When it comes to equities, it’s not hard to make the case for global diversification to Canadian investors. Canadian stocks represent just 3% of global market capitalization. The market is heavy on the big banks and natural resources companies and light on healthcare and technology (beyond Shopify). Canadian equities have appreciated by less than half the level of the U.S. market over the past 10 years.

What about bonds? Investors unhappy with the current 1.5% yield to maturity on the Morningstar Canada Core Bond Index could be forgiven for looking abroad for bigger income streams. Emerging markets bonds offer far higher yields. But that boost comes with much more risk.

Developed market global exposure can also make sense within a high-quality fixed income allocation, as illustrated by a comparison of the Morningstar Canada Core Bond Index and the Morningstar Global ex-Canada Core Bond Index. Although enthusiasm about fixed income assets is hard to muster right now—to say the least—global bonds will continue to play an important long-term, strategic role in many investor portfolios.

Going Global with Fixed Income

Fundamentally, global bonds offer investors diversification across economies, interest-rate regimes, and inflationary environments. Whereas emerging markets bonds provide higher yields and a means of profiting from the growth of the developing world, they behave more like equities in terms of risk and reward. A Canadian who adds fixed income exposure to the U.S., Europe, and Japan is building out their “portfolio ballast.” Investors focused on volatility dampening will likely prefer their bond exposure hedged back into Canadian dollars.

At 0.66%, the Morningstar Global ex-Canada Core Bond Index has an even lower yield to maturity than the paltry income level offered by the Morningstar Canada Core Bond Index. This reflects the extent to which the pandemic-driven economic downturn and massive developed world governmental response have depressed yields across the globe. The Canadian bond market and its global counterparts have both become more sensitive to interest rates, as measured by their durations.

Comparing Canadian and Global Core Bonds

| Index | Average Coupon (%) | Yield to Maturity (%) | Terms of Maturity (Yrs) | Effective Duration (Yrs) | Credit Quality | Number of Constituents | Composition % | Country Exposure % |

| Morningstar Canada Core Bond | 2.59 | 1.46 | 10.76 | 8.26 | AA | 1,111 | Government: 35.1 Government-related: 46.7 Corporate: 18.2 | Canada: 97.23 U.S.: 1.48 |

| Morningstar Global ex-Canada Core Bond | 2.033 | 0.66 | 9.27 | 7.67 | AA | 16,462 | Government: 56.5 Government-related: 8.5 Corporate: 18.4 Securitized: 16.6 | U.S.: 43.12 Japan: 16.65 France: 6.60 U.K.: 6.20 Germany: 5.87 |

Source: Morningstar Indexes. Data as of July 31, 2021

The composition of the Canadian bond market deviates significantly, though, from other developed markets. The Canada Core Bond Index, which contains just a tiny fraction of the debt instruments present in the global index, provides exposure to just a single sovereign issuer. Aside from diversification across countries, the Global ex-Canada Index is more heavily weighted toward sovereign debt, driven by massive issuance by the governments of the U.S., Europe, and Japan in recent years. The Canadian index has significant exposure to government-guaranteed entities like the Canada Housing Trust, whereas the Global ex-Canada Index includes a large slug of securitized bonds, including mortgage-backed securities, covered bonds, and asset-backed securities, which aren’t present in the Canadian index.

So, an investor who wants their fixed income portfolio to reflect the opportunity set—the universe of investable securities—certainly has reason to look globally. The global ex-Canada bond index contains bonds from U.S. agencies like Fannie Mae and Freddie Mac, French and Australian government issues, bonds backed by Heathrow Airport and Toyota auto loans, and debt issued by such leading global companies as Siemens, Novartis, Pfizer, and Nomura.

A Canadian investor might view a global bond allocation as a kind of insurance against a national economic downturn—a housing market decline, a fall in natural resources prices, or some unforeseen shock.

What Do Global Bonds Add to a Portfolio?

To offer diversification benefit to a portfolio, assets shouldn’t move in lockstep. According to the 10-year Correlation Matrix below, stock and bond movements have diverged significantly. But Canadian stocks and bonds often move in the same direction as their global counterparts. The version of the Morningstar Global ex-Canada Core Bond Index that is hedged into Canadian dollars has a correlation coefficient of 0.81 with the Morningstar Canada Core Bond Index, which means the two benchmarks are more closely related than the global ex-Canada equities index and its Canadian equities counterpart.[1] But Canadian equities portfolios can be better diversified with global bonds, considering their lower correlation to Canadian equities, when comparing the hedged global bond index to Canadian Core Bond. And global bonds have been less correlated with global equities than Canadian bonds with Canadian equities.

Source: Morningstar Direct.

