Note: This is an editorialized version of the 2020 Balanced Fund Landscape for Canadian Fund Investors. You can find the report here.

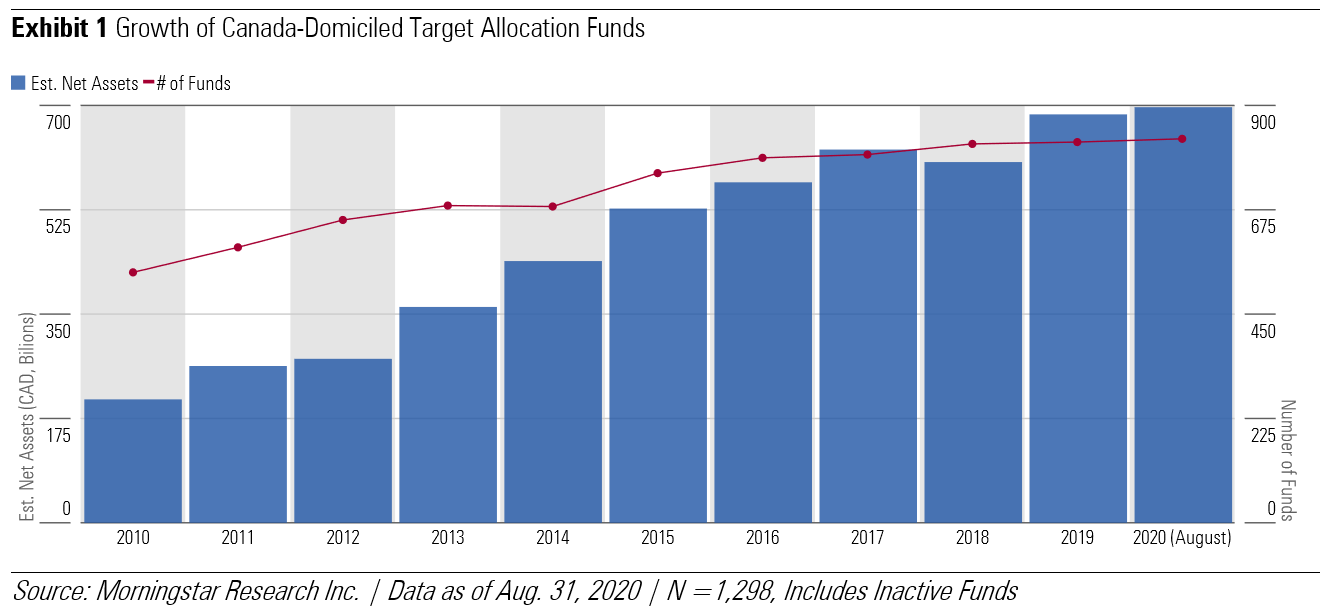

The Canadian target allocation fund market (also known as balanced funds) continues to remain important for Canadian retail investors. At the end of August 2020, assets invested in 800 balanced funds totaled close to $700 billion by our estimates, tripling in size over the past decade.

Balanced funds hold a relatively static mix between stocks and bonds. The popularity of these investment vehicles is the ability for investors and advisors to match risk tolerance and time horizon to a single fund, allowing professional managers to keep a close eye on asset allocation and ensure that the mix is regularly re-balanced.

