Having cash in your bank account will erode your purchasing power over time. Should you instead use this money to pay down your mortgage or invest in the stock market? The answer to this question depends on your situation. Since no investment solution makes equal sense to all individuals, it is essential to make informed decisions to reach your financial goals.

Here are some general guidelines to help you assess your situation.

-Age and ability to take investment risk are inversely related. The younger you are, the higher your ability to take risk, and vice versa.

-Time horizon and ability to take risk are directly related. The longer the time horizon you have, the higher is your ability to take risk, and vice versa. A longer time horizon increases the likelihood of recouping any losses you might encounter along your investment journey.

-The keyword is "ability" to take risk. Other aspects of your life also influence your ability, e.g., job- and family situation and cash dependence.

-Another keyword is "willingness" to take risk, which relates to, e.g., saving goals, motivation, and preference for risk.

But first, getting rid of any high-interest debt is recommended. According to Morningstar's Director of Personal Finance, Christine Benz, "there's no way you can beat a double-digit return by investing in anything else that's guaranteed."

Establishing an emergency fund is also a recommended action. Experts typically advise having at least three months' salary as an emergency fund. With that out of the way, let's have a closer look at two common alternatives if you have excess cash; pay down your mortgage or invest in the stock market.

Mortgage Down-Payment

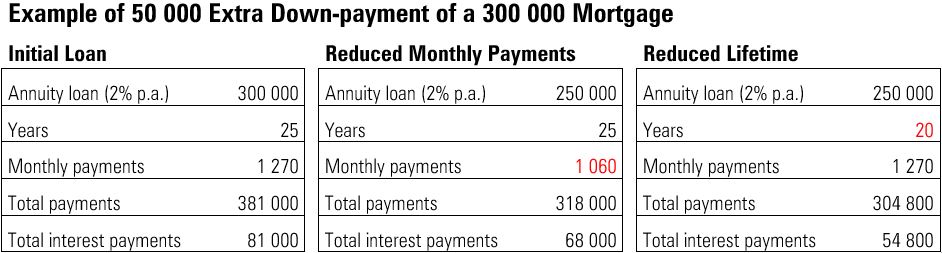

Suppose you have a low ability or low willingness to take risk. In that case, accelerated mortgage down-payments can be a good choice. Reducing the interest-bearing debt increases the likelihood that you can service the debt payments if interest rates rise or if a black swan event enters your life.

An extra mortgage down-payment today will also increase your future disposable income, either by reduced periodic mortgage payments or a reduced lifetime of the repayment schedule.

Additionally, owning a home is often more than an investment because it is an integral part of people's lives. Paying down your mortgage and increasing your home "ownership" can provide a sense of security and satisfaction that can surpass any rational economic argument for investing elsewhere.

As a side note, in case of any large expenses in the near- or mid-term future, having cash in your bank account might be the best option.

Stock Market Investing

If you can earn an expected after-tax return in the stock market that exceeds your mortgage rate, investing in the stock market can be a viable alternative, assuming you have the appropriate ability and willingness to take risk.

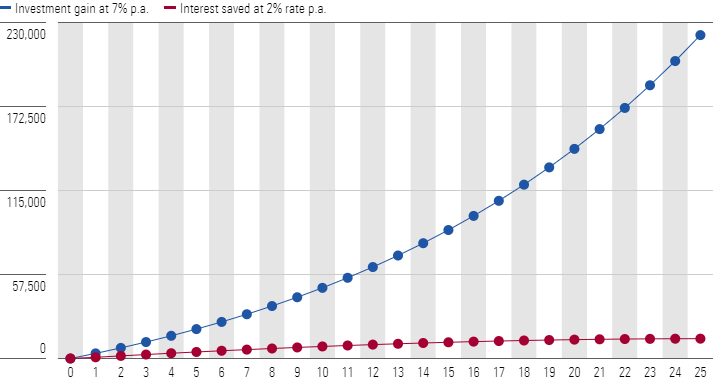

While stock market investing is not risk-free, it usually yields an expected return well above mortgage rates in the long run. What is a "long-run"? Some might say a minimum of five years, and others might say a minimum of ten. The blue graph below illustrates the investment gain over 25 years from a $50 000 stock market investment at 7% annual return. And the red graph illustrates the interest saved over 25 years from a $50,000 down-payment of a 300 000 mortgage with a 2% mortgage rate.

The total investment gain is $221,000. The total interest saved is $13,000. (Down-payment of an annuity loan, from $300K to $250K principal outstanding. 25 years repayment schedule. 2% mortgage rate p.a.).

Before you get FOMO and go YOLO on your cash reserves, consider the risks associated with stock market investing.

-Negative return risks: Everything that can influence your investments to drop in value, e.g., market risks and company-specific risks.

-Human risks: Everything related to your decision-making, including emotions and biases. Words of wisdom such as "Buy low, sell high" and "Be fearful when others are greedy, and be greedy when others are fearful" are easier said than done. Developing diamond hands is not for the faint-hearted, but it can serve you well in the long run. As studies have shown, time in the market beats timing the market.

Focus on Your Situation

Using extra cash to pay down your mortgage or invest in the stock market comes with its pros and cons.

Paying down your mortgage can protect against rising interest rates, reduce any psychological debt burden, and increase your disposable income in the future. One potential drawback of accelerated down-payments is the potential opportunity costs associated with forgone investment alternatives.

Investing in the stock market will likely increase your overall portfolio risk and expected return. Because no individual likes to lose money, remaining invested in the stock market - especially in down markets - requires a strong mindset. You can reduce the portfolio risk through diversification and by applying a long time horizon.

Keep in mind that no investment solution makes equal sense to all individuals. What is ideal for you might be quite different from what is suitable for your friends, neighbours, or colleagues. Filter out the noise, focus on your situation, and make informed decisions so you can reach your financial goals.

This article does not constitute financial advice. It is always recommended to speak with a financial professional or advisor before buying or selling mutual funds/ETF’s or securities.