Finally, a Proper Inflation Hedge!

Professional investors immediately took U.S. Treasury Inflation-Protected Securities seriously. While the mom-and-pop counterparts to TIPS, Series I Savings Bonds (also known as I Bonds, or inflation bonds), attracted a mere US$360 million during their first full year of operation, TIPS received US$31 billion when they debuted, in 1997. Last year, the U.S. Treasury issued US$186 billion worth of TIPS, thereby pushing the outstanding balance of TIPS to almost US$2 trillion—5 times more than bitcoin and twice the size of the entire cryptocurrency marketplace.

In other words, TIPS have become a big deal. And why not? Before TIPS, there were no securities designed specifically to combat inflation. Investors could cobble together accidental inflation hedges, such as gold, energy stocks, or perhaps real estate—assets that might peripherally benefit from higher prices or at least suffer less damage than mainstream securities, but which were not directly connected to changes in the Consumer Price Index. TIPS are. When the CPI rises, the Treasury raises the principal value of all TIPS by that amount.

Inflation Arrives

Until very recently, TIPS’ insurance policy went unused. For the 24 years from January 1997 through January 2021, the annualized rate of increase in the CPI was a mere 2.09%. For all practical purposes, inflation was not an investment danger. Holding 30-day Treasury bills would have nearly matched the inflation rate, earning an annualized 1.99%, and owning anything even slightly bolder would have exceeded it. TIPS were useful in theory but unnecessary in practice.

Then came inflation’s resurgence, in spring 2021. The financial markets were initially skeptical that inflation would persist; despite the CPI’s spike, stocks maintained their rally through the remainder of 2021, while bonds held their own. In fact, the yield on a conventional 10-year Treasury note was lower on Dec. 31, 2021, than it was on April 12 of that year, which was the day before the Treasury announced the first of what would be many inflation shocks.

Everything changed with the new year. In January, both stock and bond prices plummeted, suffering a tandem decline that continues to this day. The reason: inflation that has far exceeded economists’ expectations, leading the Federal Reserve to hike interest rates much more sharply than expected. At long last, TIPS would have their moment! Their inflation protection would now show its value.

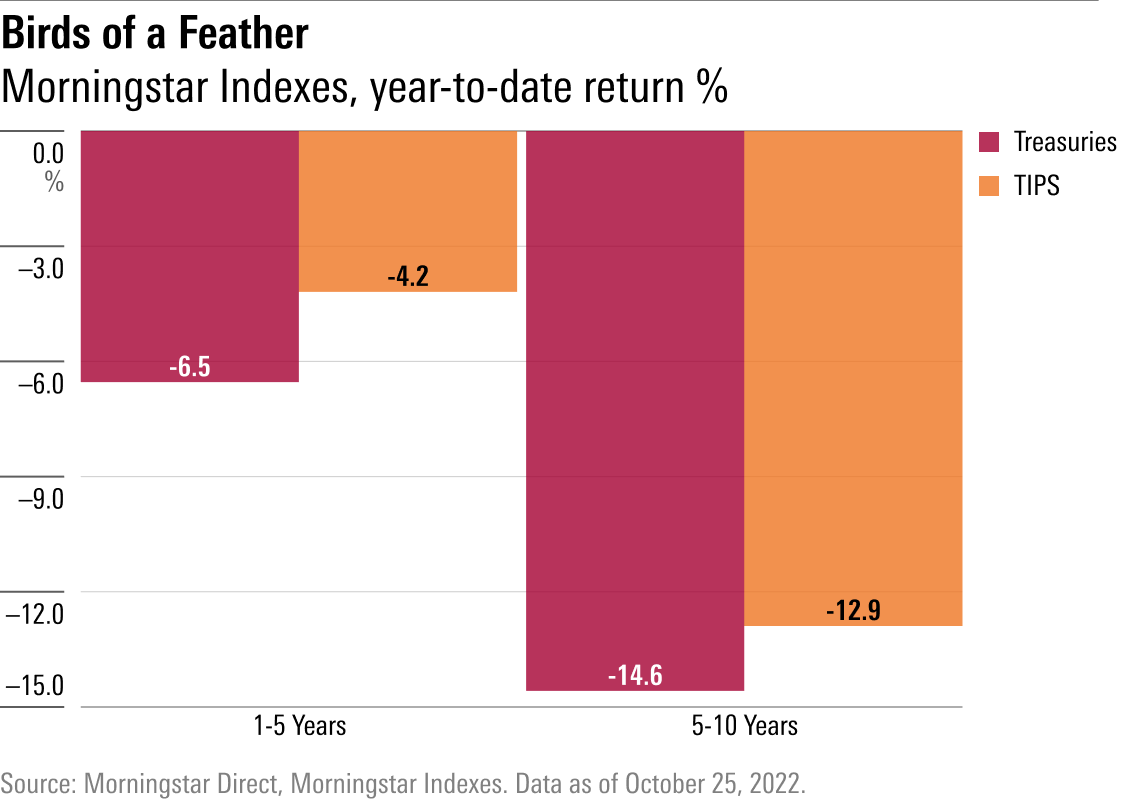

Not hardly. TIPS have performed disastrously, barely outdoing the traditional Treasuries that they were designed to thrash, should inflation appear.

What Happened?

The return on bonds can be decomposed into two components: 1) the inflation rate, and 2) that which remains, called the real yield. With a conventional bond, those two components are concealed, because the security is priced by a single statistic, its nominal yield. A bond that pays 4% may expect 3% future inflation, thereby delivering a 1% real yield; or it may forecast 2% inflation, with a 2% real yield. Any combination that sums to 4% will explain that security’s price.

