Our view that the U.S. economy would experience a very strong long-run recovery from COVID-19 was far from clear earlier in the year, but it has become the consensus outlook, thanks to several months of strong economic data.

Two main threats have emerged to our optimistic thesis. First, investors are worried that additional stimulus won’t be forthcoming or that the November election outcome could have other negative consequences. However, we think the recovery should be in good shape even without additional stimulus. Vaccines are far more important to our economic view, and we remain optimistic that a successful vaccine will be deployed in the first half of 2021 and allow for a largely complete return to normal.

The other main threat is the coronavirus third wave, but we think economic activity should hold up fine as it did under the second wave of the summer. While parts of the economy won’t return to normal until we get a vaccine, the bulk of the U.S. economy has become fairly resilient to the virus.

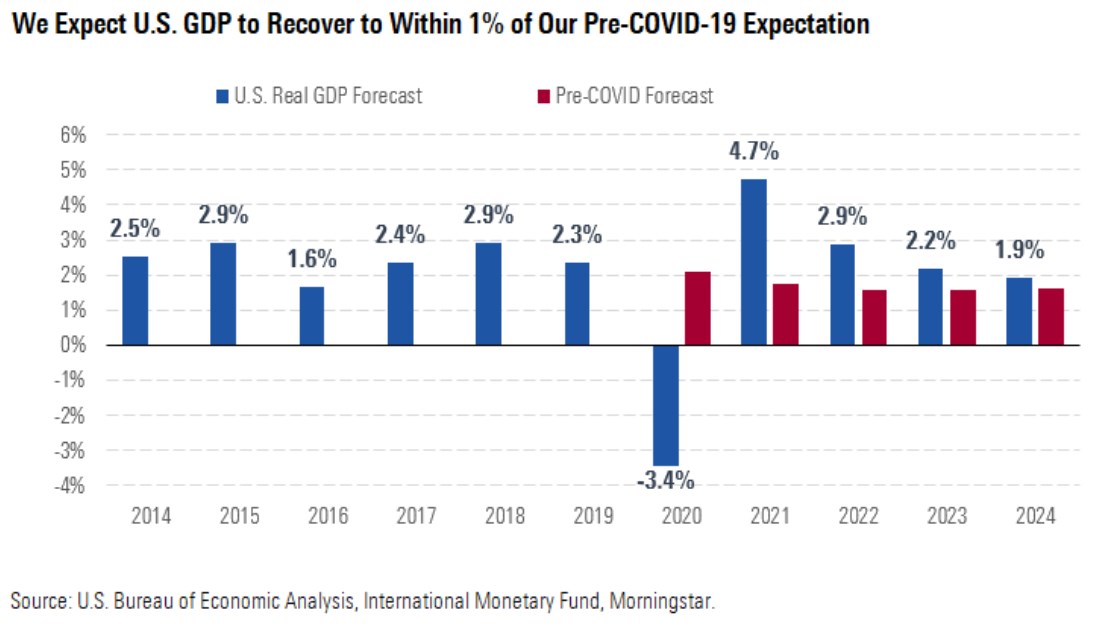

We expect U.S. GDP growth of negative 3.4% in 2020, about 550 basis points below our pre-COVID-19 expectation. This drop in GDP is much more severe than in the Great Recession nadir of 2009. Nevertheless, we expect strong catch-up growth in 2021 and the following years, such that U.S. GDP recovers to less than 1% below our pre-COVID-19 expectations. That’s a much better result than the Great Recession, which caused a lasting drag on U.S. GDP (around 10%-15% by the mid-2010s).

