When we hear stories about people making money on GameStop, or Bitcoin, or on BUZZ, it is a constant and understandable challenge to not question our own investment strategy. What was once a quick read of the investment section of a newspaper has now somehow morphed into a hyperactive bombardment of news constantly being pushed to our screen.

This said, seasoned investors know that that staying true to your investment discipline is often the best recipe for success, and for the most part, investors should steer clear of constantly changing their investment approach. Here’s why:

Morningstar’s Dr. Paul Kaplan and Dr. Maciej Kowara authored a paper outlining the number of “critical months” inherent in a fund’s historical performance. (Critical months are defined as months of a fund’s performance that, if they didn’t exist, would cause the fund to underperform their stated benchmark.) They found that investment returns are far from a straight line. Rather than posting a small gain each day, fund performance can often be ‘clumpy.’ Case in point, it was found that across global actively managed funds there was on average just 6 critical months of performance over a 15-year period spanning 2003-2018. If you are constantly changing investment strategies, it is likely that your fund selection will change as well. Changing funds too often is one way to assure that you miss these critical months of performance.

So when should you change your investment strategy?

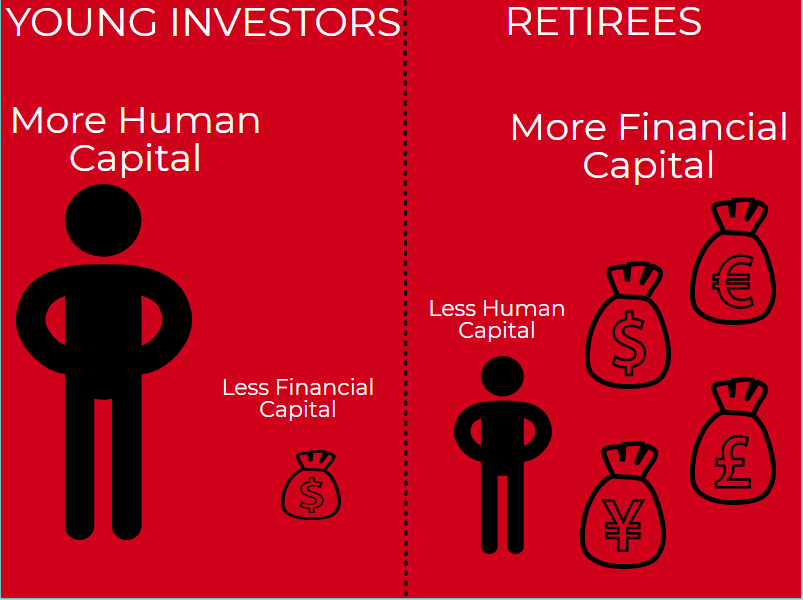

Human vs. Financial Capital

When defining your investment strategy, it is often worthwhile to think of two ‘sources’ of capital. The first is human capital, which is effectively your ability to earn money over time. The second is financial capital, which is how much actual money you have available to invest today.

Young investors have an abundance of human capital since it is likely that a young person has many income-earning years ahead of them. At the same time, young investors typically have very little financial capital. On the other end of the spectrum, retirees have very little human capital but an abundance of financial capital. When choosing an investment strategy, your risk capacity has lot to do with the sum of financial and human capital. The more capital you have (human or financial), the more risk you can afford to take.

There are stages in life when the balance between human and financial capital will change, and at this time, you could consider reviewing your investment strategy.

Here are some such life events (This is not a complete list, and all may not apply to every investor):

- Job Loss: When you lose your job, your potential human capital decreases. If this is a permanent change, your ability to withstand risk also reduces, and hence a revisit of your investment strategy to a more conservative approach may make sense.

- Addition of a Financial Dependent/s: If you are now tasked with taking care of a loved one financially, you may not have the same ability to withstand risk. Again, it may be worthwhile revisiting your investment strategy in favor or something more conservative.

- Recieving a Gift/Inheritance: If you receive a monetary gift or inheritance from a family member, your financial capital increases. The increase of capital here may warrant a more aggressive investment strategy, all things equal.

- Retirement: When you retire, you transition from capital accumulation to capital decumulation phase. This is a major event that definitely requires a look at your investment approach (likely transitioning to conservative income-producing investments to fund your retirement requirements).

Generally speaking, it is ill-advised to change your investment approach frequently. Although it is tempting to allow news and economic forecasts to drive your investment decisions, focusing on your risk capacity at a given point of time might be better indicator of when you should make strategic shifts in your investment approach. Experience tells us that a steady hand and patience are the keys to reaching financial goals.

This article does not constitute financial advice. It is always recommended to speak with a financial advisor or investment professional before making any changes to your investment strategy.