The coronavirus pandemic has caused unprecedented changes and disruptions in everyday life. Of these changes, few have been as impactful or as frequently discussed as the lockdown-induced work-from-home experiment, which has caused many to question conventional wisdom on how work should be conducted. This experiment has caused widespread speculation that the office real estate industry will be permanently impaired as employees work remotely forever.

We demur. For all its excess, the coworking craze demonstrated that the desire to convene physically to conduct work has strengthened even in an increasingly digital world. Moreover, most employees have emphatically indicated an enduring preference toward flexibility in the form of hybrid remote work. Elements central to work, such as collaboration, company culture, and career development, are more effectively served in a centralized, purpose-built office environment.

Nevertheless, the office real estate industry has a difficult road ahead. It is inherently cyclical, and the scale of office-prone job losses closely mirrors the global financial crisis. Furthermore, we still expect the pandemic to increase the pace of growth in fully remote and hybrid remote work, both of which were already gradually growing before the pandemic. These two factors will damp demand for office space, informing our conclusion that demand for office space will remain essentially flat through 2029, with a compound annual growth rate of 0.1%.

Although we expect muted demand growth, the office real estate investment trusts and commercial real estate services companies we cover represent compelling investment opportunities. Investors have allowed negative headlines to drive undue pessimism regarding the industry. New York office REIT SL Green (SLG) and commercial real estate services company Jones Lang LaSalle (JLL) are our top picks, although there are several other compelling investments in this market environment.

- In the United States, we forecast that total demand for office space will be essentially flat over the next decade, at a CAGR of 0.1% through 2029, compared with our pre-COVID-19 forecast of around 0.4%. Our reduced forecast is driven by cyclically induced job losses that will take until 2022 to fully recover and a modest reduction in space due to the increased prevalence of fully remote and hybrid remote work. This is in addition to previously existing factors such as modest cyclically adjusted growth in office-prone employment.

- The scale of lost office demand due to cyclical job losses will be roughly commensurate with lost demand due to the secular impact from increased remote work. We expect peak-to-trough job losses to reduce demand for office space by around 187 million square feet, although this space will come back once the economy improves. By comparison, around 200 million square feet will be lost over the next decade due to remote work, with this space not returning.

- We reject the false dichotomy between working from the office and working from home. Instead, we contend that the future of work is increased flexibility in the form of greater hybrid remote work. In concrete terms, we expect the percentage of the American labor force working from home four-plus times per week to increase from 9% before the pandemic to 13% by 2025. We had expected a 0.7% increase before the pandemic.

- Fully remote work will have a larger impact on office demand than hybrid remote work. Many hybrid remote employees will retain a desk, resulting in no impact on office demand. We think most companies will continue to expect employees to work from the office simultaneously to reap the collaborative and culture-building elements of the office, meaning that they must plan for peak usage.

- The office is hardly facing the threat of obsolescence, despite hyperbolic proclamations suggesting as much. Although we expect some increase in fully remote work and a modest increase in hybrid remote work, the office provides functions that cannot be fully replicated in a digital environment.

- Densification, whereby square feet per employee decreases, had been a drag on office demand before COVID-19. The outbreak of the coronavirus has temporarily halted this practice. We expect it to resume, albeit at a slower pace, once the pandemic is fully resolved.

- The pandemic and its resulting focus on public health has also temporarily halted the practice of hot-desking, whereby employees do not have dedicated desks. We expect this to remain the case through the duration of the pandemic, although the practice will gradually regain popularity once health concerns are resolved and as more employees opt for hybrid remote work options.

- Although some suggest that the pandemic represents an opportunity for suburban office real estate, we are more skeptical. Such space is already in abundant supply, and we doubt employers will choose to expand their footprints much amid the outbreak. Once the pandemic is resolved, we expect the same drivers behind the outperformance of urban office real estate to return.

Investor Trepidation About the Office Sector Results in Bargains

The market has reacted to the coronavirus crisis by shunning any entity with exposure to office real estate. We recognize that the industry faces a difficult period. However, we think prevailing valuations are harsh and imply a reality that is far too gloomy.

When the coronavirus first struck in the U.S., speculation was rife that office real estate owners would struggle to collect rent. Some were even suggesting that the lockdown conditions constituted a force majeure circumstance that justified nonpayment without penalty.

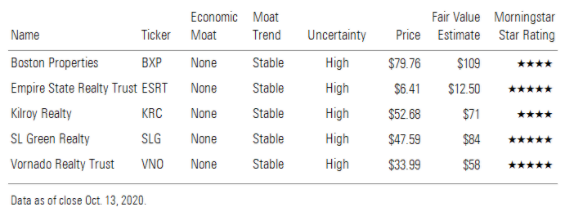

But such fears have receded, with creditworthy tenants largely making their payments, although with a slightly longer collection period. In fact, high-quality names such as Boston Properties Group (BXP) and SL Green reported office property rent collection rates of 98% and 96%, respectively, during the second quarter.