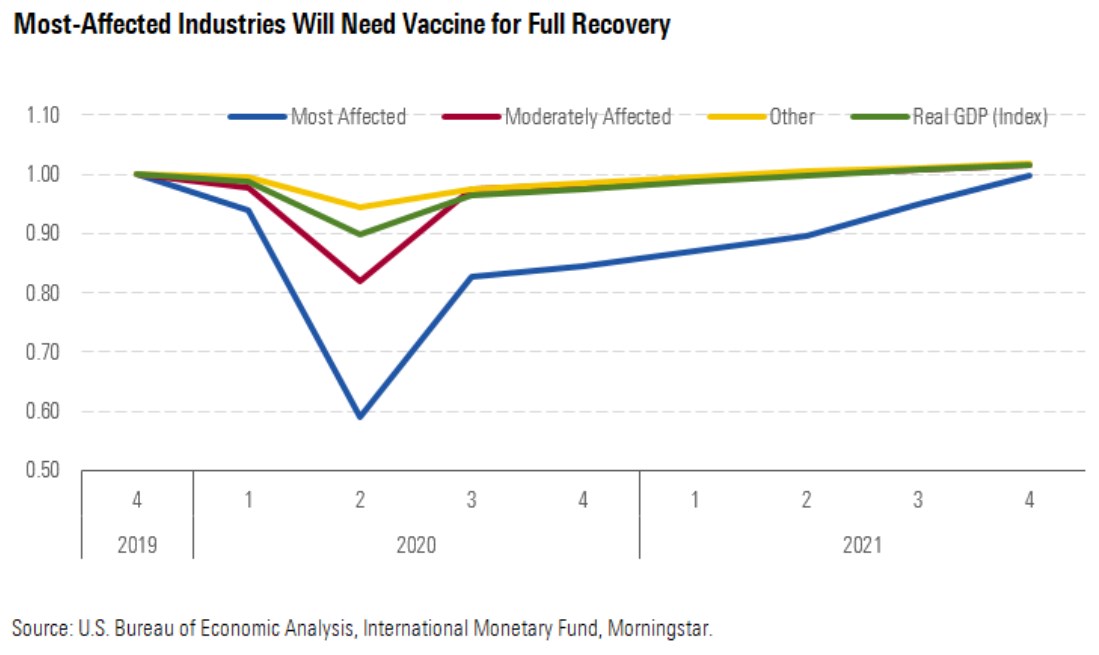

By our preliminary estimates, moderately affected industries (including retail and healthcare) have already bounced back sharply from second-quarter lows. The most-affected industries (including restaurants and hospitality) have also seen a strong recovery, though we expect that recovery to stall temporarily in coming quarters until the pandemic can be quashed by a vaccine.

Once a vaccine is widely deployed by mid-2021, we expect a near-complete recovery to occur even for the most-affected industries as people return to normal patterns of behavior. U.S. GDP should reach the fourth-quarter 2019 high-water mark by the third quarter of 2021.

We expect a strong recovery in labor markets, with unemployment falling to 4.9% by the end of 2021 (only slightly above the 3.5% level of the fourth quarter of 2019). As of the third quarter of 2020, employment was down 7% year over year, underperforming real GDP, which was down just 3% year over year. This is because the most-affected industries account for a much higher share of employment (15% of prepandemic levels) than they do of GDP (6%), reflecting lower output per worker for low-tech/low-wage industries like restaurants.

As these industries recover throughout 2021, we should see employment growth converge to GDP. This will also be important in ensuring that the demand side of the economy remains strong, as the low-income workers in these industries have a high propensity to consume and relatively little savings with which to maintain their spending in the absence of a job.

