Commitments to mitigate climate change are more ubiqitous than ever, and companies, asset managers and governments have been at the forefront over the last year.

President Biden rejoined the Paris Agreement on his first day in office, the Net Zero Asset Managers Initiative gathered steam, and milestone gatherings such as COP26 sought to catalyse global collaboration to address the climate crisis.

At the same time, the market saw increasing demand from investors who want to take climate action in their portfolios. Climate change poses the biggest long-term threat to our future, and will impact not just how we invest, but how we live.

Some of the dangers for investors include transition risks, which arise with the shift to a low-carbon economy, such as changes in regulation, technology, and consumer behaviour.

Then there are also physical risks, which threaten companies' supply chains, operations, and assets as, say, increasingly extreme weather events buffet businesses. That could be flooding. It could also be hurricanes or earthquakes.

Climate change presents opportunities for investors too, though. Through their portfolios, investors can gain exposure to companies developing innovative solutions to mitigate the damage, such as carbon capture technologies.

In our recently released report Investing in Times of Climate Change, we dig into the global landscape of climate-focused funds, map out the products that fit into each broad type of climate strategy, and demonstrate the growth in climate funds across different markets.

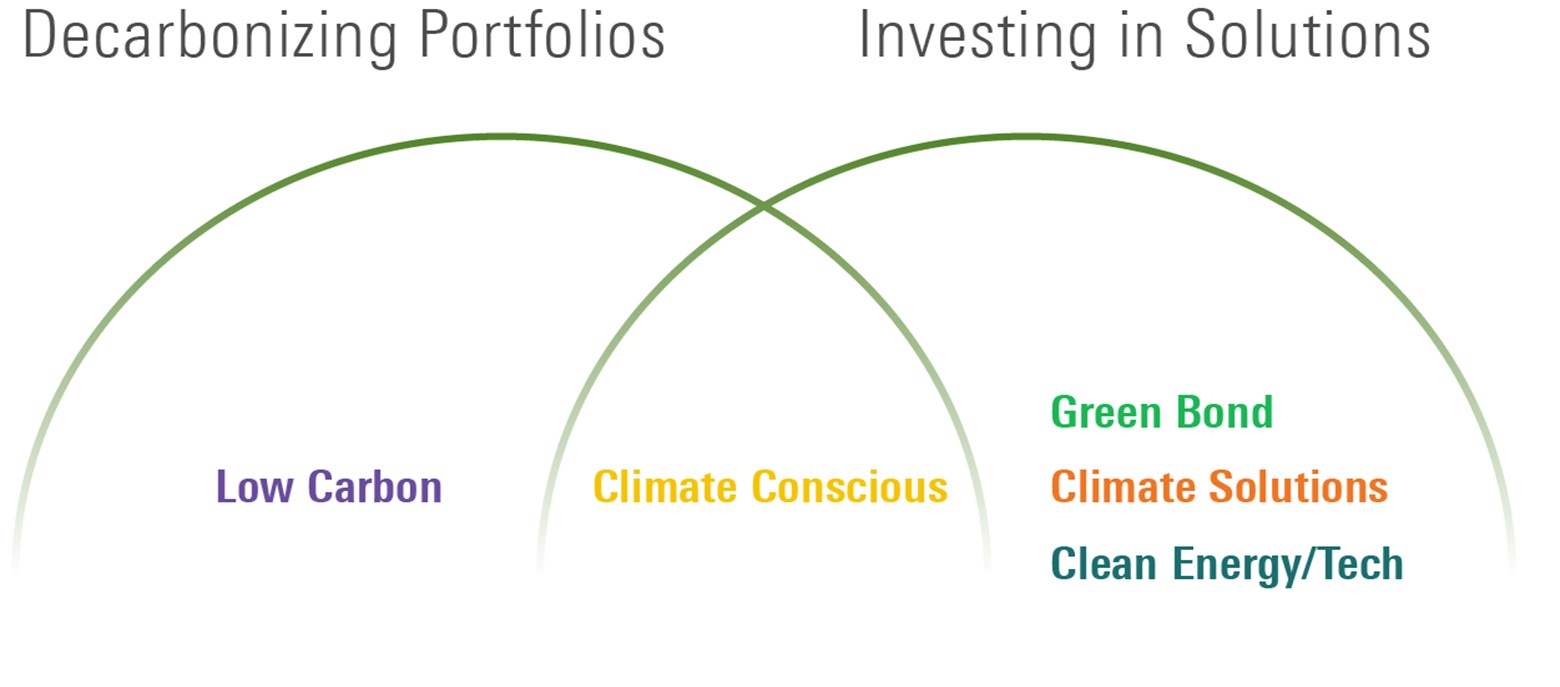

This universe of climate funds comprises a wide and growing range of strategies that aim to meet different investor needs and preferences. To help investors navigate what can be a confusing mix of offerings, we subdivide the universe into five mutually exclusive categories, shown in the exhibit below.