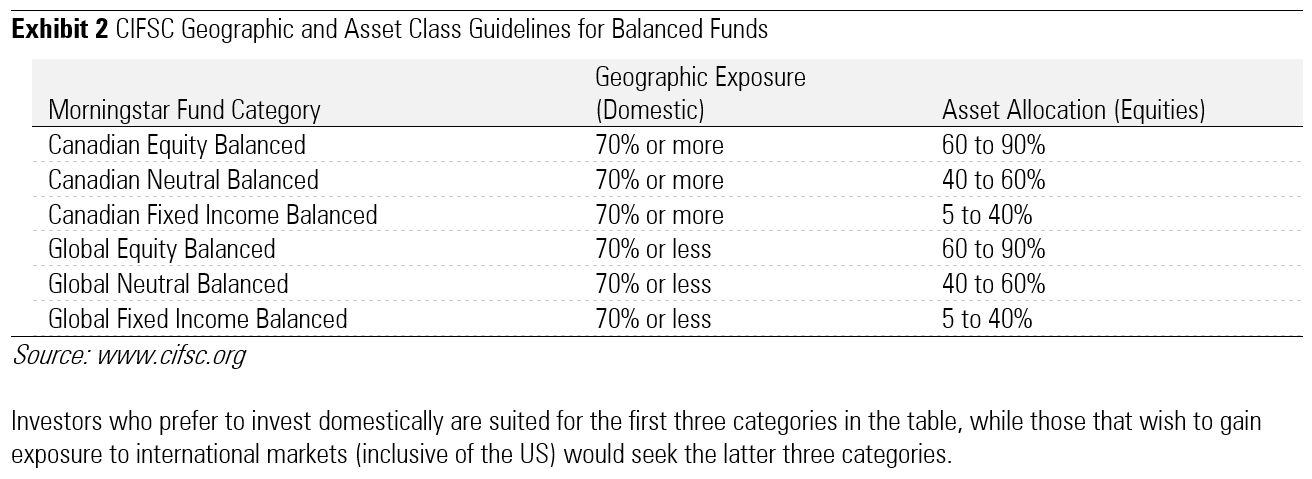

In Canada, there are six main categories of balanced funds, as defined by the Canadian Investment Funds Standards Committee (www.cifsc.org), of which Morningstar is a voting member. The names of each category relate to their asset allocation and geographic exposure.

Investors who prefer to invest domestically are suited for the first three categories in the table, while those that wish to gain exposure to international markets (inclusive of the US) would seek the latter three categories.

Balanced Funds and COVID-19

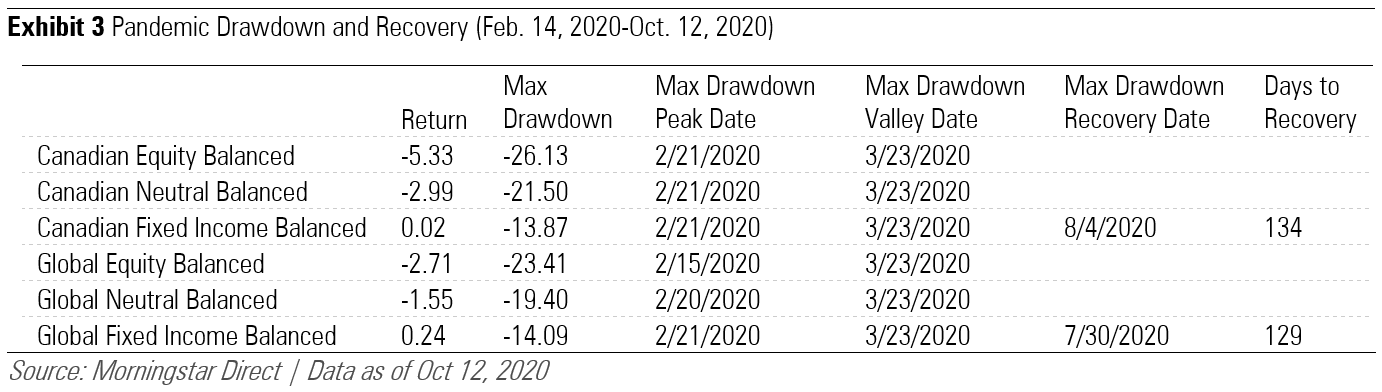

2020 has been a tumultuous year for all investors, thanks to the coronavirus pandemic. Balanced funds were not immune to the effects of the sell-off experienced in March.