Resurgent Third-Quarter GDP Not a Surprise

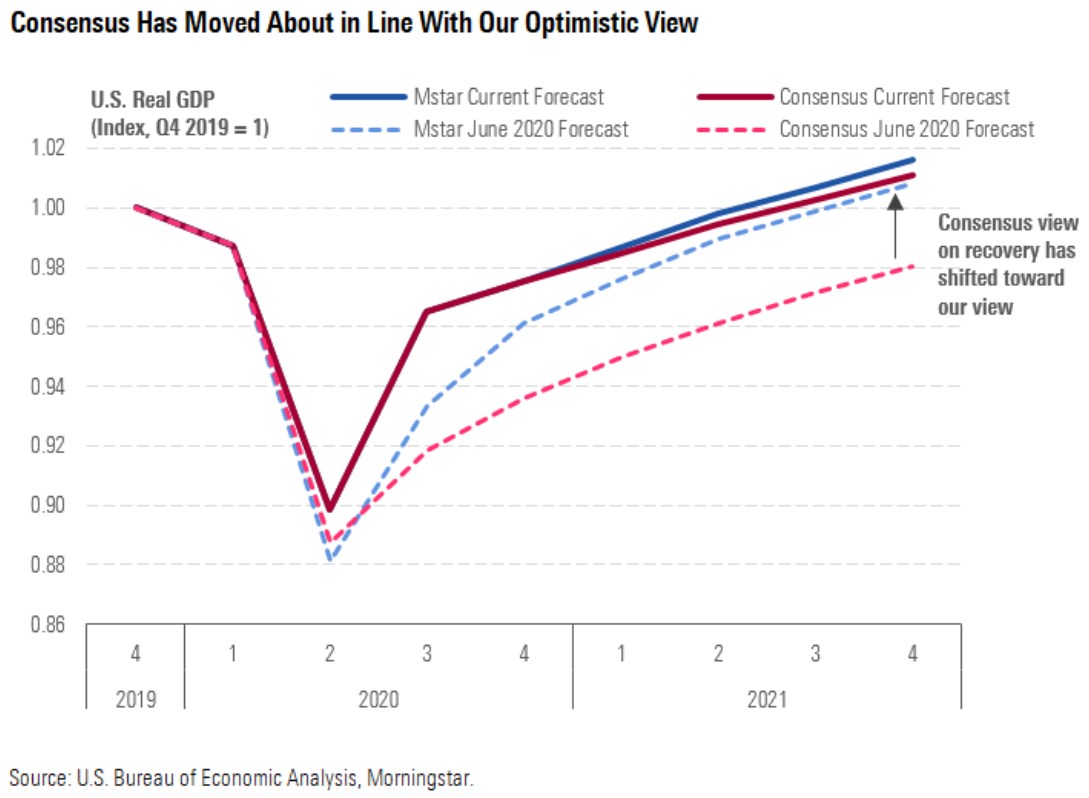

Well before the release of the strong third-quarter GDP numbers, consensus had moved much closer to our optimistic views on the recovery on the back of very strong monthly data. Even we have been surprised by the near-term strength of the recovery, but our 2021 GDP forecast is fairly close to our forecast of early June. Consensus, by contrast, has moved up its 2021 expectations by around 3% since June.

The news that U.S. real GDP surged 7.4% in the third quarter (33% on an annualized basis) was hardly a surprise, given that monthly data has given a good picture of the extent of the recovery for some time now. The recovery is far from over, however, with third-quarter GDP still down about 3.5% from fourth-quarter 2019 levels. Likewise, the monthly indicators still show a deficit as of September versus January levels.

From an expenditure perspective, the 2020 recession remains very unusual relative to historical recessions, reflecting the unique impact of the pandemic. As of the third quarter, real GDP was down 3% year over year, driven mostly by consumer services spending, which was down 7% year over year. This hit to services never happens in a typical recession. By comparison, at its nadir in the second quarter of 2009, services spending was down just 0.6% year over year. Consumer services expenditure accounts for roughly 70% of total personal consumption and nearly one half of U.S. GDP, so this accounts for why the short-term hit to GDP has been so severe during the pandemic.

By contrast, spending on consumer goods (especially on durables) typically weakens during a recession, but it’s been a major countervailing force in the current recession. In fact, consumer durable goods spending was up 13% year over year (nominal) in the third quarter, the strongest growth in any year--recession or not--since 1986.

