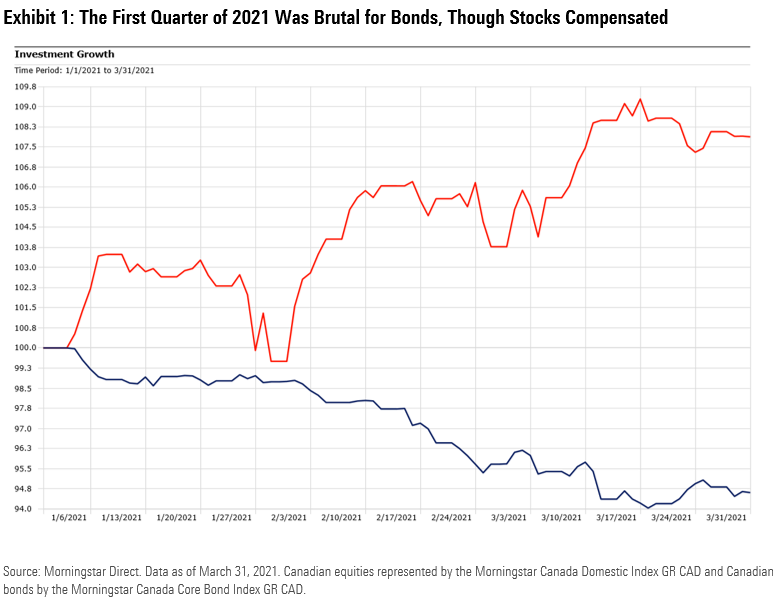

"Don't own bonds." The blunt warning from hedge fund guru Ray Dalio in November 2020 looks obvious in retrospect. Rock-bottom interest rates designed to stimulate pandemic-stricken economies had nowhere to go but up. In early 2021, Canadian 10-year Treasuries nearly doubled—from roughly 0.80% to 1.5% in just two months. The yield on the 10-year U.S. Treasury rose from 1.0% to 1.7% over the same span. Those rising yields undermined bond prices, including a long-term Canadian federal bond that lost 13% of its value in the first quarter of 2021.

As a result, core bond portfolios took it on the chin. As displayed in Exhibit 1, the Morningstar Canada Core Bond Index, which represents the investment-grade credit market for Canadian fixed-income investors—including debt issued by federal and provincial governments, corporates, and government-guaranteed entities like the Canada Housing Trust—lost 5.4% of its value in the first quarter of 2021. Meanwhile, the Morningstar Global ex-Canada Core Bond Index declined 2.6% in Canadian dollar terms. Those are steep short-term losses for an asset class that is considered relatively safe. Meanwhile, equities rallied.

What triggered such bad times for bonds in early 2021? The answer: good times for the global economy and other assets. With COVID-19 vaccines rolling out, societies reopening, the global economy recovering, and monetary and fiscal stimulus flowing, inflation expectations have grown. Risk assets have boomed—not just equities but celebrity special-purpose acquisition companies, nonfungible tokens, cryptocurrencies, and other speculative investments. Markets are in "risk on" mode.

Dalio's 2020 warning was clearly right from the perspective of tactical asset allocation, but bonds still have merit as a long-term strategic portfolio building block. Regular coupon payments hold appeal for investors of all sizes, from retirees to asset owners looking to match future known liabilities. Bonds counterbalance the risk of equities and serve as portfolio ballast, especially useful during times of market stress. When fixed-income strategies lose money, their drawdowns tend to be far milder than those of stocks. That especially true of high-quality bonds and less so for high-yield corporate bonds and emerging-market debt, which behaves far more like equities.

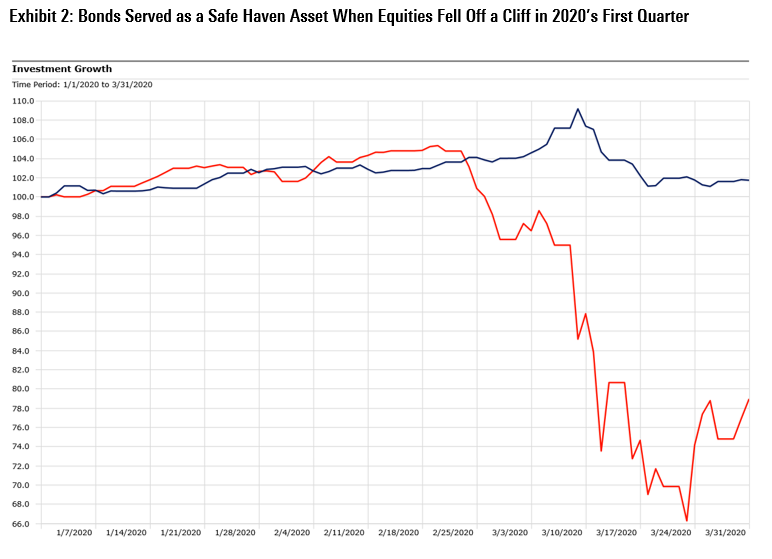

Recall the experience of the first quarter of 2021, when COVID-19 pandemic panic gripped markets. Panicking investors rushed the exits of global equity markets across the board. Bonds served as a safe haven.