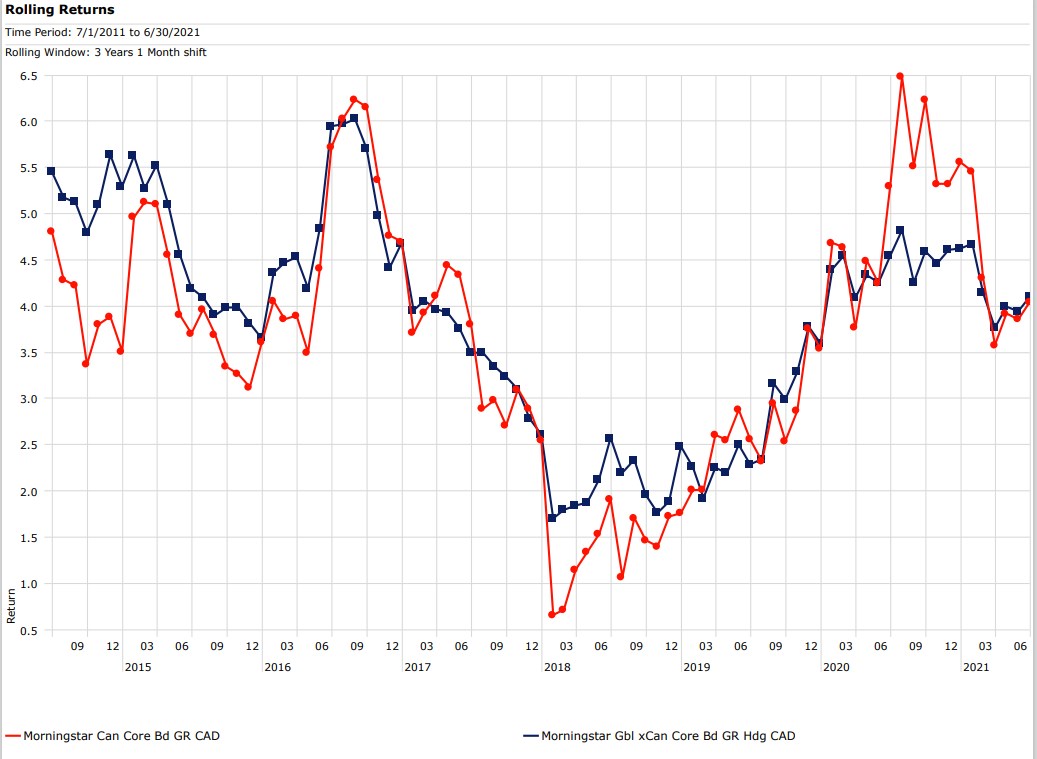

Correlation coefficients only reveal so much, though. First, correlations can change. Second, correlation captures the direction of movement, not magnitude. Looking at 3-year rolling returns over the past 10 years, there have been several periods during which Canadian bonds and global bonds have produced very different results. Canadian bonds posted superior performance in several periods ending in 2020, but global bonds had the advantage for many three-year windows ending in 2015 and 2018.

Source: Morningstar Direct.

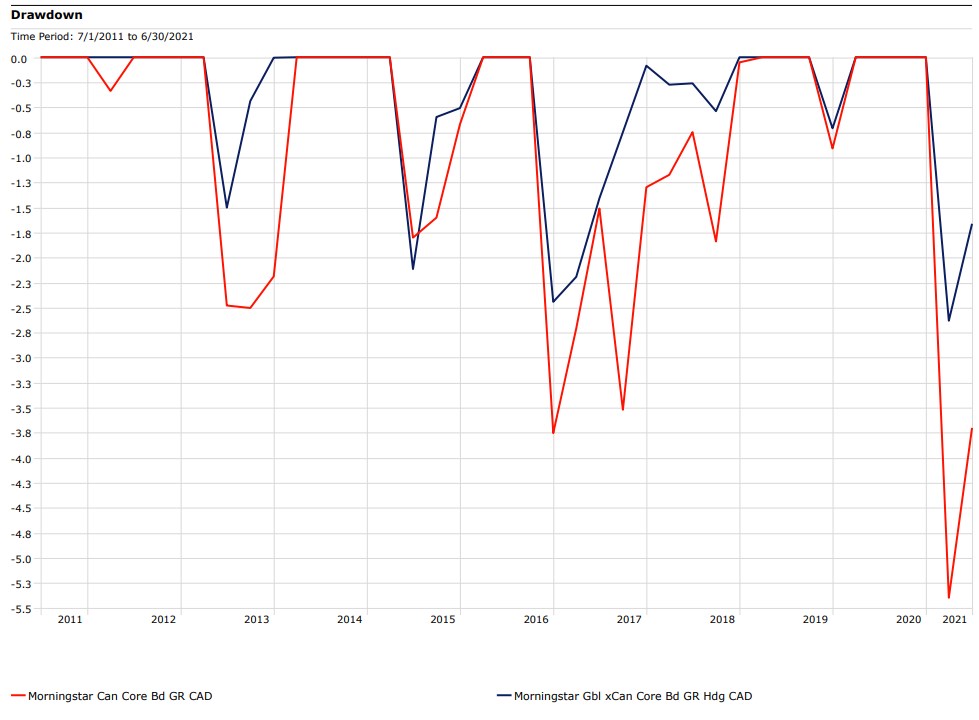

Focusing on down quarters within the past ten years, global bonds have typically lost less than their Canadian counterparts.

