:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SNOVSAXAZJHB3A726JIN3TBT2U.jpg)

At the start of this year’s proxy season, we looked at trends in climate-related resolutions globally. Because investors see a warming planet as a major investment risk, they are demanding better disclosure on what the risks are and how companies are taking action to mitigate them. A preliminary Morningstar study shows that the volume of climate resolutions remains high, but support has declined. In 2022, the volume of resolutions increased sharply versus the previous year, with most of the activity taking place in the United States. At the time, we also noted that shareholder support for climate resolutions was on a downward trend.

How about for 2023? We don’t yet have the full picture. However, analysing a limited selection of shareholder resolutions for companies in climate-exposed sectors gives us a pretty good indication of what’s going on.

The key takeaways we observed are:

- The high volume of climate-related resolutions in 2022 appears not to have been a one-off. There’s a similarly high number of resolutions in the 2023 proxy year.

- The declining trend in support for these resolutions in 2022 has continued this year.

Trends in the U.S. regarding the volume and level of support for climate resolutions differ from those in Canada and internationally. In a select number of industries, the number of U.S. climate resolutions surged; the volume of these proposals in Canada also increased. But amid the declining trend in support, climate-conscious investors will no doubt want to take extra care to ensure their fund manager is voting in line with their own environmental priorities. As our recent research on BlackRock, State Street and Vanguard shows, even managers running similar fund strategies can end up making very different proxy voting decisions.

Large Volume of Resolutions Continues into 2023

We will publish our detailed analysis of shareholder resolutions for 2023 later this year. But ahead of that, we took a look at climate-related shareholder resolutions in some key climate-exposed sectors: banking and insurance, energy and utilities, and materials. Our analysis captured proposals in the 2022 proxy year and the first 11 months of the 2023 proxy year in the U.S., Canada, and four other markets (Australia,France, Switzerland and the UK).

