We’ve lowered our U.S. GDP forecasts for the near term and increased our forecasts for later years. Overall, since our last update, we reduced our forecast through 2025 by 70 basis points, which is mainly attributable to our reduced population forecasts.

The delayed cadence of the economic recovery is driven by worsened supply-side shocks, along with the Federal Reserve’s heightened determination to curb inflation by tightening monetary policy. The Ukraine war shows no signs of abating, and the supply-side impact is exacerbated by increased prospects of a European Union embargo on Russian oil. Although the United States is not a net importer of energy, the recent surge in energy prices will hit the purchasing power of ordinary households.

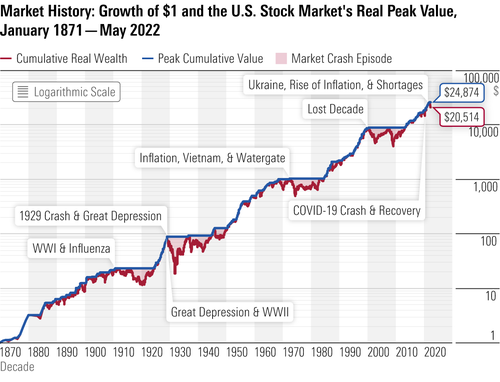

- U.S. Bureau of Economic Analysis, Bloomberg. Data as of May 17, 2022.

Inflation in 2022 Staying Hotter for Longer Than Expected

Likewise, we now expect higher inflation for 2022 but lower inflation in later years. Near-term oil prices are surging, but our 2025 oil price forecast of $55 per barrel is unchanged. Relief from the spike in prices for autos and other durable goods also looks to be slightly delayed. We’ve more carefully factored in expectations for housing’s contribution to inflation, which will peak in 2022-23, in our view.

- U.S. Bureau of Economic Analysis, Bloomberg. Data as of May 17, 2022.

We’re More Bullish Than Consensus on Long-Run GDP

Our GDP forecasts for 2022 and 2023 are about in line with consensus, which has also lowered its forecasts a good deal recently. But we differ greatly with consensus in the longer run. Altogether, we expect a cumulative 250 basis points more real GDP growth through 2025 than consensus does. Consensus remains overly pessimistic on recovery in the labor supply and has generally overreacted to near-term headwinds. We expect a growth rebound in 2024 as the effects of supply shocks fade, with the Fed providing support by backpedaling on monetary tightening as needed.

- U.S. Bureau of Economic Analysis, Bloomberg. Data as of May 17, 2022.

We Expect Inflation to Fall Much Faster Than Consensus

On inflation, our views diverge sharply from consensus, especially after 2022. Bond market breakevens imply a similar view as consensus on inflation.

While consensus has largely given up on the idea that inflation will be transitory, we still think most of the sources of today’s high inflation will abate (and even unwind in impact) over the next few years. This includes energy, autos, and other durables. Combining these factors with tightening monetary policy, we expect inflation to undershoot 2% in 2023 and 2024. Worries about inflation broadening out into the rest of the economy (including via high wage growth) look overblown.

- U.S. Bureau of Economic Analysis, Bloomberg. Data as of May 17, 2022.