If you’d been following IPO news, or stock market news, or any investment news over the past six months, you could not have missed references to ‘Blank-Check Companies’, or SPACs. Most recently you might have heard about it in the context of General Motors and Nikola.

Here’s the backstory. General Motors (GM) made an announcement in September 2020 that it was getting into a “strategic partnership” with Nikola, an electric vehicle company that at that point had not yet manufactured a product. According to the terms of the agreement, GM would receive an 11% equity stake in Nikola in exchange for manufacturing the Nikola Badger pick-up truck using GM’s own hydrogen fuel cell and battery technologies.

A couple of days after the deal was announced, Hindenburg Research published a report called ‘Nikola: How to Parlay an Ocean of Lies into a Partnership With the Largest Auto OEM in America’. The report claimed the authors had evidence of fraud perpetrated by Nikola.

Since then, the founder and chairman of Nikola has stepped down, the SEC and Justice Department are looking into the claims made in the report, and the stock has fallen over 20%. Stephen Girsky, a former vice-chairman of GM and a member of Nikola’s board has taken over as chairman.

Nikola Not the First

Girsky founded an investment company called VectoIQ that then created a special company which was publicly listed but had no business operations. VectolQ was created specifically to take Nikola public via a so-called reverse merger: the SPAC merged with Nikola in June this year, and Nikola became a publicly-traded company as a result.

Companies that go public via reverse mergers circumvent some of the stringent requirements of the SEC in the United States. How? And why? To understand that, you need to know what SPACs are, and how they work.

What Are SPACs?

A ‘Special Purpose Acquisition Company’ is a company with no real business operations. It exists only to raise capital via an initial public offering, or an IPO, and to then use that capital to buy existing private companies.

“This atypical pathway to the public markets was once a niche strategy for small investment firms," as Morningstar Pitchbook analyst Cameron Stanfill explains.

These companies own and manage nothing except the cash that they raise. Because of this, they are called ‘Blank-Cheque Companies.’ They are generally formed by investors, also called sponsors. Sponsors usually have experience and expertise in a particular sector, and it is assumed that the acquisition targets will be companies in that sector. Many sponsors are seasoned private equity investors.

"These early embracers saw SPACs as a way to extract fees from adding structure to a reverse merger," notes Stanfill. "The strategy has now become the hottest financial topic of 2020 after a massive uptick in the volume of these blank-check vehicles and as the stature of the investment professionals involved legitimized the space.”

How Do They Work?

Stanfill describes the process like this, “At first, the SPAC follows the traditional IPO process, registering with the SEC, filing prospectuses and running investor roadshows. This entity then prices the IPO and raises the funds that will subsequently be deployed to acquire the target business. At this point, the SPAC is a publicly traded shell company and has assumed much of the cost and time commitments usually borne by the target company.”

Once the SPAC raises capital, it usually has two years to complete a deal. If it does not, it faces liquidation. In the meantime, the capital is placed in a trust account, which earns interest at market rates.

What’s interesting though, is that when these companies IPO, they do not have to identity the companies that they want to acquire. Put another way, if you buy into a SPAC, you will have no idea which company you might end up owning. You don’t even know IF you will end up owning an acquired company.

The concept of a SPAC itself can be boiled down to a pre-sold IPO for the private company that it acquires – without many of the stringent requirements, checks and balances that go into a traditional listing.

Red Flags

Investors should remember that the long (and indeed, tedious) IPO process is in place to protect investors. When a company goes public via a traditional IPO, there is careful institutional and regulatory vetting, which ultimately benefits the investor by bringing issues to light.

Take for example the Nikola case. If Nikola was to have gone the traditional IPO route, there would have been a much more stringent due diligence and audit process than with the SPAC reverse-listing. It is important to note that at present, the allegations of fraud are just that – allegations. The SEC is in the process of investigating the claims. But nevertheless, there are questions around whether the claims would have gotten as far as they have if the firm had gone through the traditional IPO route.

But let’s go back to SPACs.

Why 2020?

SPACs have been around for at least 30 years. Why all the interest now?

Stanfill points out that direct listings were all the rage in 2019. “Then came the pandemic, which plagued markets with economic uncertainty, especially in public markets. The sustained volatility and the distinct price declines earlier in 2020 made IPOs and direct listings impractical options for the majority of private companies, which is where SPACs have found an opportunity. Unlike SPACs, direct listings do not allow private companies to raise any new capital during their transition to the public markets, which presents a problem for many start-ups, given the elongated economic ambiguity driven by the pandemic.”