Source: Morningstar Direct.

This is reflected in lower volatility statistics for global bonds. The Morningstar Canada Core Bond Index has a standard deviation of returns of 4.2 over the trailing 10-year period through mid-2021, while the Morningstar Global ex-Canada Core Bond Index has produced a standard deviation of just 2.7. It’s not surprising that a global bond portfolio, diversified across more than 15,000 securities and dozens of markets, provides a smoother ride than a more focused, single country index.

Lower volatility and downside protection are key attractions. After all, bonds aren’t just for income. They also diversify equity market risk, dampen portfolio volatility, and preserve capital. They are especially useful for risk-averse investors, including those who have moved from the accumulation to decumulation stage of life.

The pattern of global bonds performing especially well during recent downturns parallels a longer-running trend. Ian Tam, Morningstar Canada's director of investment research, examined a series of equity market crashes over the past 25 years using Morningstar mutual fund category averages. He observed that global bonds produced better returns than Canadian bonds during three equity market crashes—the Asian Currency Crisis of 1998, the Technology Bubble burst of 2000-2002 and the Global Financial Crisis, 2008-2009. For example, Morningstar’s Global Fixed Income mutual fund category average return was 10% from April-August 1998, while the Global Equity category declined by 9% over that span, and the Canadian Fixed Income category was flat.

U.S. Treasuries can take a lot of the credit for this record. They are an especially popular safe haven asset during crises. When equity markets crash and correlations go to 1, panicky investors across the globe are comforted by the “full faith and credit” of the U.S. government.

For retirees who draw income from their portfolios, government bonds are critical. To quote noted author and financial adviser William Bernstein from Morningstar’s The Long View podcast:

“You invest in fixed income not for the return on your capital, but the return of your capital. If you have a Treasury bill that yields close to zero, in the long term, it still may be the highest-yielding asset, the highest-returning asset in your portfolio, because it is the asset that allows you to sleep at night and stay the course. And that's the real purpose. You're not looking for yield; you're looking for safety. And that's what those things provide.”

Why Would I Buy Bonds Right Now?

It’s hard to get excited about fixed income at this juncture. The yield on the 5-year Government of Canada bond was less than 0.90% in August 2021 while the 10-year U.S. Treasury hovered around 1.30%. These low current yields likely portend muted future bond returns. With inflation a real risk, interest rates seem much likelier to go up than down.

But a strong dose of humility is required when it comes to asset class forecasting. We were also told not to buy bonds in the wake of the Global Financial Crisis of 2008 when interest rates were rock-bottom and yields depressed. Yet the benchmark 10-Year U.S. Treasury hasn’t come anywhere near the 5% level it hit in 2007. Amidst declarations of “Bond Bubbles” and other dire warnings in the years following 2008, bond indexes appreciated. Both the Morningstar Canada Core Bond Index and the Morningstar Global ex-Canada Core Bond Index hedged into Canadian dollars returned roughly 4% on an average annual basis over the past 10 years through mid-2021. That’s modest compared to equity market returns, but not bad on an absolute basis. And it came during a period of low inflation.

Many bond market prognosticators have been confounded by the events of 2021. After yields shot up in the first quarter on the prospect of reopening societies, inflation, and a roaring economic recovery, expectations moderated in the second quarter. The Morningstar Canada Core Bond Index bounced back from its 5.4% loss in the first quarter to climb 1.8% in the second quarter. The global ex-Canada index gained 1.0% in the second quarter after falling 2.6% in the first three months of the year.

Yields could very well stay “lower for longer” if the pandemic drags on and the global economy stumbles along. The U.S. Federal Reserve appears to be in no rush to “taper” its bond purchases and raise rates, and as the old investment aphorism tells us: “Don’t fight the Fed.” Meanwhile, European bonds could benefit from “spread narrowing,” as continental integration brings yields on debt issued by countries like Italy and France closer to German levels.

Nowhere is it written that bond yields must revert to an historical mean. Yields in Japan and Europe have been low, even negative, for a very long time. The massive Baby Boom generation continues to enter retirement and global bond buyers seem to have an insatiable appetite, pushing yields down.

For investors who would rather not scrutinize yield curves, credit spreads, and default rates, sticking to a long-term strategic asset allocation diversified across various types of stocks and bonds alleviates the need to read tea leaves. Within a portfolio, some assets will always be zigging while other are zagging. A Canadian investor with a global portfolio is both open to greater opportunity and the full spectrum of diversification benefits.

[1] Though the indexes were launched in 2019, pre-inception returns have been modelled based on historical bond market data.