For those fortunate enough to keep a steady income by working from home as the coronavirus pandemic rips through the economy, a silver lining is that over the last few months, you may be saving more by spending less. For example, say you’ve not been able to get your daily XL double double from Timmies over three and a half months. You’ve saved around $170 after taxes. If you drink venti pikes from Starbucks, you’ve saved $240!

This combined with savings from not eating out, and temporarily eliminating the cost of daily transport to and from work may leave some lucky Canadians with a pleasant surprise in the bank. You might wonder, is a few hundred bucks enough to invest? Yes. It is!

In the past decade, the barriers of entry for investing have come down tremendously. The growth of the ETF market, proliferation of discount brokerages, the appearance of robo-advisors, all-in-one ETFs, and now commission-free trading have made low-cost investing much more accessible to the average Canadian.

So, assuming you only have $170 from your forgone caffeine money to invest, how do you do it?

Option 1: Robots!

Robo-advisors are automated advice platforms that invest your savings in a diversified set of low-cost passive ETFs based on your risk tolerance, as discovered through an online survey. These platforms are known for having easy on-boarding with small minimums and low ongoing management fees. Aside from having low fees, the products that are chosen on your behalf will be diversified and suited to your risk tolerance. As your financial situation and risk tolerance changes, so to does the portfolio’s allocation to stocks and bonds to align with your preferences.

At present, two robo-advice platforms that we know of are willing to fully invest your forgone caffeine money: WealthSimple (no minimum) and RBC Investease ($100 minimum). If you have been able to scrape together $1000 in savings over the pandemic, virtually any Canadian robo-advice platform will invest and manage your savings.

Pros: A very cost-efficient way to invest in a diversified portfolio suited to your risk tolerance.

Cons: By and large you will be invested in indices and hence, will get index-like returns.

Option 2: DIY Wealth

For those who prefer control over their own portfolio (and have the knowledge to get started), discount brokerages are aptly named for their reduced fees in placing trades within an investment account relative to full-service brokerages. 10 years ago, these brokerages charged upwards of $30 per transaction (buying or selling an investment) which at the time was still much cheaper than trading through a full-service broker. Since then, healthy competition has taken these fees down to less than ten dollars per trade. WealthSimple Trade goes further by advertising no commissions per trade with no account minimums, mirroring US firm Robinhood.

Pros: You will have full control over your trading and can choose between actively managed and passive index ETFs. By doing your own research and trading, you will not be charged fees for advice (although you will still have to pay the fees for the ETF to invest

Cons: As the do-it-yourself option, investing requires some homework, mainly understanding how much risk you are comfortable with, and picking an ETF that suits that level of risk tolerance. In Canada there are close to 1000 ETFs, plus another 2400 that trade in the US. A small subset of these are allocation ETFs (those that invest in a mix of stocks and bonds) which is well suited for DIY investors as most of these investments automatically re-balance the weighting between stocks and bonds so that you don’t have to (and hence save transaction costs).

Pro Tip: If this is your first time investing, consider setting up your account through a tax-shelter like a TFSA (Fax Free Savings Account) or an RRSP (Registered Retirement Savings Plan) to ensure you maximize the amount of wealth in your pocket.

Why do it?

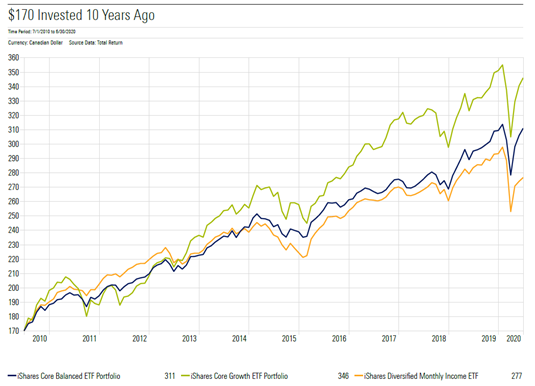

Even though $170 might seem like a drop in the bucket (after all, it’s coffee money), here’s what $170 looks like had it been invested 10 years ago in a selection of low-cost ETFs that invest in both stocks and bonds:

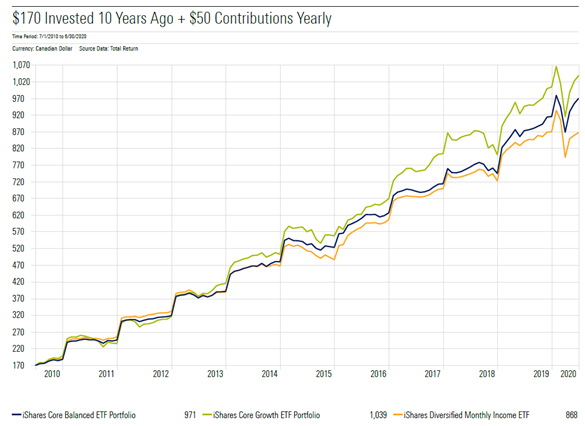

The problem with this chart is that investors couldn’t do this ten years ago with only $170, at least without first paying fees to open accounts, eating away at your starting amount. Technology, competition, and scale now allow many more Canadians to access investments with very little to start. Moreover, if a regular contribution is within your means, here’s what that might look like:

What not to do:

This article sums it up well. Online forums like reddit in combination with a commission-free trading account are a dangerous combination. Investing is distinctly different from day trading. Between having coffee and day-trading, I’d just have coffee.

This article does not constitute financial advice.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OSPGGQHXJVCGLBHR5CUUQWH3NQ.png)