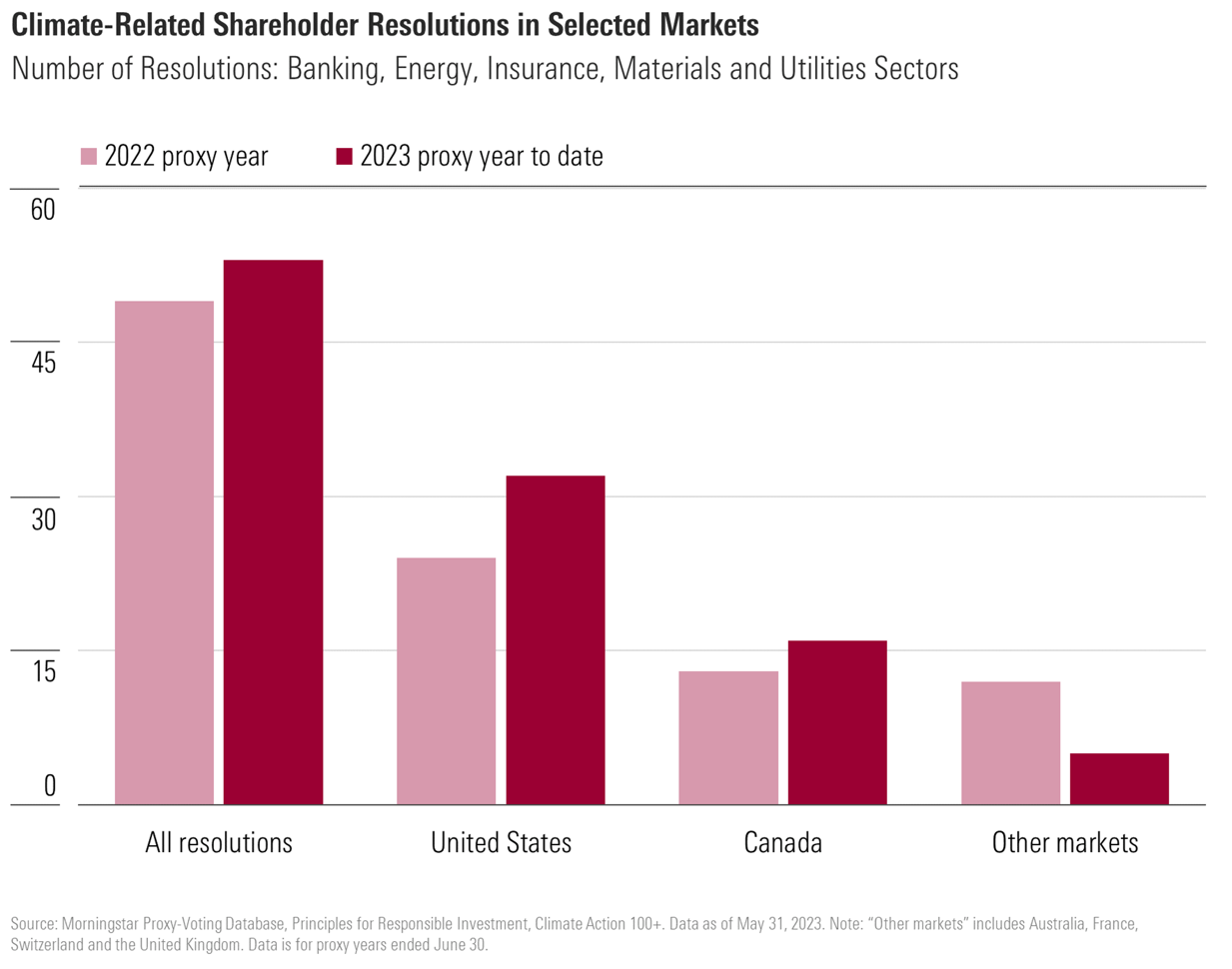

Number of Shareholder Resolutions on Climate in Five Key Sectors

Source: Morningstar Proxy-Voting Database, Principles for Responsible Investment, Climate Action 100+. Data as of May 31, 2023. Note: “Other markets” includes Australia, France, Switzerland and the United Kingdom. Data is for proxy years ended June 30.

For these sectors, we found that the number of climate-related shareholder resolutions in the first 11 months of the 2023 proxy year (53) already exceeded the total for the entire previous year (49), as shown on the chart above. This trend was led by the U.S., where 32 such resolutions were voted on in the 2023 proxy year to date, compared with 24 in the 2022 proxy year. In Canada, we counted 16 such resolutions in the 2023 proxy year to date, compared with 13 in 2022.

By contrast, in the other four markets, the volume of resolutions decreased (from 12 to five) over the same period. The increasing prevalence of management “say-on-climate” resolutions, which we discussed in our April preview, is likely to be a factor here.