We even see evidence that collections have improved as the crisis has dragged on, with Empire State Realty (ESRT) showing the most impressive improvement. The company reported 73% office rent collection for April, and that figure improved to 93% for July.

Despite the impressive nature of rent collections, the worst is yet to come for the office real estate market. With the suddenness of the crisis causing transaction volume to crater, it remains unclear how badly market rents and occupancy will decline.

Nevertheless, we view many of the office REITs we cover as undervalued, with SL Green providing the most attractive valuation. Investors are understandably concerned about the short-term cyclical impact presented by the coronavirus-induced recession as well as the specter of long-term demand destruction presented by remote work.

In the case of SL Green and its New York City-based peers, investors are even more pessimistic. The region was the initial epicenter of the pandemic, and its image suffered somewhat. Furthermore, a glut of supply additions spurred in large part by the Hudson Yards megadevelopment was large enough that investors were already wary of the market.

We share many of these concerns and model sharp declines in net operating income through 2021, with the market barely recovering to its prepandemic level by the end of 2022. Although we expect choppy market conditions, New York City and its office market will recover from the current crisis. The city certainly has its share of issues, and certain aspects specific to its office market merit concern. However, the market has unfairly punished SL Green for this, in our view.

We retain belief in New York’s unique infrastructure assets and its position as a hub for global talent. In fact, some of the same tech companies that have provided media-friendly remote work announcements have reiterated their commitment to the city by planning to locate more jobs there and signing for additional square footage. For example, Facebook recently increased its footprint in New York City by signing with Vornado Realty’s (VNO) 730,000-square-foot Farley Building in Midtown Manhattan.

There are also some emerging concerns regarding the increased debt load for many office REITs. Vornado is the most concerning in this respect, with a debt/EBITDA ratio of 14, although we expect this to settle at around 11 by the end of 2020. Such levels are certainly cause for concern, and Vornado has announced a cut to its dividend to ensure financial stability. The company is hurt by exposure to high street retail that far exceeds that of its office REIT peers.

Despite the elevated level of debt, though, we do not see Vornado or any of its peers as being in danger of a liquidity crisis. At the end of the second quarter, Vornado possessed a quick ratio of 6.6 and an EBITDA/interest ratio of 2.6. We expect the second and third quarters to be the height of the downturn and note that even in this environment, it appears that Vornado and its peers are devoid of any liquidity concerns.

Empire State Realty entered the pandemic with the most attractive balance sheet among the office REITs we cover, and this approach is set to pay off. However, challenges deriving from exposure to the Empire State Building observatory deck and a lower-quality tenant base have caused the company to not pay a dividend for the rest of 2020. This prudent move was largely preventative and should stop the company from running into major difficulty in an unprecedented environment.

Commercial Real Estate Services Stocks Have Cratered

The three commercial real estate services companies we cover have fared poorly in the current crisis despite showing some pockets of strength. The pandemic has introduced a level of uncertainty that has caused commercial real estate transactions to freeze up as most players employ a wait-and-see approach.

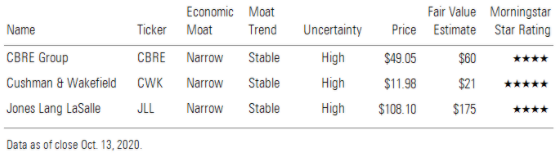

We expect Jones Lang LaSalle’s revenue to drop 13% year over year in 2020, with EBITDA declining 24%. The dramatic nature of the declines derives from weak performance in the brokerage business, which generates attractive margins but is highly transactional.

However, we still view Jones Lang LaSalle as one of the most attractive valuation-adjusted names on our list, with larger peer CBRE (CBRE) seeing much stronger performance in its stock despite operating in the same industry. Jones Lang LaSalle’s share price decline since the pandemic broke out has shown far too much market pessimism, in our view.

Although Jones Lang LaSalle operates in a highly cyclical business, it carries a healthy balance sheet and is part of a triumvirate of companies that are uniquely positioned to capture share in an industry that is ripe for consolidation. It is second only to CBRE as a global commercial real estate services company and is able to effectively compete for business and contracts despite the slight disadvantage in size.

The commercial real estate services companies have varying levels of exposure to the transactional brokerage business. CBRE has the largest exposure with 68% of its revenue coming from this type of business, while Cushman & Wakefield (CWK) only has 46% of its revenue coming from this category.

All three companies have benefited from a boom in demand for corporate real estate outsourcing for functions such as facilities management among other services. During the current crisis, such services have proved invaluable, with owners and occupiers of real estate space relying even more heavily on institutional support amid an explosion of uncertainty.

We expect this business line to provide a measure of stability for CBRE, Jones Lang LaSalle, and Cushman & Wakefield. The business is more contractual in nature, and renewal rates have essentially hit 100% in the current environment. However, it has a lower relative margin profile, which will contribute to an even greater deterioration in EBITDA compared with the already dramatic declines in companywide revenue.

How Exposed Is Your Equity?

Get The Global Makeup Of Equity Indexes With Our Free Tool Here