Easy-to-use financial rules of thumb have always captured public interest, whether they are presented in best-selling books, TV talk shows, or, most recently, short TikTok videos.

Easy-to-use financial rules of thumb have always captured public interest, whether they are presented in best-selling books, TV talk shows, or, most recently, short TikTok videos.

The allure of these shortcuts to financial health is understandable: The idea that the answers to complex financial decisions can be simplified into 10 words or less seems magical. Unfortunately, the research behind many of the most famous financial rules of thumb is not robust and, in some cases, nonexistent.

In our research, "Shortcuts or Dead Ends? The Relationships Between Rules of Thumb, Habits, and Financial Health," we took a closer look at popular examples of rules of thumb. Specifically, we examined which ones people use most often, which ones people deem important, and which ones have a positive relationship with financial well-being.

Digging Into Rules of Thumb

We ran a survey using a nationally representative sample to identify rules that people may use for their financial decisions. We also measured participants' financial well-being using the Consumer Financial Protection Bureau's Financial Well-Being Scale, a standard measure of financial health. Within the survey, we presented each participant with a list of common rules--which we collected from existing academic, industry, and internal research--pertaining to spending, saving, debt management, or investing. From there, we asked participants to rank the rules by how closely they followed them when making financial decisions.

We then analyzed the data to identify which rules people said they used, how often they used them, and whether there were associations between each rule's frequency of use and the individual's financial well-being. We also asked participants how easy and automatic it was for them to follow a particular rule, which helped us understand the role of habit formation when using rules.

In our full piece, we delved deeper into each of our findings, but here we'll focus on one key aspect: financial well-being.

How Financial Rules of Thumb Correlate With Financial Well-Being

Although correlation does not signify a causal relationship, this analysis helps us identify which rules that people with a higher level of financial well-being report using.

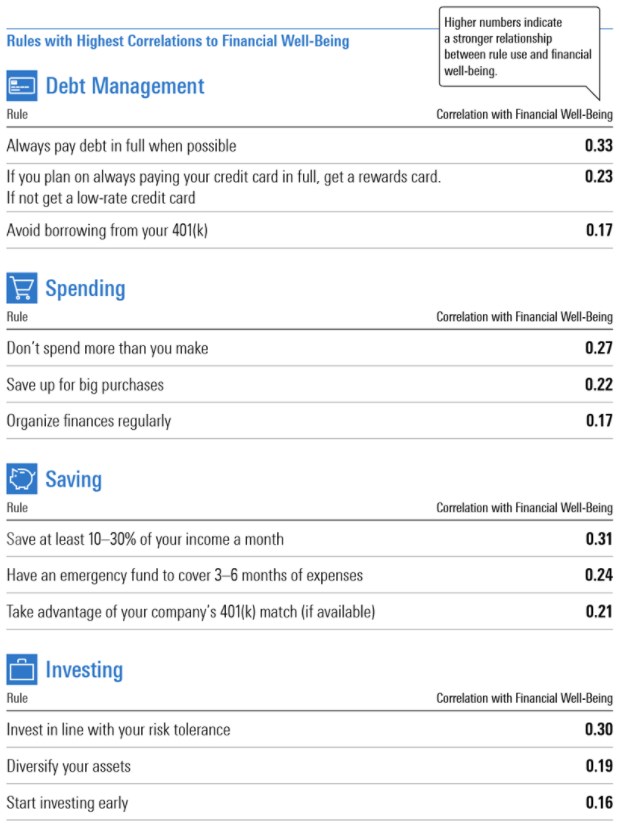

For this part of the analysis, we examined the correlation between the rankings of the different rules and participants' financial well-being score. The following table displays the rules for each topic that showed the strongest positive relationships with financial well-being, along with the strength of that relationship.

This analysis helps us begin to see which rules are associated with financial well-being, thus helping to sift through the myriad financial rules of thumb that many investors have at their disposal.

Consistency Is Key in Executing on Financial Rules of Thumb

Our analysis emphasized one clear, and seemingly obvious, point: A financial rule of thumb can only be effective if it is actually used.

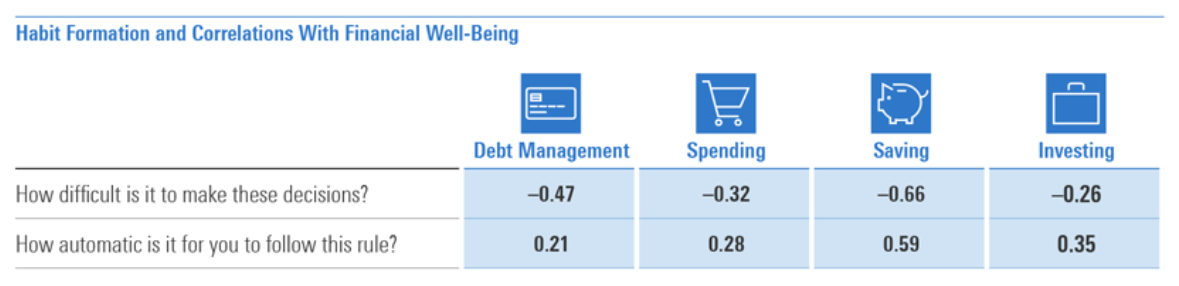

When we asked participants about the ease associated with using their top rule, we found negative correlations between how difficult they perceived practicing the rule to be and their financial well-being. In other words, the easier it was for a person to make these decisions, the more financially well-off they were.

Financial Rules of Thumb and Habits May Be Useful in Financial Decisions

Although it's always better to make informed financial decisions based on your personal situation, the truth is that we are human beings facing our own shortcomings and less-than-ideal situations. When making financial decisions, we may face an overwhelming number of options, unpredictable uncertainly, intense time pressure, or a lack of information. And the right financial rules of thumb can help us make an efficient and effective decision when we are in a pinch.

In our research, we found a few promising examples of rules of thumb that financially well-off people tend to use. Also, we found that although the particular rule you use is important, the most impactful thing you can do is to use your rule of thumb consistently.