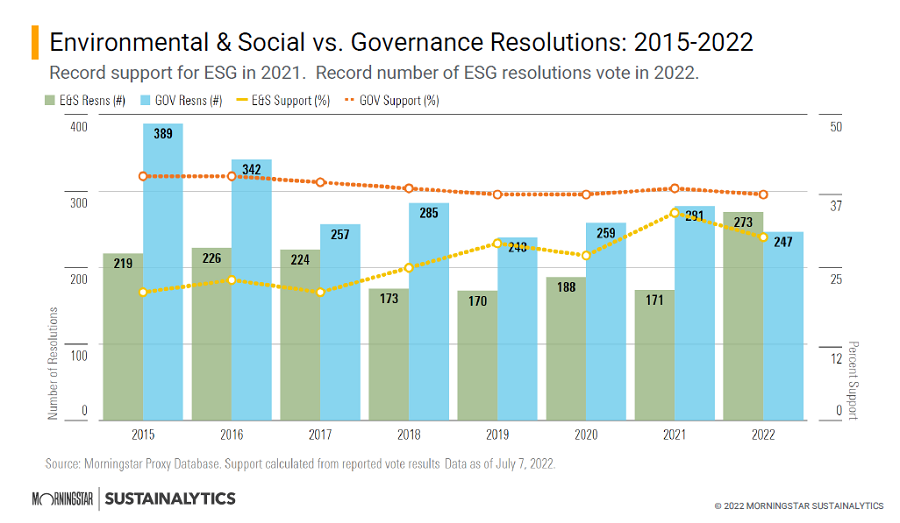

According to Morningstar's proxy database, the 2022 proxy season saw a record number of environmental, social, and governance resolutions head for vote. (Find out what proxy voting is here.)

This year also saw the rise of what we have been calling anti-ESG shareholder proposals. These proposals use various tactics to get on the ballot, many of which obfuscate the real intent behind them, and are usually submitted by groups that oppose the work of "pro-ESG" investors.

The anti-ESG movement has gotten a lot of attention this past year, particularly from prominent U.S. politicians. Some examples include former U.S. Vice President Mike Pence's op-ed in The Wall Street Journal, Florida Gov. Ron DeSantis' ESG financial fraud initiative, and Gov. Greg Abbott's anti-ESG bill in Texas. (My colleague Jon Hale offers a riposte to the anti-ESG movement in this recent commentary.)

“I see this anti-ESG push as the next extension of the ongoing culture war," says Morningstar ESG equity strategist Kristoffer Inton. "Many of these thoughts, and even some of the bills, are written without a great understanding of sustainable investing. Any investor that ignores ESG risk, like any other risk, does so at their own peril."

This anti-ESG push translated into more action on shareholder proposals—close to 50 such proposals were filed in this past proxy season. On the ground, however, most of these shareholder proposals failed to garner much support.

Anti-ESG Shareholder Proposals Fail to Get Support

Morningstar's proxy database has tracked 43 anti-ESG proposals filed by the National Legal and Policy Center, the National Center for Public Policy Research, and Steven J. Milloy during the 2022 proxy season. In the six months from January to June, proposals filed by these groups received only 7% support on average, and only 12 received over 5% support. In contrast, resolutions filed by other shareholders achieved an average of over 30% support across the board.

Part of the reason for the low levels of support could be that asset managers don't see anti-ESG issues as being relevant for shareholder value.

"Our recent research shows that large asset managers have come out strongly in favor of measures that seek to improve diversity, equity, and inclusion at the board level, senior management, and in the wider workforce," says Lindsey Stewart, director of investment stewardship research at Morningstar. "That includes those that haven't so far taken a particularly strong line on environmental issues like climate or biodiversity. As one U.S. top-five asset manager puts it: 'Our view is that diversity of perspective and thought—in the board room, in the management team and throughout the company—leads to better long term economic outcomes for companies.'

"So, we're seeing that these so-called 'anti-woke' proposals such as those requesting reporting on the impact of corporate DEI initiatives on groups with no history of socioeconomic exclusion—are getting almost no traction with voting shareholders."

To asset managers like pension funds, for example, there has to be a sound business reason to support or reject a proposal, and whatever the proposal is, it should benefit the long-term returns of the fund and be in the best interests of the beneficiary, so that the asset managers can fulfill their fiduciary duties.

Industry players who have been following these issues for years feel that many anti-ESG filings are frivolous and are filed with a sense of grievance, and this shows in the results.

"Businesses and investors care about what makes a difference on the bottom line," says Heidi Welsh, the founding executive director of the Sustainable Investments Institute. "If you cut out the political noise and look at facts on the ground, climate change is occurring, human capital management is an important competitive issue, and companies are managing for it and investors are paying attention to it. Those are the facts."

However, there are still 12 anti-ESG proposals that received significant support. Let's look at those in some detail.

Anti-ESG Shareholder Proposals That Earned Investor Support

Of the 12 anti-ESG shareholder proposals that received more than 5% support, 10 were filed by the National Legal and Policy Center, or NLPC. Four of these received more than 20% support, with one proposal at Twitter (TWTR) on lobbying disclosures, receiving over 40% support.