Coronavirus Third Wave Won’t Sink Recovery

A third wave of coronavirus cases has surged in recent weeks, with the seven-day average for new cases rising from about 43,000 per day on Sept. 30 to 75,000 as of Oct. 28. However, we don’t think the United States’ economic recovery is in jeopardy.

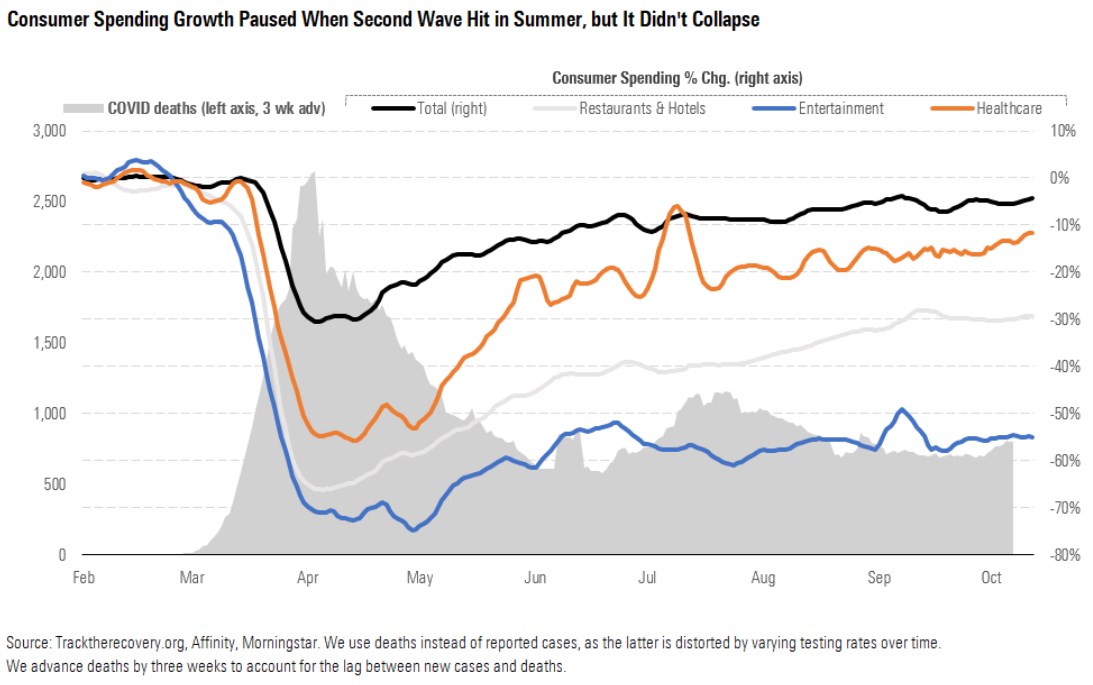

The second wave of the virus cresting in July caused a pause in the recovery in consumer spending. But consumer spending certainly didn’t collapse; it remained far above the trough levels of April. Even restaurant and hotel spending remained stable. Only spending on live entertainment (a small part of overall consumer spending) slipped.

Likewise, so far in this third wave, consumer spending looks stable. At this point in the pandemic, people are learning how to continue much of their ordinary economic behavior while trimming their risk of getting infected (or at the very least, they are pushing risk down to a level they are comfortable with). For example, people are still mostly avoiding large events to about the same extent they did in April, as the risk of infection is very high. By contrast, many people have returned to eating in restaurants, where the risk is still significant but much lower than a large crowded event.

We don’t expect a full return to normal until the pandemic is decisively ended by a successful vaccine. Still, with consumer spending remaining stable and investment spending still improving, the economy should be in decent shape in the coming months even with a third wave. We don’t expect another wave of widespread shutdowns to occur, which would constrain broader economic activity, particularly as long as death counts remain well below the March/April wave.

The U.S. economy has adapted quite well to the temporary new normal created by the pandemic, helping to soften the economic blow. This means that it is now somewhat less sensitive to fluctuations in case rates than it was at the outset of the pandemic.

