See more episodes of Quant Concepts here

Phil Dabo: Welcome to Quant Concepts working from home edition. ESG investing is a quickly evolving trend, with people particularly interested in all aspects of environmental, social and governance issues. Climate change is part of the environmental factors and will be one of the most economically impactful events in human history. Estimates of the costs of climate change have a wide range with a recent report by the Economist Intelligence Unit, estimating the net present value costs of climate change at $4.2 trillion. Inclusion and diversity is part of the social factor along with human rights and customer satisfaction. Corporate governance is the last factor of ESG, which incorporates business ownership structures, as well as the way that companies manage risks associated with the increasingly stringent regulatory environment.

Today, let's take a look at a strategy that focuses on companies that are reinvesting in their businesses, and leverages ESG research from Sustainalytics. As always, we're going to start by selecting our universe of stocks, which includes all 700 stocks in our Canadian database. Next, we're going to rank our stocks according to four key factors. The first factor is the trailing reinvestment rate, because we want companies that are trying to capture growth opportunities by putting money back into their businesses. The next factor is the industry median reinvestment rate for the next year. This is the forecast for the reinvestment rate for each industry to make sure that we're investing in sectors that are more growth oriented. The next factor is the three-year average return on equity, which is a performance metric that incorporates profitability, leverage and return on assets. The last factors are price to earnings ratio relative to earnings growth, which is a simple metric to make sure that we're not paying too much for the growth of the company's earnings.

Now that we have our stocks ranked from 1 to 700, we can start going through our screening process. We're only going to buy stocks that are ranked in the top 30th percentile of our list, and we want the company's controversy level to be zero. This is based on Sustainalytics assessment of over 35,000 sources to determine stakeholder impact, or reputational risk following events reported in the news. We want a healthy three-year average return on equity above 10%. And we want to eliminate most micro-cap stocks, so we've placed a market cap minimum of $270 million. I used the price change to 12-month high to capture companies that have good momentum. Our research shows that certain stocks that are trading close to their 12-month high tend to continue performing well and provide good downside protection. Our last buy rule is the ESG risk, which measures the company's exposure to ESG issues and the management of those issues. Here we want the company to have a score that is better than the median for all 700 stocks in our universe.

Now let's take a look at our sell rules which we've kept very simple. We're going to sell stocks if they deteriorate and fall to the bottom half of our list. We're also going to sell stocks if they become more controversial and have a score above zero. And our last sell rule is ESG risk, and we're going to sell stocks if the ESG risk deteriorates and falls to the bottom half of our list. Now let's take a look at performance. The benchmark that we use is the S&P/TSX Total Return Index. And we tested the strategy from June 2012 to July 2021. Over this time period, this strategy generated a very strong 20.3% return which is 10.7% higher than the index and with only a 31% annualised turnover.

We can see by looking at the annualised returns that this is a strategy that has beaten the benchmark over every significant time period, although it's done that with slightly higher price risk as you can see by the standard deviation, it also has superior risk adjusted returns, as you can see by the Sharpe ratio. It's also important to note that this strategy does have slightly lower beta which is a measure of market risk.

When looking at this performance chart we can see very good outperformance by the strategy over the past 10 years, and when looking at the up and downside capture ratio, we can see very strong performance from the strategy showing that the strategy outperforms the S&P/TSX most of the time when looking at a quarterly basis. So when looking at the overall market capture ratio, we are confident to see that this is a strategy that has performed well over the past 10 years. This is a great strategy to consider if you're interested in growth-oriented companies that are reinvesting in their business and are also good at managing ESG risks. The rules applied to the strategy are quite stringent to make sure that the companies on the buy list are good at managing ESG exposures. In addition to that, the strategy has had great performance particularly in 2015 during the energy crisis when the strategy outperformed the S&P/TSX by 19%.

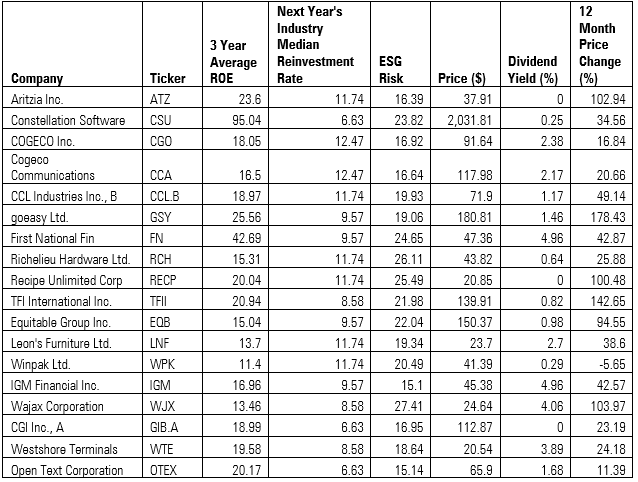

You can find the buy list along with the transcript of this video. For Morningstar I'm Phil Dabo.

{kind=link}