In view of the outstanding performance of the Nasdaq 100 Index in recent years, more and more investors from Europe are flocking to funds and ETFs, like QQQ, that are oriented towards or track the US stock market barometer. But what are the distinguishing characteristics of this index? In the following Q&A we provide facts and figures to clear up common misperceptions.

The Nasdaq 100 is a selection index of the largest US technology stocks, isn’t it?

Put this way, this statement is not true. In the media and among investors, the Nasdaq index is often referred to as the "technology” or even the “computer stock market". This is a misunderstanding that goes back to the origins of this market segment. "Nasdaq" stands for National Association of Securities Dealers Automated Quotations (own emphasis). Founded in 1971, Nasdaq was the world's first fully electronic trading platform, a computer exchange -- but not a market where only computer or technology stocks are traded. Moreover, in the 1990s, "technology" and "computer" companies were often used interchangeably, perpetuating this misunderstanding. In short, the index often brings together growth companies that opted for a listing on the Nasdaq and not on the NYSE. The best-fit description would be that the Nasdaq is a market segment that contains a big bunch of fast-growing companies.

So which stocks does the Nasdaq 100 Index bring together?

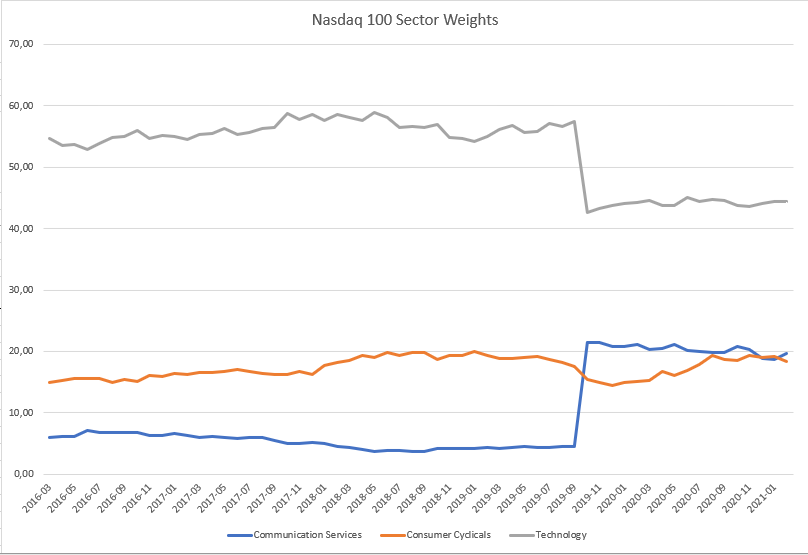

The index reflects the performance of the 100 largest non-financial stocks listed on the U.S. stock exchange of the same name. This brings us to one of the index's shortcomings: it excludes banks, and energy, commodities and real estate are typically not included. Industrials also make up but a minuscule share of the index. This leaves the technology, telecommunications and consumer cyclical sectors, which are weighted at 44 percent, 20 percent and 18 percent respectively. Health care stocks and defensive consumer stocks follow at a considerable distance, each accounting for between four and six percent of the index weight. The Nasdaq 100 Index is thus not sufficiently diversified at the sector level to qualify as a representative index for US stocks. It is also very top-heavy, with the largest ten stocks accounting for over 50 percent of its weight.

If consumer cyclicals and telecoms make up a large share of the Nasdaq 100, that sounds more like old industries rather than growth companies.

This is another common misperception. The MSCI and S&P industry classification rules were modified in 2018. This led to a reclassification of quite a number of technology companies which were stamped as telecoms and consumer stocks. Accordingly, the weight of the technology sector declined from just under 60 percent to just over 40 percent. The weighting of telecoms and consumer goods stocks increased accordingly, but this did not reflect a restructuring of the index. (See the chart below). Since 2019 Amazon.com and Tesla are classified as cyclical consumer stocks; Alphabet and Facebook are now counted as communications service providers und

So the Nasdaq 100 index is not a representative, market-wide index?

So the Nasdaq 100 index is not a representative, market-wide index?

Correct. It has a large imbalance at the industry level and also at the individual stock level. Even though there is now a hot debate among investors in the U.S. as to whether the S&P 500 has not become too tech-savvy, it is still a representative market barometer for US large-cap companies – as are the MSCI USA and the Russell 1000. Speaking of a representative market index, another shortcoming of the Nasdaq 100 is that it only includes companies listed in a specific market segment. From this point of view, it has no claim to representativeness in its own right.

What could be the function of a Nasdaq 100 tracker in the portfolio context?

Clearly only as a satellite and not a core holding. But what is the nature of this satellite? Now it starts to get complicated. The question is not easy to answer because, on the one hand, it is too concentrated for an index that is representative of the US equity market. On the other hand, it is not concentrated enough for a technology sector index. There are much purer plays in the technology fund space which not only track U.S. technology stocks but rather global technology companies which seems like a preferable option for European investors. An alternative could be thematic funds which play on the technology theme. While these funds tend to be highly risky, they do allow much more targeted exposures to larger and smaller technology stories than the Nasdaq 100.

As an investment case, this index is an anachronism. Its appeal largely stems from the gargantuan performance of the last decade, when unique constellations came into play: Falling interest rates, which favoured fast-growing companies; the underwhelming performance of financial, commodity and energy stocks, which are virtually absent from the Nasdaq 100 - and, most importantly, the outperformance of technology stocks. Investors must ask themselves whether this constellation will necessarily repeat itself in the next ten years, or whether other conditions might not prevail. In view of the discussion about regulating or even breaking up powerful tech platforms such as Alphabet or Facebook and the increasing tendency of governments to tax global corporations such as Amazon more effectively, question marks should be added here. As we speak, Nasdaq 100 trackers are currently having a rough ride when compared to U.S. value and small cap stocks which had been out of favour until well into the fourth quarter of 2020.

Capture Opportunities in Technology

Learn about the Morningstar Exponential Technologies Index here

.jpg)