First, consumers have switched to consuming more goods and fewer services, as the former exposes them to less infection risk per unit of economic value. In particular, durable goods spending has surged. Third-quarter durable goods consumption was up 13% year over year, the highest quarterly increase since 1986. Second, within goods spending there’s been a shift from physical stores to e-commerce. Likewise, sales of groceries (including by general merchandise stores) are up as people cook more and eat at restaurants less.

These shifts in demand have been facilitated by large shifts in U.S. employment. Retailers that have seen strong demand have been able to hire new workers and expand capacity quickly. Supporting the e-commerce supply chain, employment in the courier and warehousing industries has picked up.

More Stimulus Probably Isn’t Necessary for Economic Recovery

Many are worried that the lack of further fiscal stimulus could starve the recovery. However, we don’t think this is a major threat to the long-run economic recovery.

In our base case, we do expect that more stimulus will be passed in 2021, irrespective of most scenarios for the election outcome. The one scenario in which stimulus is at serious risk is if Democratic candidate Joe Biden wins the presidency but the GOP wins the Senate. If the last episode of a Democratic presidency and GOP House is any indication (under Barack Obama from 2011 to 2017), then fiscal stimulus could be hard to come by. However, this scenario has a fairly low probability at this point (only 14%, per FiveThirtyEight as of Nov. 2).

In any case, we think additional stimulus would mainly pull forward growth rather than change the long-run trajectory of GDP. This is first because we think the economy will reach nearly prepandemic levels of slackness in the economy within the next few years. We forecast the employment/population ratio to reach about 60% by the fourth quarter of 2021, only slightly below the fourth-quarter 2019 level of 61%. Once the slack in the economy (the “output gap” in economic terminology) is gone, there isn’t room for stimulus to sustainably boost GDP.

There’s good reason to think that even without a new stimulus bill, the slack in the economy can be absorbed within the next several years. First, we expect a vaccine to be widely deployed in the U.S. by mid-2021. Once that occurs, we think most of the economy will return to normal fairly quickly.

Many of the remaining unemployed workers say their layoffs are temporary rather than permanent. Many of those reported as being temporarily laid off in April indeed came back to work. Furthermore, even some of those who were reported as having exited the labor force as of April have rejoined the ranks of the employed. In addition, just a few industries highly affected by COVID-19 (such as restaurants) have accounted for about 75% of total job losses as of September. Damage to the broader economy has been limited.

Our other reason for thinking that more stimulus isn’t critical is that it’s easy to underrate how much good has already been done by the stimulus passed so far in 2020. The U.S. federal deficit/GDP ratio hit 15% in fiscal 2020, up 1,000 basis points versus 2019. This is the largest peacetime increase in the deficit in U.S. history.

The fiscal stimulus provided a massive boost to personal aftertax incomes. Disposable personal income was still up 5.4% year over year in August after being up double digits in the second quarter. For full-year 2020, disposable personal income will likely be up around 6%, better than the 2019 increase of 3.7%. For comparison, for full-year 2009 amid the Great Recession, disposable personal income fell 0.3%.

Much of this boost to disposable income has been saved. At first, this surge in savings created concerns that the stimulus wasn’t achieving its desired effect of lifting spending and thereby the economy. We do think the stimulus boosted spending far higher than it would’ve been otherwise. Nevertheless, the savings windfall has left household balance sheets in good shape overall. This means that consumers will be primed to spend more once the need for social distancing lifts in 2021 with a successful vaccine.

This is even the case for lower-income individuals, based on some data. While much attention has focused on the fact that lower-income workers fared worse in terms of layoffs, there’s been less attention on the effect of the large transfers received by those individuals as part of the stimulus. Credit card delinquencies have actually fallen by around 30 basis points in 2020, according to the U.S. Federal Reserve, whereas they soared by nearly 300 basis points during the Great Recession. Likewise, several researchers found that poverty rates have fallen by around 150 basis points during the pandemic.

