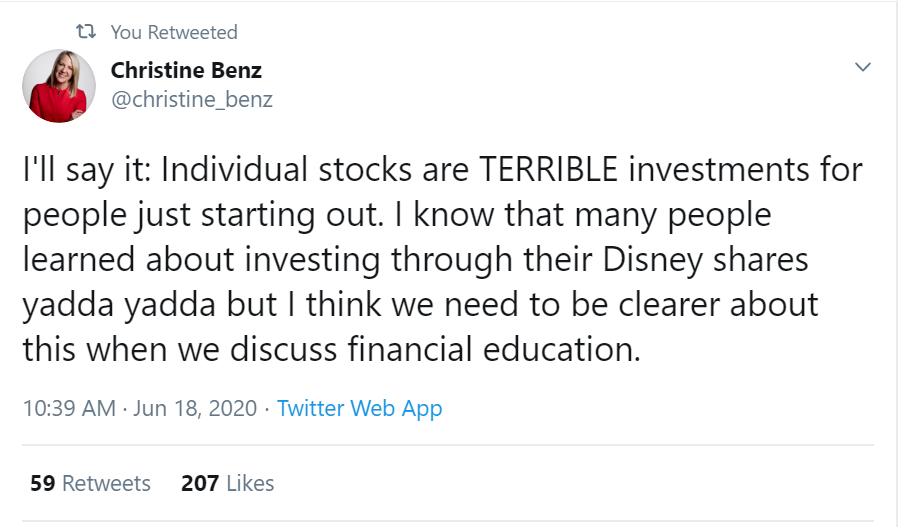

Recently, a Tweet by Christine Benz, our director of personal finance, generated a fair amount of conversation – and a little controversy. First, here’s the Tweet:

She’s absolutely right. If you’re just starting your investment journey, or even if you're at any other stage in your investment life cycle, it IS a terrible idea to put all of your money into a single stock. Remember the story about the girl who put all her eggs in one basket, and then tripped and fell, breaking and losing all of her eggs? There’s a reason you ‘Don’t put all your eggs into one basket’. And putting all of your savings into one stock is the same thing – but for investing.

To make sure you don’t lose ALL of your eggs if you trip and fall, you need to put your cache of eggs into different baskets. This process of dividing your savings or investable income or assets (the eggs, if you will) into different asset classes like stocks, bonds or real estate (these are the baskets – though there are more than these) is called ‘diversification’. Diversification is critical for long term investment success, and to ensure the safety of your portfolio.

Investing’s Free Lunch

Morningstar Canada’s director of research Paul Kaplan called diversification the one "free lunch" in investing because by diversifying, investors can reduce risk and possibly improve performance.

“Imagine that a portfolio's return fluctuated between -15% and 25% so that the average return is 5%. Over time, the compound rate of return will be about 3.1%. Now suppose that through diversification, it was possible to create a portfolio with returns that fluctuate between -5% and 15%. The average return of this portfolio is also 5%, but the compound rate of return will be about 4.5%. This illustrates the mathematical truism that if two portfolios have the same average return, the one with lower volatility will outperform. Hence, any opportunity to reduce volatility without reducing average return should be taken,” Kaplan explains.

Put another way, if you spread your assets into different asset classes, you reduce volatility. This is because different asset classes and different markets do not move in lock-step. For example, when stocks go up, typically, bonds would go down. So by diversifying into different asset classes, even if one portion of your portfolio falls, the others are there to prop it up.

“Just look at the past three major market corrections in Canada excluding the pandemic (tech bubble, Asian currency crisis, and the financial crisis). During these extreme market events, equity funds fell the hardest, bonds fell the least, and allocation funds (those that held a mix of stocks and bonds) were somewhere in between,” points out Ian Tam, Morningstar Canada’s director of investment research.

Where Should You Invest?

With thousands of individual stocks, mutual funds and exchange-traded funds, the task of deciding where and how to invest can seem daunting, but Benz urges investors to resist the urge to overcomplicate and/or to venture into overly narrow investment types.

“Instead, focus on low-cost, broadly diversified investments. For investors just starting out, target-date mutual funds can take the mystery out of the investment process: These funds employ aggressive, stock-heavy postures when investors are in their 20s, 30s and 40s, then gradually become more conservative as retirement draws close.

