Of the market timing strategies known to investors, “Sell in May, Go Away” is often mentioned, not only because of its catchy rhyme but perhaps also because of its appealing nature. Wouldn’t it be nice to go up North for the Summer and not worry about your investments? To its credit, the strategy was founded on some logic: during the Summer months as investors are less active, trading volumes fall, as does enthusiasm for the market and hence potential for gains. There is also a bit of truth to the concept if you look at the historical returns in Canada.

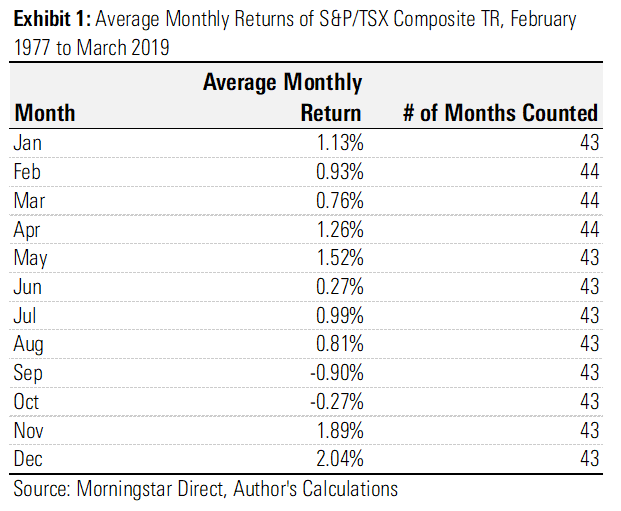

On average, over the last 43 years, the months of June, September, and October do tend to have lower returns than other months. A common version of the “sell in May, go away” strategy is to go to cash on May 1st, and then buy back into the market on November 1st. Being in cash during these lower return months might on the surface appear like we are focusing our efforts solely on the months with historically higher returns. However, this is where credibility to this strategy stops.

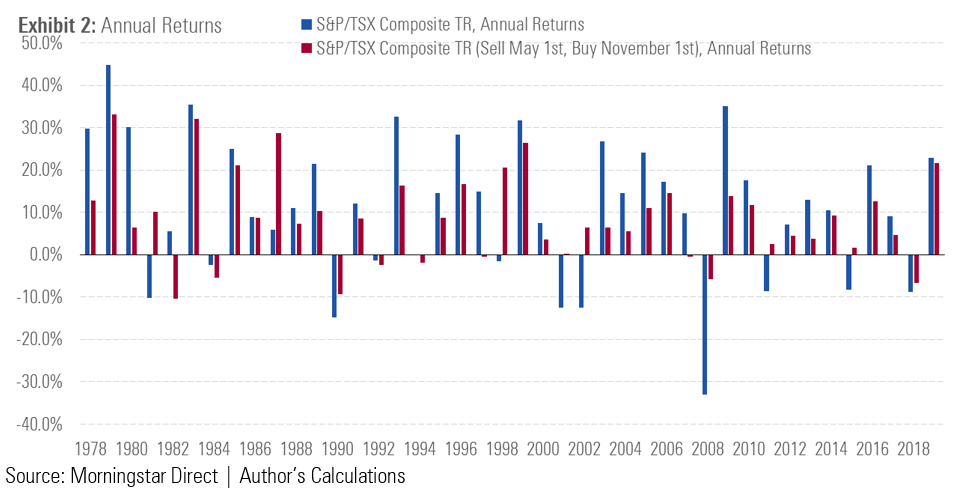

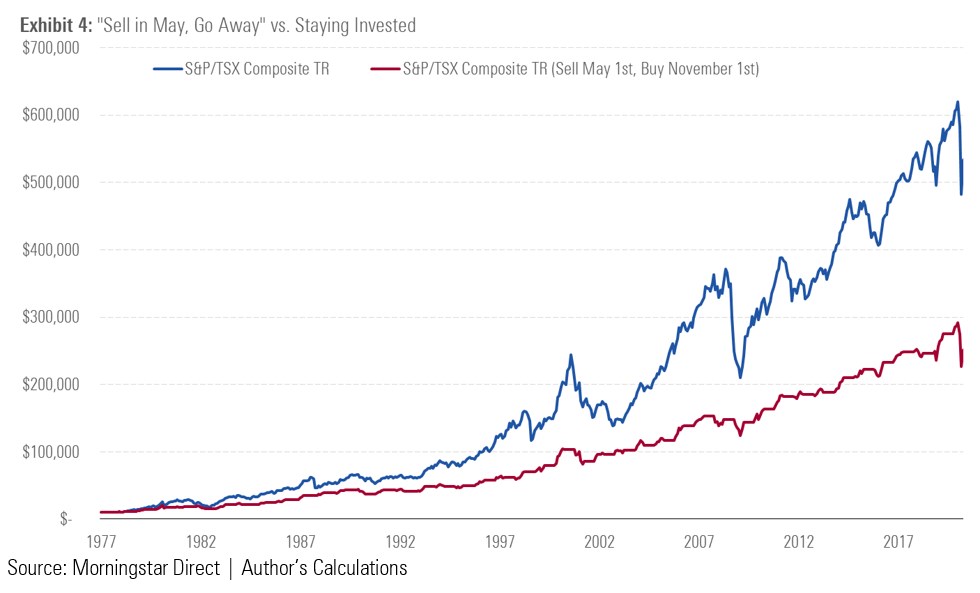

Aesop’s fable of the grasshopper and the ant applies here in full force. Those that “go away” during the Summer simply lose out over the long term. Case in point, here is the performance of the S&P/TSX Composite index against itself, removing the performance of the index between the months of May to October, inclusive. The idea is to illustrate what happens if an investor were to go to cash at the end of May and then buy back into the market on November 1st.

We’ve highlighted in blue the annual returns of the index, and in red the returns of the “Sell in May, Go Away” strategy. Though not a failure, it was found that most of the time, leaving the market in May and then returning in November affords a lower return than staying invested.

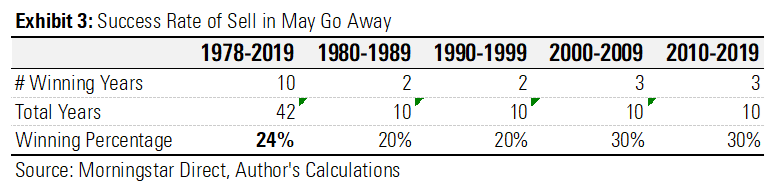

If we were to look at the number of times this strategy beat the index, the stats go further in highlighting the performance. Over the past four decades, there were ten calendar years where the “Sell in May, Go Away” strategy performed better than staying invested. That figure stays more or less consistent within each decade in isolation. In the 1980’s there were two years where the strategy beat the index, in the 2000’s there were three. Regardless of which decade we look at, the strategy does not do the investor any favours.

Finally, we look at the effect of compounding; a core financial concept that is imperative to the success of investors. Had an investor started with a $10,000 investment in the index in 1977 and applied the “Sell in May, Go Away” strategy, they would find themselves with $280,000 CAD less than someone who simply stayed invested the entire time.

All this said, it is important to echo that for retail investors, timing the market rarely affords better returns. Though technical analysis techniques exist that dive deep into investor behavior, these concepts require a great deal of attention and skill to execute consistently and successfully. The market is generally efficient, and investors can expect that any systemic opportunities are quickly arbitraged away by professionals. For retail investors, keeping true to risk tolerance and having a realistic expectation of returns will lead to a better path to financial success over the long term.

This article does not constitute financial advice. It is always recommended to speak to an advisor or investment professional before investing.