Low Carbon and Climate Conscious funds tend to focus on reducing climate-related risks in portfolios (decarbonising portfolios) and investing in companies that positively align with the transition to a low-carbon economy.

On the other hand, Green Bond, Climate Solutions, and Clean Energy/Tech funds target companies whose products, services, or projects directly or indirectly address climate challenges and opportunities.

In our research, we also highlight the role each climate fund category might play in an investor’s portfolio. For example, funds that invest in climate solutions typically carry certain risks – such as sector concentration – that make them more suitable as satellite holdings rather than part of a core allocation in a diversified portfolio, for which low carbon or climate conscious funds may be more suited.

Additionally, we outline the various sustainable-investing approaches in use by climate funds and explore how well fund portfolios match their climate ambitions using multiple Morningstar metrics.

Enter China

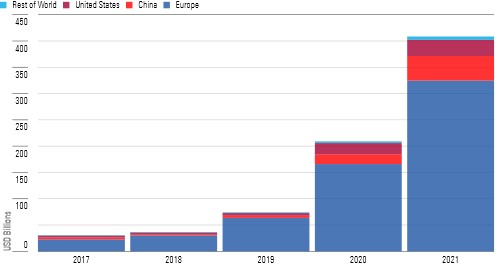

On a global scale, as of December 2021, there were 860 climate funds that fit our definition, with collective assets under management of US$408 billion worldwide. Global assets have doubled in one year, boosted by continued fund flows and an accelerated pace of product development.

Unsurprisingly, given its greater commitment to a climate agenda, Europe remains the largest and most diverse climate funds market, followed by China, which for the first time last year overtook the United States as the second-largest climate funds market.

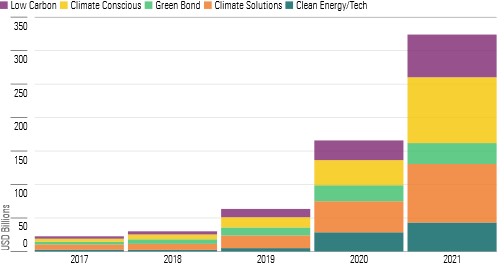

Fuelled by higher investor interest in climate issues and by regulation, assets in European climate funds doubled last year to US$325 billion.

The years 2020 and 2021 were pivotal for sustainable investing in Europe with the rollout of two groundbreaking classification and disclosure regulatory frameworks as part of the European Union’s Action Plan on Sustainable Finance: the EU Taxonomy and the Sustainable Finance Disclosure Regulation, or SFDR. Both initiatives have had a ripple effect across multiple areas, including climate investing.

The accellerated asset growth can be attributed to the increased inflows of money into two types of climate funds: climate solutions and climate-conscious funds. Over the year, flows into the European climate fund universe amounted to an all-time high of more than US$108 billion, up 61% from the previous record in 2020.

These strong flows accompanied rapid product development, with the launch of 151 new climate funds and the repurposing of 52 more in Europe last year (shown below).

Climate-conscious strategies represented almost half of the new launches. Climate conscious funds tilt toward companies that prioritise climate change in their business strategies and are therefore better positioned for the transition to a low-carbon economy.

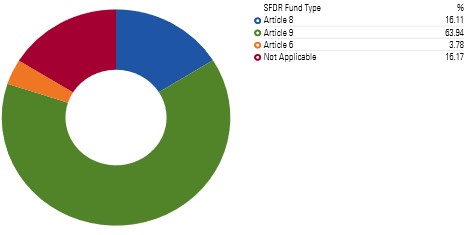

At the end of 2021, Article 9 funds dominated the European climate fund landscape, with US$208 billion (almost 64%) of the assets. Climate funds classified as Article 8 funds accounted for US$52 billion, or 16% of the universe.

