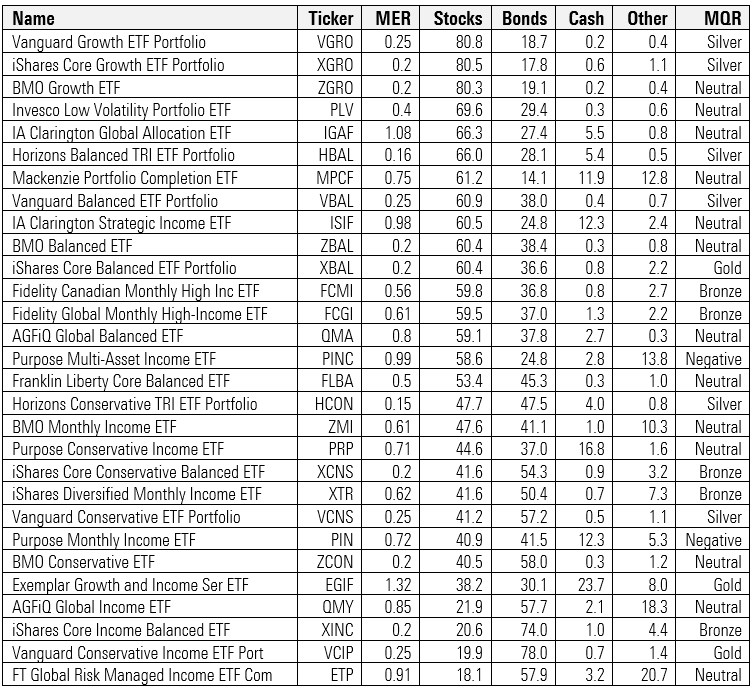

To help narrow down choices, Tam summarizes the allocation ETFs available in Canada and sorts them on stock exposure:

How Exposed Is Your Equity?

Get The Global Makeup Of Equity Indexes With Our Free Tool Here