Spring is once again in the air. With much of Canada cautiously opening for the Summer, the age-old adage of “Sell in May, Go Away” might again cross investors’ minds, especially in light of recent market volatility spurred on by inflation, rising interest rates, and ongoing geopolitical tensions in Europe.

This might make sense – especially if you subscribe to the idea that markets are seasonal. When we look at the data, there is some truth to this.

Looking at the last 45 years of returns data for the S&P/TSX Composite (TR) Index and averaging out monthly returns, we can see that the months of June through October have historically showed lower average returns than other months. On the surface, selling on May 1st then re-buying back into a portfolio on November 1st (a commonly cited approach), might make sense. But here’s where it goes awry:

When we further look at full annual returns since the late 70s, we can see that most of the time, staying invested the whole year affords better results in the calendar year compared against the tactical choice of selling the portfolio in May and re-buying in November (conservatively assuming no transaction costs at all). Moreover, when we tally it up, we can see that in each decade in isolation, “Sell in May, Go Away” is not a winning formula. In the illustration below, we took a look at the # of years where the strategy outperformed simply staying invested. Over the last 4 decades, the strategy simply hasn’t done the investor any favors.

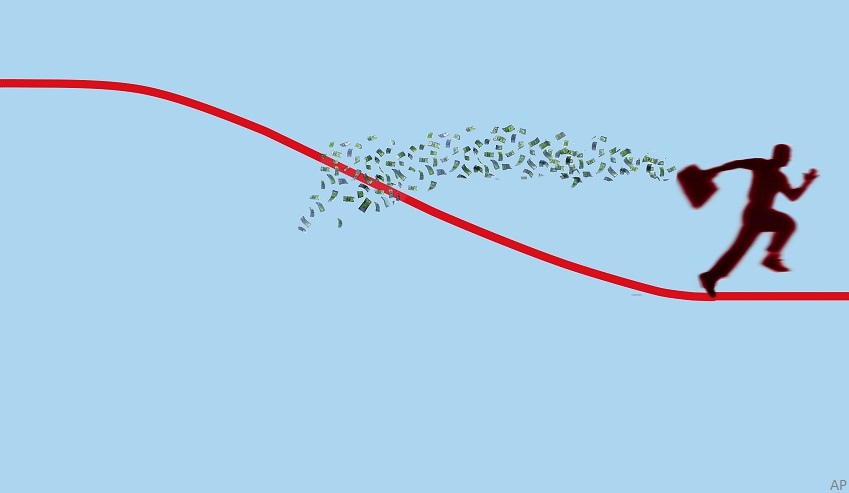

Perhaps the most powerful argument against doing so is when look at the effects of compounding. When you pull your money out of the market, the magic of compounding returns disappears. This is best illustrated in the below chart, comparing a consistent application of “Sell in May, Go Away,” against the index itself.

Simply staying invested in the index affords an investor a vastly larger amount of wealth at the end of the 45-year period. A conceptual 10,000 investment into the index in 1978 would be worth about 480,000 more today than the “Sell in May, Go Away” strategy.

Some might argue that this time is different, given recent events and the evolution of the market. This may be true, but for experienced and average investors alike, timing the market is an incredibly difficult task, with little guarantee of success.

What Can I Do Instead?

If choppy markets are making you nervous, perhaps revisiting how much risk you can comfortably take on and re-jigging your asset allocation (mix between stocks and bonds) might be worth your time as opposed to making tactical moves in your portfolio.

Additionally, regularly re-balancing your portfolio to ensure that this asset mix is in line with your risk profile is a much more productive use of your time. Moreover, rebalancing your portfolio naturally averages out the price you pay for each security. During the rebalancing process, you are buying more of securities that have fallen in price (averaging down your cost basis), and selling securities that have risen in price (taking some profits).

This article does not constitute financial advice. It is always recommended to conduct one’s own research before buying or selling any security.