On Tuesday, Dec. 6, manager Fernando Santos benched his veteran forward, Cristiano Ronaldo, for Portugal’s round of 16 game with Switzerland in the 2022 World Cup. The two had recently scrapped. Also, it was the team’s fourth match in 13 days, and Ronaldo was 37 years old. He could use the rest.

To write that this choice made news is akin to stating that the Beatles were popular. Ronaldo is not only among the sport’s greatest-ever players, but he is also a world-class diva who attracts attention like sugar draws flies. (If Cleopatra and Maria Callas had somehow created a love child, Ronaldo would be he.) Across the world, save for the United States, the headlines blared.

The match proved remarkable. Portugal routed the Swiss, scoring six goals against a squad that had only conceded two goals in its previous three World Cup matches, including a bout with mighty Brazil. What’s more, Ronaldo’s replacement scored a hat trick. The upshot was obvious, concluded both fans and commentators. The team was better without Ronaldo. He should also sit for Portugal’s next game.

Manager Santos concurred. Ronaldo was watching again when Portugal faced minnow Morocco, which overcame steep odds by advancing to the World Cup quarterfinals. This time, the result was very different. Morocco held heavily favored Portugal scoreless, beating it 1-0. Hurrah in Rabat! Utter failure for the idea that Portuguese soccer improves without Ronaldo. (Indeed, his stand-in was replaced shortly after halftime.)

Naturally, my thoughts turned to the saga’s investment implications. (See, boss, I was WORKING!) Three aspects seemed particularly instructive.

Lesson #1: Wedded to Narratives

People need stories. Tales are the muscle and sinews that unite the bones of facts. However, it is easy to forget that narratives are inventions. They exist solely because we created them. While they can be useful guides, if pointed in the wrong direction they become dangerous distractions for people who wish to use them to make decisions. Narratives must constantly be challenged and tested.

Portuguese soccer fans thought otherwise. Before the match against Switzerland, most believed that benching Ronaldo made sense. After the team scored six goals in his absence, easily winning what had been expected to be a tight contest, the sentiment became nearly universal. Their opinions had been substantiated; Portugal had unlocked the secret to its success. (Such beliefs, of course, are universally held by fans, regardless of the sport or country of origin.)

It’s all too easy to behave similarly as an investor. (Believe me, I know.) Take recent events. When inflation resurfaced in spring 2021, professional economists expected that the problem would subside quickly. After all, that had been the long-standing pattern. Consequently, the economists shrugged off the summer and autumn reports, forecasting in December that 2022′s consumer inflation rate would be less than 3%. Oops.

Inflation hawks have fared no better. When the U.S. economy rebounded after the 2008 global financial crisis, hawks criticized the Federal Reserve’s policy of quantitative easing, which they said would surely spark inflation. For years, they issued stern warnings about bond prices. To no avail: The inflation wolves stayed home. Prices remained dormant for more than a decade, after which it was far too late to claim a forecasting victory.

Sometimes, repeating the same investment story signals inattention, not fortitude.

Lesson #2: The Single-Cause Fallacy

Sports fans prefer their arguments unadorned. When a team goes on a winning streak after hiring a new coach, credit that deed. If a squad missing a key player loses to an opponent that it had previously beaten, that player’s absence was the reason. And when Portugal suddenly exploded for six goals, in the very game in which Ronaldo was at long last benched, the explanation was obvious.

Investors are similar. When facing a barrage of information, they tend to simplify their analysis by seeking the key feature that dominates other considerations. Successful analysis, from this perspective, comes not from adjudicating through the mass of points and counterpoints, but instead by finding that critical factor. Doing so turns investment analysis into one-stop shopping.

The two mental processes are not exactly alike, however. Sports fans examine differences. They measure success or failure by what has occurred since the time of major change. In contrast, investors are likelier to emphasize similarities. What past investment era looks most like our current experiences?

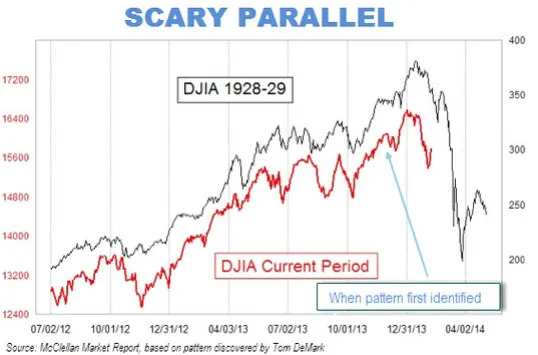

My favorite illustration of this mindset was a highly influential chart, which sadly I cannot locate on the internet, that purported to show how stock prices before and immediately after 1987′s Black Monday crash resembled those from 1929. The chart was prominently displayed in an article from The Wall Street Journal, and helped to convince many investors, both retail and professional, to steer clear of equities entering 1988. The stock market then rallied strongly.

(Although I could not find that chart, I did find a 2013 knockoff, which provides a flavor of the original.)

The same mindset occurs constantly with investment analysis. For example, many researchers now cite the 1970s as a useful guide, as that decade also featured an energy crisis and soaring inflation. What thrived then may also thrive today. That is a dicey bet. Investors may crave simplicity when making decisions, but the market harbors no such desires when setting its prices.

Those who do not learn history may be doomed to repeat it. So, however, might be those who apply its lessons too literally.

Lesson #3: Institutional Pressures

The final item, I grant, is speculation. I cannot read Fernando Santos’ mind. Nevertheless, I strongly suspect that he felt entering the Morocco game that his hand had been forced. Had Santos started Ronaldo, and had the game ended as it did in a 1-0 loss, he would have been vilified by those who knew that Portugal benefits from benching Ronaldo. Practically speaking, since the team had scored six goals under the new lineup, Santos could not use the previous version.

From such situations was born the adage, half a century ago, that professional investors “can’t get fired for buying IBM.” The meaning is clear: When managers must choose between a security that strikes outsiders as thoroughly sensible, and one that raises questions, it’s best to play it safe. If the security profits, the manager will be praised regardless. Should it fail, however, the manager will likely escape criticism for the former selection, while being assailed for the latter.

Individual investors face no such constraints. This, historically, has been their advantage over their professional counterparts. Institutional investors execute their trades at lower prices (no longer the case with equities), are supported by additional research, and devote more time to the endeavor. The sole advantage enjoyed by individual investors is freedom from institutional constraints—the ability to make decisions that are solely, completely, and entirely in the investor’s best interest, rather than perhaps also appealing to onlookers.

Whether that advantage can be gainfully employed is another matter. Rarely does the financial marketplace present a case as obvious as that of the Portuguese soccer team, when observers overwhelmingly believed the unlikely proposition that swapping a good old forward for a good young forward would transform the team. Investors, by and large, are more rational than sports fans. But institutional pressures do occasionally affect market prices. When they do, everyday investors can profit from the fact that they operate without outside scrutiny.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}