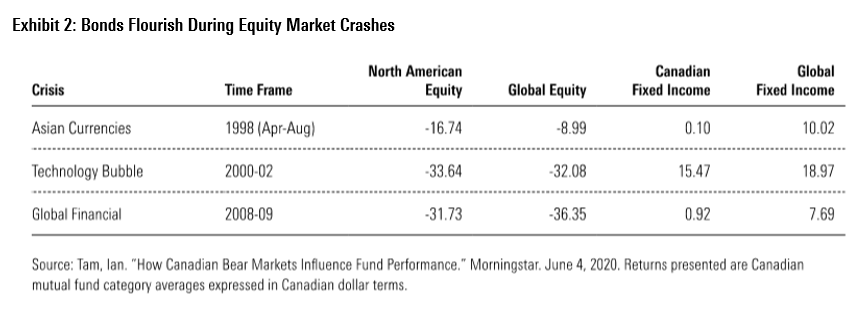

The pattern of bonds holding up during a crisis is consistent with a long-running trend. In a study of asset class behavior during bear markets, Ian Tam, Morningstar Canada's director of investment research, examined a series of equity market crashes over the past 25 years using Morningstar mutual fund category averages. As displayed in Exhibit 3, Tam observed that Canadian fixed income and global fixed income were incredibly resilient as stocks were selling off, often gaining significant ground in flights to safety.

It's important to note that bonds have been maligned for years for their low yields. In the years after the global financial crisis, bonds were dismissed as "return-free risks." More than one pundit warned investors away from bonds, as Dalio did in November 2020. Strong equity market returns in the decade after 2009 left many less experienced investors wondering why they would ever own anything other than stocks in a portfolio. And yet, bonds cushioned equity market losses in 2015 and 2018. Consider the divergent performance of stocks and bonds in calendar 2018:

- Morningstar Canada Domestic Index (equities): -8.7%

- Morningstar Canada Core Bond Index: 1.3%

- Morningstar Developed ex-North America Index: -5.7%

- Morningstar Global ex-Canada Core Bond Index: 1.2%

When the 2020 pandemic-driven bear market came around, bonds also did their job. They diversified equity market risk, damped volatility, and preserved capital. That's an especially useful function for risk-averse investors, including those who have moved from the accumulation to decumulation stage of life. Despite their losses in the first quarter of 2021, bonds' struggles were more than offset by a strong quarter for equities. Investors holding a classic 60/40 stock/bond portfolio were in positive territory.

What About Bonds Going Forward?

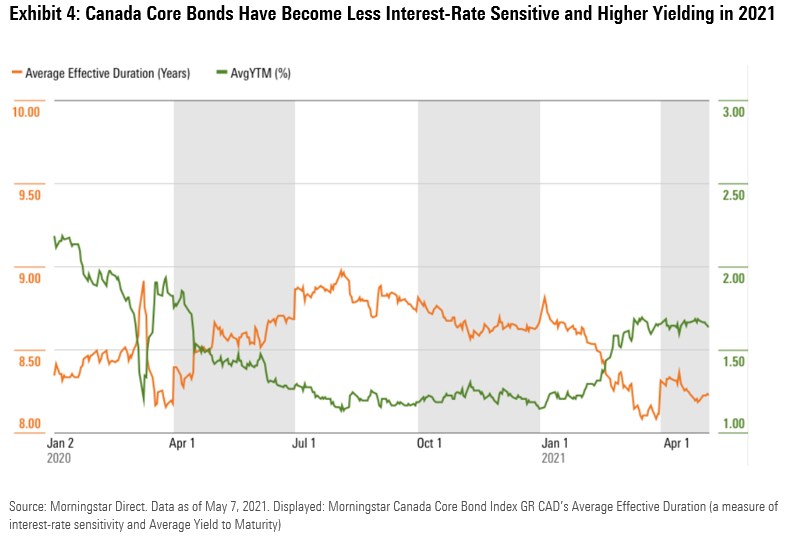

In the near term, investors have reason to be more optimistic about bonds now than in the fourth quarter of 2020. As rates rise, the duration and sensitivity to changes in interest rates fall. As displayed in Exhibit 4, the effective duration of the Morningstar Canada Core Bond Index has already started to dip from its high in January 2021 as a result of increased rates. The duration is still significantly longer than 10 years ago, but each basis point of higher interest rates should be less painful than the one before it. Meanwhile, yield has increased, which bodes well, given that yield is an important contributor to the total return from fixed income. These same things are also true of the Morningstar Global ex-Canada Core Bond Index.

Bonds Earn Their Keep

The first quarter of 2021 shows that high-quality bonds are capable of losing money over short periods. But the 5% decline for the Morningstar Canada Core Bond Index—unusually severe for fixed-income assets—is a far cry from the 20% decline that equities have repeatedly shown themselves capable of experiencing. Paul Kaplan, director of research with Morningstar Canada, identified 18 bear markets (20% decline or more) over 150 years of U.S. equity market history—an average of one crash every eight years.

The correlations between stocks and bonds move around. Investors shouldn't overemphasize correlations, though. While short-term correlations are changeable, they become more stable in the longer term. Bonds’ ability to zig when stocks are zagging is especially useful when markets are in “risk-off” mode.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VYKWT2BHIZFVLEWUKAUIBGNAH4.jpg)