Essentially, he describes SPACs as large “boxes of money, that necessitates a much lower level of diligence than a similarly sized IPO of an operating entity, since there are no financial statements to scrutinize.”

Now that traditional IPOs are relatively fewer, investors have flocked to SPACs, in the hope of hitting upon the next Tesla (TSLA), or PayPal (PYPL). With this increased demand, existing sponsors have raised higher amounts. For example, Chamath Palihapitiya’s Social Capital Hedosophia’s first two SPACs acquired Virgin Galactic and Opendoor. He has since launched three more SPACs.

The true value of SPACs rest in the companies they acquire, and that's the main draw for retail investors. But you need to weigh this potential against the costs and risks associated with the convenience of SPACs afforded to other people.

Who Makes the Money?

It’s not always smooth sailing, however. “Despite the benefits SPACs offer, they are not a cure-all. From a cost perspective, a merger with a SPAC nets out to essentially the same cost outlay to the company as a traditional IPO. The original IPO fees are paid initially by the SPAC itself—typically 5.5% of the amount raised in the SPAC—but these costs are implicitly passed on to the company along with the sponsor’s promote and any investment banking fees related to the acquisition itself,” Stanfill says.

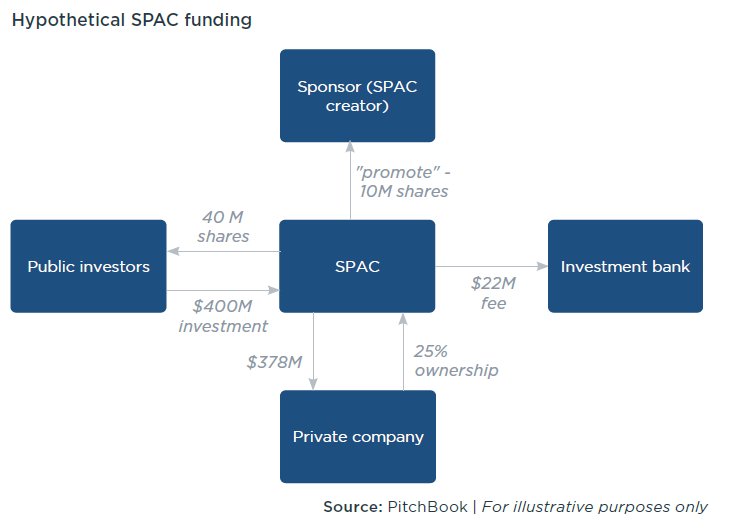

He explains it with this example. If a hypothetical SPAC raised a $400 million IPO by selling 40 million shares at $10, the vehicle would pay $22 million in fees to the investment banks, leaving $378 million for the transaction. At the SPAC’s founding in this scenario, the sponsors bought 10 million shares for a nominal fee rather than buying them for $100 million, therefore implicitly taking away capital that could have been raised by the company. In this simplified version, the company is implicitly paying $122 million to raise $500 million, leaving the company with $378 million or a 22.4% cost of capital without even factoring in warrants. This is relative to a traditional IPO raising $500 million, which at a 7% fee would cost the company $35 million, with the proceeds to the company totaling $465 million.

Should You Buy A SPAC?

Still want to go for an SPAC? As always, we guide caution.

First, You do not know in advance the acquisition target you’re taking a bet on the founder of the SPAC. Retail investors rarely have insight into the minds of founders, and can only make bets based on public perception. This is a risk.

Second, even if the founder has a target in mind, the SPAC might not be able to close the deal. If this is the case, and you get your money back a few years after the initial investment, that is an opportunity cost. An opportunity cost is what you lose in gains you could have potentially made, had you not invested in the SPAC.

Third, as Stanfill’s note on fees to investment banks shows, there’s a lot of people making a lot of money from SPACs – and those people don't seem to be retail investors.

Fourth, the success of the SPAC depends on the success of the company it acquires. As established, the research, due diligence and checks behind these acquisitions may not be as stringent as it would have been in the case of a traditional IPO, or public company acquisition. It again seems like the investor is the loser.

So before you invest in an SPAC, ask yourself who is making the money, on what, and if you have alternatives you could consider. And as always, invest based on your financial goals, risk appetite and time horizon. When in doubt, seek a financial advisor.

How Exposed Is Your Equity?

Get The Global Makeup Of Equity Indexes With Our Free Tool Here