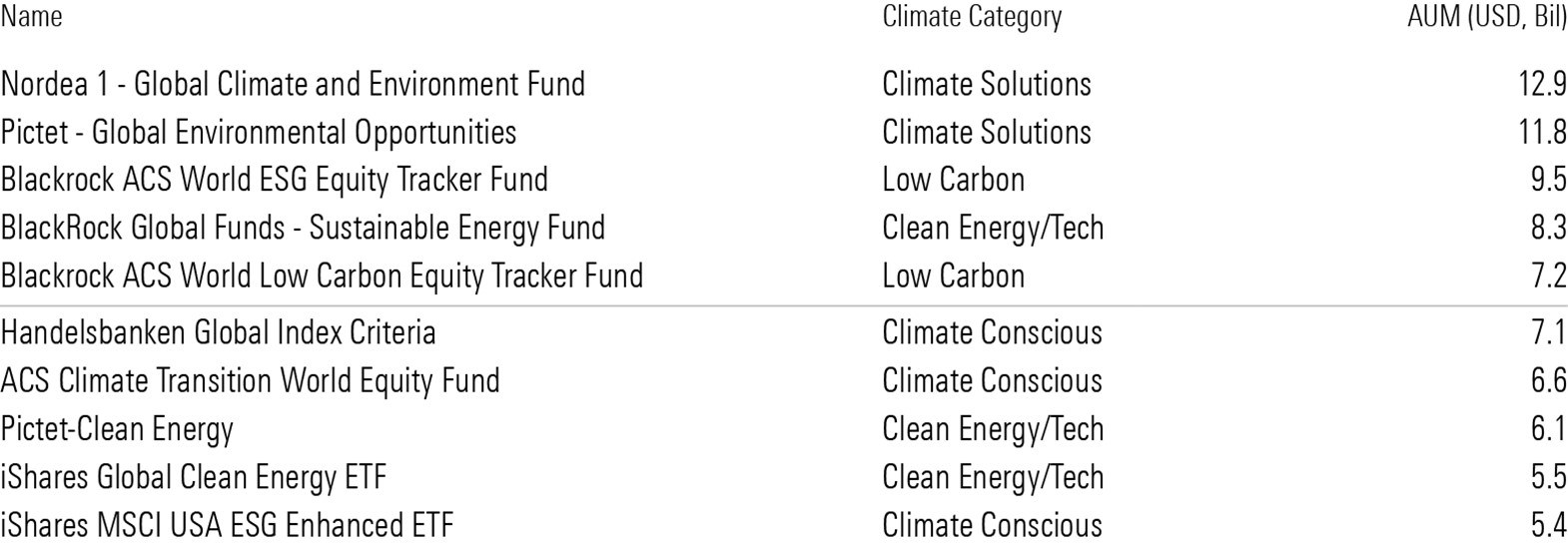

The exhibit below shows the 10 largest climate funds in Europe at the end of 2021. Among these, three were newcomers: BlackRock's ACS Climate Transition World Equity Fund, Handelsbanken Global Index Criteria (which switched to track a Paris-aligned benchmark in May 2021) and iShares MSCI USA ESG Enhanced ETF, which converted a climate-transition benchmark in December.

These newly-created EU climate benchmarks are designed to consider both climate risks and opportunities, and to match the transition to a climate-resilient economy by ensuring a yearly decarbonization target of at least 7% (in line with the decarbonisation trajectory of the IPCC's 1.5˚C scenario.

The Situation Stateside

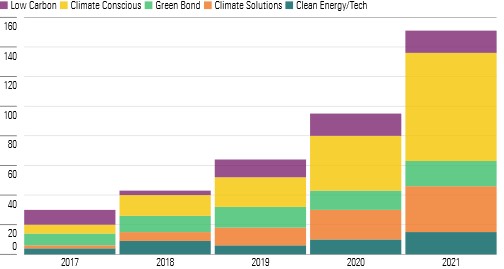

US climate funds experienced tremendous growth last year, with assets in these funds passing the US$30 billion mark. As shown below, this represents a 45% increase over the previous record in 2020 and is nearly nine times the total seen five years ago.

While Clean Energy/Tech funds retain the majority (61%) of these assets, other categories are gaining ground. As shown below, climate solutions funds grew by 116% to US$4.5 billion in assets at the end of 2021, followed by low carbon funds (142%, $3.4 billion). Equally noteworthy is the climate conscious category, which made its debut in the US only last year.

China Rises

For the first time, China overtook the United States as the second-largest climate funds market last year. As shown below, China’s universe of climate funds more than doubled in size to US$46.7 billion, representing a 149% increase compared with the previous year.

The rapid expansion of China's climate fund market can be explained by the heightened focus on climate change and other environmental issues in the ruling party's agenda for economic transformation.

In February 2021, the State Council announced guidance to support the establishment of "a sound economic system with green, low-carbon and circular development, and promoting eco-friendly economic and social development in all respects.” In March, the government proclaimed goals including: "peaking carbon dioxide emissions before 2030" and "reaching carbon neutrality before 2060."

Against this backdrop, energy transition, energy efficiency, and circular economy feature prominently in the development of climate-related financial products and services in China, including carbon credit and the first national emissions-trading system. The evolution of related regulatory frameworks will likely bring forth more structural changes to the Chinese fund market.

You, The Investor

Despite the tremendous growth seen in climate investing and commitments over the past few years, it is increasingly clear that we need to see faster and more widespread action.

In its latest report, the IPCC warned the window of opportunity to take any meaningful climate action is rapidly closing. Worldwide emissions must fall by half by 2030 and reach net zero by 2050 to have any chance at keeping global temperature rise under 1.5°C. Ultimately, global cooperation between governments is required to address the full scope of this threat, but the private sector and investors can be part of the transition, too.

On the one hand, climate change represents an investment risk that ought to be accounted for in portfolios. On the other hand, investors increasingly have access to innovative climate solutions through opportunity-seeking climate funds. Last but not least, on behalf of investors, asset managers should engage with companies via active ownership and proxy voting to advocate for robust climate strategies.

In this rapidly-evolving space, it is even more important that investors do their homework. Because many climate funds have a relatively short history, with most launched in the past couple of years, their performance can be hard to assess. Still, investors should understand the funds' investment objectives, portfolio construction processes, and expected outcomes.