As far as the implications of policies other than fiscal stimulus that result from the November 2020 election outcome, we believe that even with a Biden win and the Democrats capturing a large Senate majority, policy changes are unlikely to be large enough to change our views for U.S. GDP. The plausible increases in revenue and spending proposed by Biden would not push the size of government up to unprecedented levels.

Vaccine Availability Key to Ending Pandemic

COVID-19 cases are rising this fall due to lack of compliance with masking and social distancing, less-than-ideal diagnostics and contract tracing, and efforts to reopen businesses and schools as cooler weather sets in in the Northern Hemisphere. In the U.S., we assume 287,000 deaths and about 20% of the population infected by the end of the year, which generally implies increased infection rates but slightly lower death rates, as infected patients skew younger and treatments improve.

Gilead’s (GILD) antiviral treatment remdesivir now has full Food and Drug Administration approval after a solid clinical study showed 30% improvement in recovery time and trend to mortality benefit in hospitalized patients, although efficacy here is still relatively modest. Generic steroid dexamethasone has also shown a reduction in deaths of 20% in later-stage patients, and oral antivirals are in the works at Merck (MRK) and Ridgeback. Some arthritis drugs like Eli Lilly’s (LLY) Olumiant and Roche’s (RHHBY) Actemra seem to have a small effect in tamping down any overreaction by the immune system, helping to keep patients off ventilators and improve recovery times slightly. Most promising among treatments are targeted antibodies; both Regeneron (REGN) and Lilly have filed for emergency use authorization of their antibodies, which show strong potential to improve recovery time among high-risk patients.

We continue to think vaccination will be a key part of ending the pandemic. The most advanced vaccine programs are the mRNA vaccines from Moderna (MRNA) and Pfizer/BioNTech (PFE)/(BNTX). We expect FDA reviews of the initial EUA (Emergency Use Authorization) applications to take a matter of weeks, allowing the first EUAs in December and several other potential EUAs in the first and second quarters of 2021, allowing for broad vaccination in the U.S. in the first half of next year. Assuming 70% of adults are vaccinated, at a 70% efficacy rate, that would mean half of the adult population would be protected. But some already have immunity from COVID-19 or potentially from other coronaviruses, so that should be enough to reach herd immunity.

We’ve assigned probabilities of approval to the programs that have reported phase 1 data from 50% to 70%, based on the strength of phase 1 data and experience with vaccine types, which we have a variety of, improving odds of some success. The RNA programs have led with solid data, partly due to rapid design and manufacturing, but the challenge here will be distribution, as they generally require a deep freeze to preserve the vaccine, and there are not yet any approved RNA vaccines. Adenovirus or viral vector vaccines have slightly more validated technology (like Johnson & Johnson’s (JNJ) Ebola vaccine) and are also quick to manufacture in large quantities; J&J’s one-dose vaccine that only requires refrigeration could be a huge advantage in terms of logistics. Vaccine developers have a lot of experience with antigen-based vaccines, and Novavax had strong phase 1 data; a booster allows the use of very small amounts of antigen, so this increases the dosages that could be available significantly.

We think safety so far looks solid. The six-week FDA hold on AstraZeneca’s (AZN) U.S. vaccine trial due to a case of transverse myelitis in one patient in the U.K. trial and J&J’s two-week voluntary study pause of its own trial due to an undisclosed serious medical event (reportedly a stroke ) have both come to an end, and trials have restarted. Regulators at the FDA and study investigators could not establish a link between either vaccine and the illnesses, although we note causation is also not ruled out. Overall, we’re encouraged by FDA guidelines requiring a median of two months of safety data since the patient’s final shot of a vaccine before a company can file for an EUA, since the vast majority of side effects are seen within six weeks of vaccination, and companies will need six months of safety data before full licensure.

How Exposed Is Your Equity?

Get The Global Makeup Of Equity Indexes With Our Free Tool Here

.jpg)