By our estimates, these categories of funds experienced a significant a net outflow of $9 billion in March. Performance-wise, balanced funds withstood significant drawdowns in the same month with only fixed income balanced categories having recovered to their pre-pandemic highs. In effect, funds with more bonds in them lost less, and hence have been the quickest to recover this year.

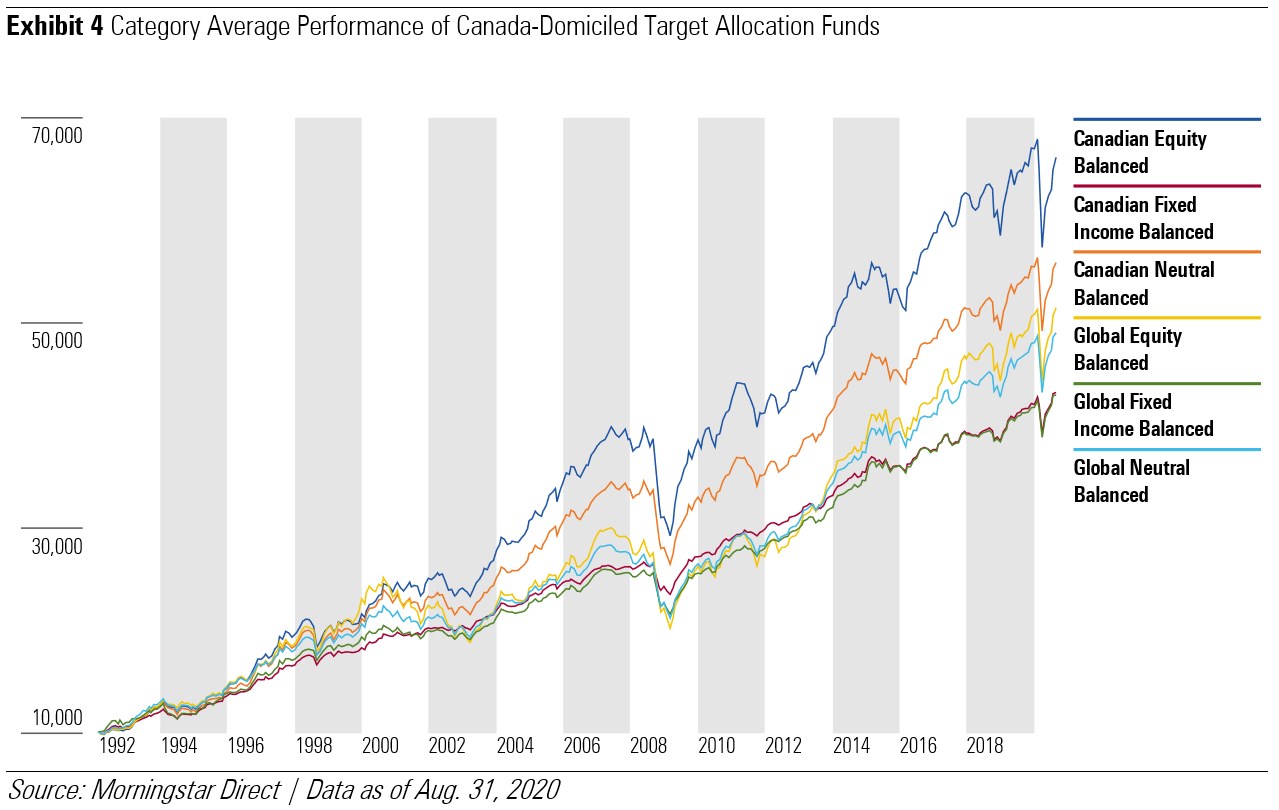

What About the Long-Term?

Over a long timeframe and in the context of Canadian and global exposures, target allocation categories performed as modern portfolio would expect; funds with higher exposure to equities outperformed those with less. However, global categories (those with greater than 70% exposure outside of Canada) did not fare as well as their domestic counterparts over the 30-year time frame indicated in the chart below.

