Learn about sustainable Canadian funds here.

On the Rise

The OECD reports that one fifth of professionally managed U.S. assets now invests at least partially on environmental, social, and governance principles. Other sources cite higher figures. Whatever the true amount, ESG’s emergence trails only the growth of indexing as the largest investment trend of the past decade.

That ESG investing has become thoroughly mainstream is demonstrated by the decision of Wharton’s MBA program--traditionally, the Wall Street feeder--to add ESG research to its curriculum. Explains Wharton’s dean, Erika James, “The students are asking for it. We’re going to have coursework and reading material and discussions on corporate social responsibility. We have to ... if we want to continue to be an attractive choice for business school students.”

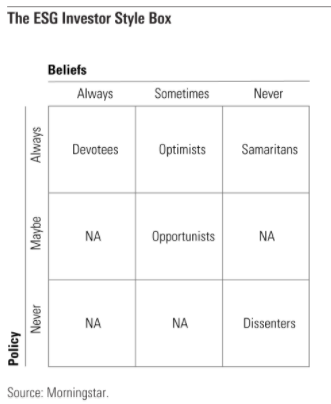

The ESG Investor Style Box

You may be less enamored of ESG principles. That’s fine; choose your own path. The purpose of this column is not to entice you into ESG investing but instead to examine the assumptions that underlie the decision to adopt--or abstain from--the ESG approach.

For this discussion, I’ve modified the familiar nine-grid Morningstar Style Box to create an ESG Investor Style Box. This box depicts nine possible approaches to ESG investing, as measured by an investor’s belief and policy. Belief, portrayed on the horizontal axis, refers to whether the investor thinks that firms that embrace ESG principles will enjoy higher stock market returns. Policy, shown on the vertical axis, illustrates the degree to which the investor is willing to act on that belief.

The labels within each grid refer to the five types of ESG investor (or noninvestor). There are only five such descriptions, rather than nine, because four of the belief/policy combinations rarely occur.

Beliefs: Always

Devotees occupy the upper left corner of the ESG Investor Style Box. They expect companies that observe the best environmental, social, and governance practices to outgain those that do not. For that reason, Devotees are ongoing ESG investors. In their view, owning organizations that score well on ESG measures gives their portfolios a long-term edge.

This strategy need not be a preference. Devotees need not applaud the ESG movement. Indeed, one could land in this style-box grid while deploring the ESG trend, regarding monies that corporations use for ESG activities as squandered opportunities. But if the rest of the world thinks otherwise, then who is the investor to argue? Astute shareholders put aside their personal beliefs, recognize what the marketplace rewards, and then hop along for the ride.

In practice, of course, almost every current ESG Devotee supports the cause. But it’s important to separate investment beliefs, as portrayed in the ESG Investor Style Box, from investment preferences. Beliefs are expectations of future performance to be discarded without regret when the evidence warrants. In contrast, preferences are individual tastes. They need not withstand logic’s test.

The remaining two grids for Always believers, Always/Maybe and Always/Never, are not applicable, because there’s no sense in abandoning ESG investing if the practice consistently works. (To be sure, companies that score well on ESG measures will not excel in every market environment, but per this mindset, the odds will constantly favor them.)

Beliefs: Sometimes

While Devotees believe that investing according to ESG principles produces an ongoing performance advantage, Optimists are not so sure. The Optimist hopes that will prove to be the case, but one cannot know. Perhaps the assets lavished on environmental, social, and governance issues were indeed wasted. Or, perhaps, the investments were once a sound decision, but the stock market has since overpriced that virtue.

This leads to an additional wrinkle: Even if the Devotees are initially correct, they may eventually be wrong. If scoring well on ESG principles improves a company’s business prospects, as, for example, do earning high profit margins or possessing a wide Morningstar Economic Moat Rating, then eventually the ESG attribute may become too popular. As the saying goes, good companies don’t always make good stocks.

Whereas the Optimist recognizes this reality but remains loyal to ESG because of personal preferences, Opportunists respond to the prevailing investment winds. If ESG investing looks to be profitable, the Opportunist will consider that approach. If, on the other hand, ESG-inspired companies do appear to have wasted monies that could have been better spent on improving shareholder value or if their stocks have been overbid, then the Opportunists will stay on the sidelines.

Finally, there’s no description for the Sometimes/Never grid. While it’s possible that an investor might detest ESG investing so deeply as to refuse to participate, even if she believed that doing so would bring higher returns, that seems unlikely. After all, ESG opponents typically argue that the practice is misguided because the sole business of companies, and thus the sole interest of their shareholders, is to accrue profits. Presumably, such investors would not stand on ceremony to refuse gains sourced from ESG practices just because of their personal dislike.

Beliefs: Never

Samaritans willingly forgo profits when they invest according to ESG principles. Whereas Devotees believe that ESG approaches improve corporate fortunes, Samaritans accept the counterargument that organizations post their highest profits, and thus record their highest stock prices, by focusing relentlessly on shareholder value. However, they are willing to accept a lower stock market return in exchange for indulging their personal preference.

This is the old-fashioned view of “socially conscious investing”--that the desire to do good (as the ESG investor sees it) conflicts directly with the desire to achieve stock market profits. Effectively, the investment practice serves as a negative screen, tilting the portfolio toward lower-returning securities. This is a cost that the Samaritan is willing to bear.

In contrast, the final class of ESG investor--skipping past the Never/Maybe grid, which is unoccupied--wants no part of the strategy. For the Dissenters, ESG is an empty movement, full of sound and fury, signifying nothing. It may be that green companies will occasionally outperform because of investor enthusiasm, but that is not the way to bet. Let those who are happy to forfeit returns indulge their desires--the Dissenters will thrive by owning stocks that the ESG enthusiasts will not.