In many of the cases of the proposals that received good support, investors felt that the issues raised were legitimate governance issues or disclosure issues. Additionally, the request targeted a specific niche or question, and/or it attracted broader shareholder support. Put another way, as we have discussed in the past, many of the anti-ESG proposals found language and phrasing that the Securities and Exchange Commission finds acceptable by copying earlier approved pro-ESG proposals.

“Proposals filed by anti-ESG players can be characterized in two ways—original filings and those that have been duplicated based on previously filed proposals," Welsh says. "Original filings have little to no investor support. The issue gets a bit murkier when investors are faced with filings that mirror those passed or presented in previous years. The anti-ESG proposals began by mirroring proposals around lobbying and election spending but have gone on to copy votes around racial justice audits, and diversity, as well as some environmental-related proposals."

However, there is a third category of these filings, in which the proposals are original, garner wide support, and are usually centered around issues with less political disagreement. One such example was a proposal that got 36.8% support at Disney (DIS). The proposal was straightforward and addressed what it said it was addressing, which was one area on which pro-ESG groups and anti-ESG groups agree—forced labour in China.

The forced labour issue has financial and business-related implications, and both sides of the ESG debate want answers on how companies are addressing these risks. The Disney shareholder resolution filed by the NLPC asked that beginning in 2022, Disney report on the process of due diligence, if any, that the company undertakes in evaluating the human rights impacts of its business and associations with foreign entities, including foreign governments, their agencies, and private-sector intermediaries. The impetus for this request came from that fact that the film credits for Disney's 2020 live action film Mulan offered "special thanks" to eight Chinese government entities in Xinjiang province. Mulan was filmed in the Xinjiang region, where the Chinese government is persecuting the Uyghur people.

Despite the Filers' Values, Shareholders Focus on Value

Which brings us to the question of why some of these filings have been called disingenuous or insincere.

“It certainly has become more complex to assess which proposals are pro-ESG and which are anti-ESG," Stewart points out. "Stewardship professionals have gotten wise to the anti-ESG wing's practice of filing reasonably worded resolved clauses attached to highly controversial supporting statements—this is reflected in the low levels of support such proposals receive, often well below 5%. But it's a lot harder to deal with when the whole resolution appears reasonable, with the filer only revealing their true motivations in person at the meeting."

Here are two examples:

The first is from automaker General Motors' (GM) shareholder meeting in June. There was a shareholder resolution from the NLPC requesting disclosure on the risks of child labor in the electric vehicle battery supply chain. The wording of the resolution did not stand out as being particularly controversial. Many shareholders seemed to agree—the proposal got 22% support. However, the NLPC's comments at the GM shareholder meeting revealed the resolution to be merely a means of gaining the opportunity to air a heavily pro-fossil fuel diatribe in person.

The comments include, "Even with the benefit of millions of dollars in taxpayer subsidies, Chevy could not make the Volt popular. Now there is renewed fanaticism for electric vehicles from corporate management, the corporate media, and the failed Biden administration. But EVs are no more viable now than they were 10 years ago, despite the appearance. The only reason they have incrementally gained any popularity is because of the Biden administration's attacks on the oil and gas industry. Any product can gain popularity when the government inflicts blow after blow against its primary competition."

Another example is of Mondelez (MDLZ), the owner of brands like Oreo, Ritz, and Chips Ahoy. The NLPC filed a shareholder proposal that came up for vote at the 2022 annual general meeting. The ask was that the chair of the board of directors be an independent member of the board. The supporting statement said that “The chief executive officer of Mondelez International is also board chairman. We believe these roles—each with separate, different responsibilities that are critical to the health of a successful corporation—are greatly diminished when held by a singular company official, thus weakening its governance structure."

The ask, on paper, was reasonable, and many players, Morningstar Sustainalytics included, recommended that investors vote for the proposal. At the meeting, however, an NLPC member shared the firm's rationale behind the filing. You can hear the recording here.

Some of the statements made at the meeting included, "Public opinion polls shows dissatisfaction with big corporations is at an all-time high. People are fed up with the radical political agendas being forced down their throat by big companies. Corporate America has placed itself at odds with the economic and cultural interest of the American people."

What Should Shareholders Do About Anti-ESG Proposals?

Speaking privately, asset managers expressed dismay at the comments at the Mondelez meeting. However, as other investors point out, as unsavory as these tactics may be, when there are genuine disclosure or governance asks being made, the call for an investor who is looking at these from a fiduciary angle is to support.

At the height of proxy season, it can be challenging for investors and asset managers to pick apart the undertones of a resolution that appears on the surface to drive for greater transparency in charitable giving, or better governance, or more diversity but in reality serves to draw attention to a company's perceived support of "wokeness."

"All this shows a need for vigilance on the part of shareholders to examine the true intentions behind the proposals they intend to support," Stewart adds. "It's not always easy, but it's necessary."

What we can see from the numbers is that though there was some concern about an explosion, or at the least a rise, in these types of shareholder proposals, the reality is that most of these proposals did not garner much support. However, these proposals did receive a lot of attention, and perhaps that was the point.