How Do We Benchmark Balanced Funds?

A major issue for Canadian allocation fund investors is the lack of standardized market wide benchmarks for target allocation funds, making it challenging to objectively gauge funds' performance against an index. Case in point, a look across the oldest share class of 769 different target allocation funds in Morningstar's database shows 456 unique prospectus benchmarks with 178 listing pure equity or pure fixed-income benchmarks (which by nature of the categories is counterintuitive). To solve for this issue, in July, Morningstar launched a series of target allocation benchmarks specific to the Canadian market.

These benchmarks are unique in that they are aligned with the Morningstar Category classification system (which in Canada is also aligned with categories set out by the CIFSC). The benchmarks use observed historical portfolio holdings data that is free from survivorship bias to capture Canadian investors' home bias and preference for certain asset classes, including a cash component. The methodology used for this family of multi-asset indexes is the first to follow a consistent benchmark construction approach across global regions. Like all benchmarks, Morningstar’s target allocation index family comes free of fees. This is of particular relevance in Canada where it can be argued that fees are substantial within target allocation funds.

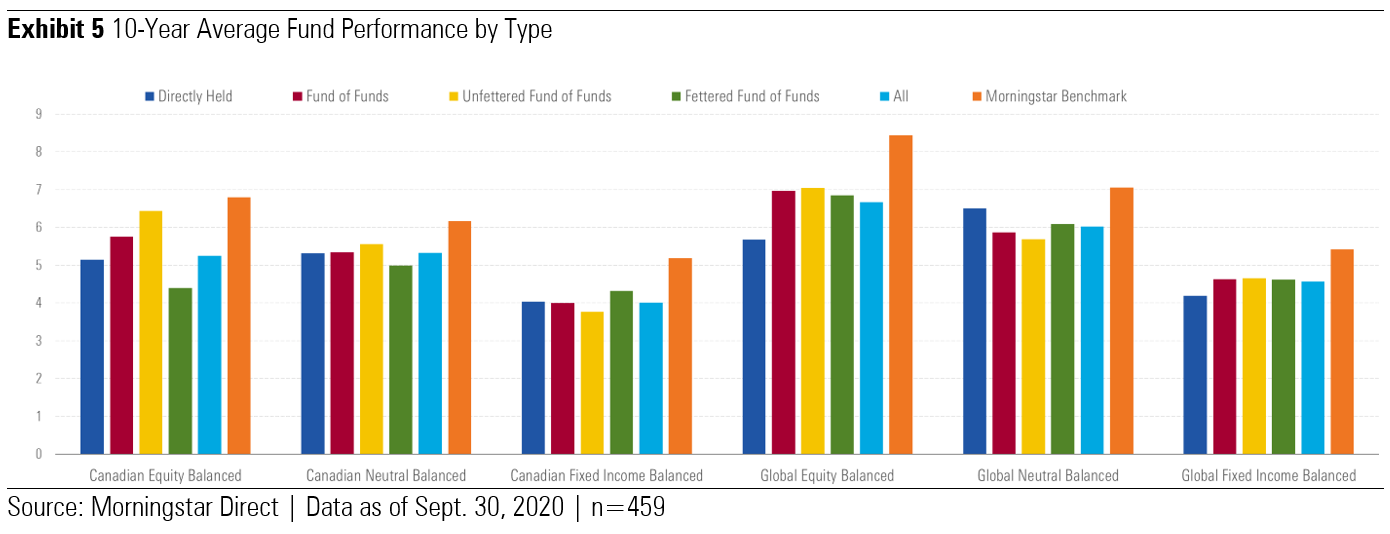

The above chart outlines the performance of the various ‘types’ of target allocation funds over a trailing 10 year period. It can be seen that in four of six categories, unfettered funds outperform their fettered counterparts after fees. In four of six categories, directly held target allocation funds underperformed those that held other funds.

.jpg)