While U.S. Federal Reserve Chair Jerome Powell wouldn’t definitively say what the next step will be for monetary policy, we think the Fed is done raising rates after this meeting and is likely to shift to cutting rates starting in December of this year.

As widely anticipated, the Fed agreed on another 0.25-percentage-point increase in the federal-funds rate in its Wednesday meeting. Subsiding distress in the banking sector along with persistently above-normal inflation ensured that the Fed would push ahead with another hike.

With the latest hike this week, the federal-funds rate reaches a target range of 5.00%-5.25%, the highest rate since 2007. Altogether, the Fed has increased the federal-funds rate by over 5 percentage points since March 2022 in order to slow down the economy and thereby reduce inflation from historically high levels.

Now the attention turns to whether the Fed is done with hiking rates, and how long it might keep rates at current levels before ultimately cutting. The Fed’s press release removed last meeting’s language that “additional policy firming may be appropriate” to instead strike a more ambiguous tone. Fed projections call for a pause in rate hikes after Wednesday's meeting, in line with the market’s view. We think further hikes are not impossible but extremely unlikely.

A strong argument in favour of pausing is that the full effects of previous rate hikes have yet to be felt on the economy. While rate hikes have slowed activity in some rate-sensitive sectors like housing, that has yet to translate into net job losses in those sectors, but that will change in the coming year. And, while bank credit has still been expanding so far in 2023, lending is likely to contract greatly later in 2023 as banks respond to falling deposits and mounting concerns around financial health.

Finally, there is also a historical lag between economic activity and inflation, which means that slowing growth may not dent inflation right away.

Assessing the likely impact of these lagged effects of monetary tightening is fraught with uncertainty, which makes the Fed’s job very challenging.

Powell has stressed the need to remain “data-dependent” in its decision-making. Powell also declined to say exactly what outcomes in terms of the data would push the Fed to one decision or another its next few meetings. But we expect the Fed to refrain from further hikes so long as inflation doesn’t show signs of accelerating again.

When Will the Tide Change?

Assuming the Fed is done hiking, when will the Fed shift to cutting? Markets are now pricing in three rate cuts before the end of 2023, a shift in the market’s thinking that is also reflected in lower bond yields compared with two months ago. This shift occurred in response to rising concerns around the banks. However, we think the Fed will be able to contain banking system instability through liquidity injections, leaving it free to wield the federal-funds rate as a weapon in its war against inflation.

Indeed, deposit outflows from banks have been muted in recent weeks after massive outflows in early March. And deposit levels are still highly elevated above the prepandemic trend. Despite the failure of First Republic last week (marking the third major bank failure this year), the rest of the banking system looks broadly secure.

We expect the Fed to pivot to cutting rates once the battle against inflation is won. Powell stated that, contingent on the Fed’s inflation forecast playing out (with the year-over-year inflation rate hitting 3.3% at the end of this year), it won’t be ready to cut rates then. But we expect inflation to fall faster than this, which is why we think the Fed will be ready to cut rates in December 2023.

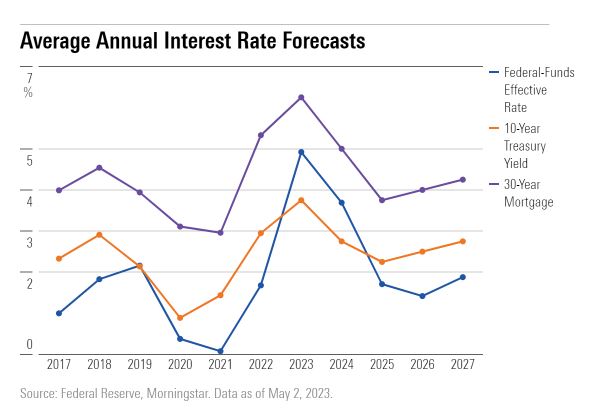

Moreover, we expect massive rate cuts in 2024 and 2025. Continued easing of inflation along with the need to stimulate economic growth will push the Fed toward hefty rate cuts, in our view. We project a federal-funds rate at the end of 2025 of 1.25%-1.50%, almost 2 percentage points below the Fed’s expectations.

For now, the markets are expecting the Fed to hold rates steady at the June meeting. According to the CME FedWatch Tool, which reflects bets by futures traders on the direction of interest rates, expectations are solidly for the fed-funds rate to stay at its new 5.00%-5.25% target.

.jpg)

.jpg)