%20(1).jpg)

With Russia continuing to wage war on Ukraine, international sanctions against the country continue to mount. This in turn raises issues for investors holding Russian-domiciled assets. Dominant stock index providers such as MSCI and Russell have removed Russian companies from their indexes, numerous asset managers have pledged to ban Russian investments on a firm-wide basis, and Russian bonds have been downgraded to junk at Moody’s, Fitch and S&P. (DBRS Morningstar does not rate Russia.)

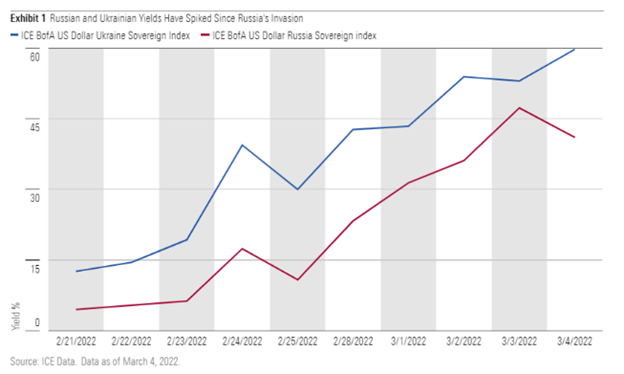

As a result of all this, many predict Russian bond defaults, and so, Russian and Ukrainian bond yields have spiked. While all this may not seem to be an immediate concern for Canadian investors, the fact is that Canadian bond investors are not immune to direct and peripheral impacts of a Russian default.

Source here.

Over the last five years, assets in Canadian-domiciled emerging market debt funds have increased over 100%. The asset class, however, remains a relatively niche space in our market. Of the 3385 oldest surviving mutual funds in the Morningstar Direct Open-Ended Fund Universe only 15 emerging market debt strategies were identified, most of which have less than 10 years of history.

Whatever the reasons for this, Canadian emerging market fixed income investors are relatively underexposed to Russian bonds. As of the end of February 2022, the Canada Emerging Markets Fixed Income peer group has an average exposure of only 1.71% to Russia, vs a 1.84% exposure held in the JPMorgan GBI-EM Global Diversified Index. Using data available at the time of publication, only 5 funds held more exposure to Russian bonds than the Index, with Sunlife Amundi Emerging Markets Debt being most exposed at 5.30%.

Note: The latest available data for many of these funds is January 31st, 2022. The data for the index is as of February 2022.

Canadians also tend to seek international fixed income exposure via global fixed income and high yield funds where investors have their choice of 215 strategies. At least 10 strategies in this category have more Russian bond exposure than the Emerging Market Debt benchmark, including the silver rated (based on the Morningstar Quantitative Rating), Pimco Monthly Income Fund. Pimco indicated that it is not adding exposure to Russian securities in its actively-managed mutual funds and separately managed accounts at this time.

Note: The latest available data for many of these funds is January 31st, 2022. The data for the index is as of February 2022.

Meanwhile, Canadian investors have been actively withdrawing from emerging market fixed income funds. Overall fixed income funds saw net inflows in January and February, but three fixed income categories saw net outflows. Emerging market debt saw approximately 40% of outflows.