If you don't want to delegate control of your portfolio's stock/bond/cash mix and investment selection, a simple way to put together a well-diversified portfolio is to employ index exchange-traded funds. Such funds track a segment of the market, such as the S&P/TSX Composite Index, rather than trying to beat it. That may sound uninspired -- and uninspiring. But broad-market index funds often have the virtue of very low costs, which can give them a leg up on actively managed funds over time. If you do opt for actively managed funds for all or a part of your portfolio, low fees should still be a key priority,” Benz notes.

Investors sometimes think that owning multiple of the same funds is the way to diversify. But that is not true.

8 Equity Funds = Diversification?

We recently had an investor reach out with this comment:

I have more than a decade until retirement, and I agree that diversification is essential. That is why my portfolio is spread among eight equity funds!

The investor was pleased with his diversification, but the fact is, a greater number of funds does not mean you are diversified. His entire portfolio consists of only eight equity mutual funds, which means that all of his assets were in one asset class – equities. He is not fully diversified across different asset classes (stocks, bonds, cash, alternatives)

“You might also not be geographically diversified if all eight funds are invested in one region (for example, North America). An easy way to find out what your funds are holding is to have a look at the Morningstar Category they belong to. These are standardized fund categories for the Canadian market and will give you an idea of geographic exposure, asset class, and style of investment. If all of your funds are in one category, that is a good warning sign for you to consider diversifying your investments,” Tam says.

Easier Ways To Learn

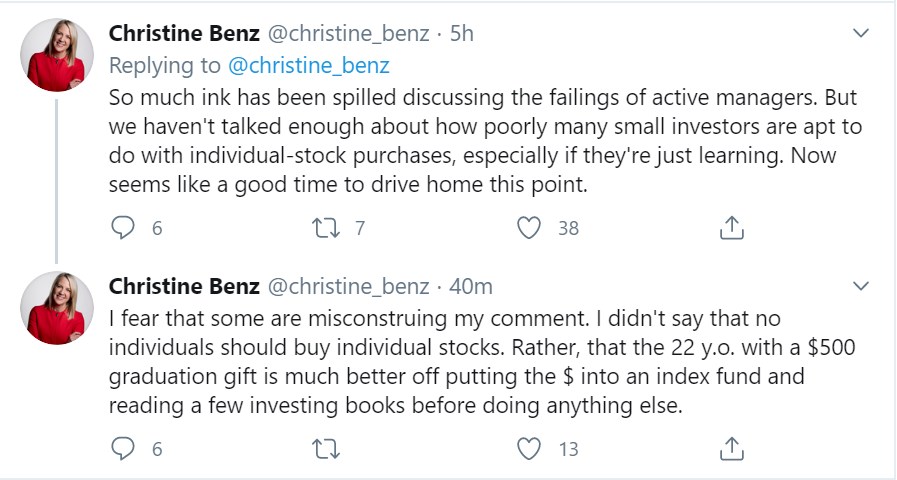

Going back to Benz’s tweet, she followed it up with two more.

The main counterpoint to her idea was that by investing in individual stocks, young investors learn valuable lessons, even if they fail. While it is always good to learn, there are easier and less costly ways to do so.

If you do want to invest in a single stock, do your homework. Understand why you’re investing in the stock, what the company does, what it’s growth plans are, how much money it has right now, how much money it will make, and also, crucially, if it makes sense for you to invest in the company at the current price.

If, after you understand all of this, and you understand the risks of investing in a single stock, you want to go ahead, then you’re making an informed decision. If you’re caught up in the excitement of something that everyone else is doing, it could be that you’re looking at a bubble.

Morningstar’s head of behavioural science, Stephen Wendel says an individual investor should arm oneself with a narrative, beforehand, to understand other people’s excitement. For example, much of that excitement may be because people feed off each other’s excitement, and that has little to do with the underlying fundamentals. That’s a valuation-driven narrative. But other – accurate – narratives could also work, from other investing philosophies, he says.

Wendel suggests two tools – externalizing and friction: “Externalizing means to thoughtfully write out your own personal investing rules, when you are in a calm state, and then use the written version to guide your day to day actions. This is a tool to avoid using your (malleable) intuitions and emotions in the moment. Friction is all about slowing you down: making it harder to act rashly in the moment, so that you might return to the issue with a calmer head.”

Passionate about investing in new ideas?

Explore the latest Global Thematic Fund Landscape report here