With TIPS, however, the figures are explicit. Because all TIPS deliver exactly the inflation rate, one can use TIPS’ prices to compute their real yields. The result reveals the popularity of TIPS—the extent to which they are in fashion. A large real yield means that investors refuse to own TIPS unless they receive a much greater return than the level of future inflation. In contrast, a negative real yield indicates that buyers desire TIPS so strongly that they will give up purchasing power to own them. They are, to use the phrase of my colleague Paul Kaplan, the marketplace’s “willing losers.”

The latter, in fairness, is not strictly correct. If the real yield on TIPS becomes even more negative, then investors who own those securities can resell them at a profit. Unless one holds TIPS until they mature, their eventual total returns are uncertain, because the marketplace’s decisions will affect the outcome.

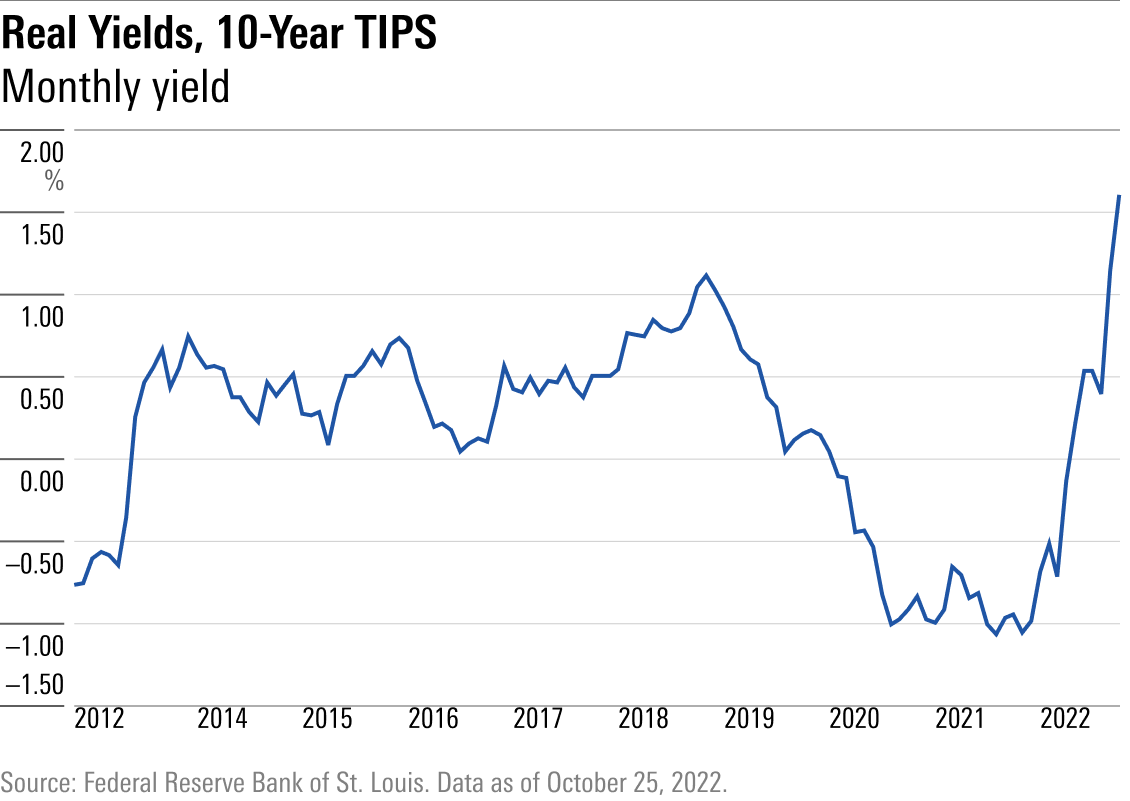

Which is exactly what happened—but in reverse. From spring 2020 through December 2021, TIPS had been abnormally costly, carrying their deepest negative yields ever. This year, that premium collapsed. Within nine months, TIPS went from being more expensive than any time during the past decade to being unquestionably cheaper. The chart below shows the real yields for 10-year TIPS over the past decade; the story for the five- and 30-year versions is similar.

Caught Out

If it seems strange to you that securities designed to fight inflation would implode when first faced with that very event, join the crowd. Although investment professionals realized before the fact that market movements could disrupt the inflation protection offered by TIPS—as with this The New York Times article or Charles Schwab SCHW note —few (if any) expected this level of carnage. Quite the contrary. When CNBC spoke to several experts a year ago about “where to put your money during an inflation surge,” the consensus top response was ... TIPS.

The good investment news, of course, is that after suffering such heavy losses (particularly with 30-year TIPS, which have shed one third of their value this year) TIPS may have become a bargain. Next Tuesday’s column will explore whether that is so, or whether TIPS need to become cheaper yet to justify their purchase.

Appendix

Technically, as some writers have pointed out, TIPS respond to rising inflation expectations, as opposed to either rising inflation itself or higher interest rates. I dodged that discussion for two reasons. First, it is beside the point, which is that even those who made that distinction did not expect TIPS to flop so spectacularly. Second, while true, that argument fails to explain why TIPS have crashed. It requires one to believe that investors increased their inflation expectations last year, then have ratcheted them down in 2022. That seems highly unlikely.

At any rate, deciphering why TIPS have performed so badly is a topic for another, longer article. Suffice it to say here that they have.

.jpg)

{kind=link}