Support for Climate-Related Resolutions Continues to Decline

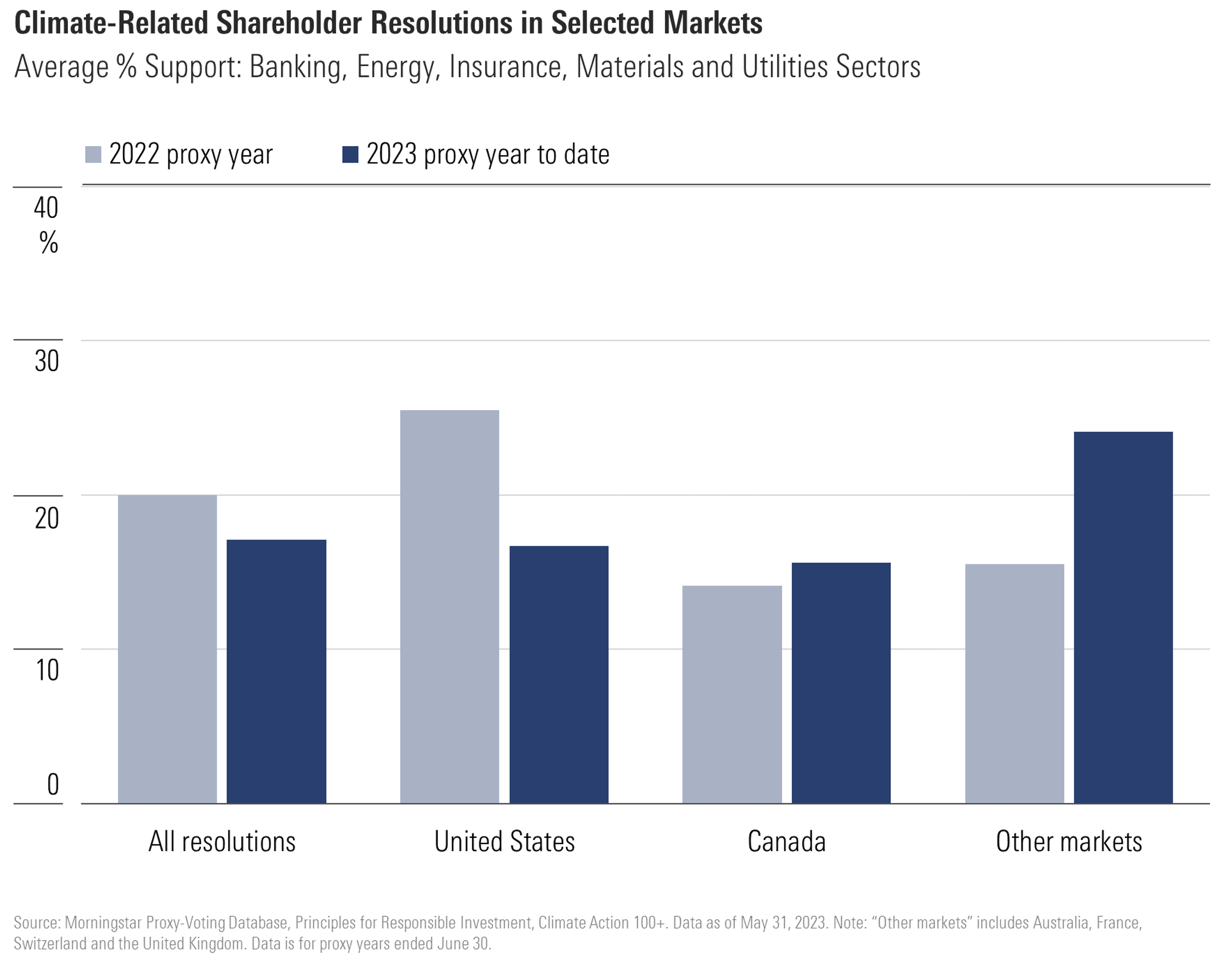

Looking at the level of shareholder support for these resolutions, we see the declining trend that we observed in 2022 continue into 2023, as shown on the chart below. Across all the resolutions in our analysis, average shareholder support fell from 20.0% in the 2022 proxy year, to 17.1% in the 2023 proxy year to date.

Average % Support for Shareholder Resolutions on Climate in Five Key Sectors

Source: Morningstar Proxy-Voting Database, Principles for Responsible Investment, Climate Action 100+. Data as of May 31, 2023. Note: “Other markets” includes Australia, France, Switzerland and the United Kingdom. Data is for proxy years ended June 30.

There was an increase in support for these resolutions in the non-U.S. markets we studied.

In Canada, a lower proportion of prescriptive resolutions in the 2023 proxy year compared with 2022 resulted in a slight increase in average shareholder support, from 14.1% to 15.6%. In the other four markets, the large increase in average shareholder support over the same period (from 15.5% to 24.%) is attributable to relatively strong backing from shareholders for proposals targeting a small number of highly climate-exposed companies (BP BP, Engie ENGI, Glencore GLEN, Shell SHEL, and TotalEnergies TTE).In contrast, for the resolutions filed at U.S. companies, average shareholder support fell by almost nine percentage points from 25.5% in the 2022 proxy year to 16.7% in 2023.

What’s Driving These Trends?

There’s a mix of different factors behind these trends. Amid the increased volume of resolutions in 2022, we observed that asset managers were reluctant to support many of the new shareholder proposals on environmental and social themes on the grounds that they were unduly prescriptive. With similar high volumes of proposals this year, it appears that this trend has continued.

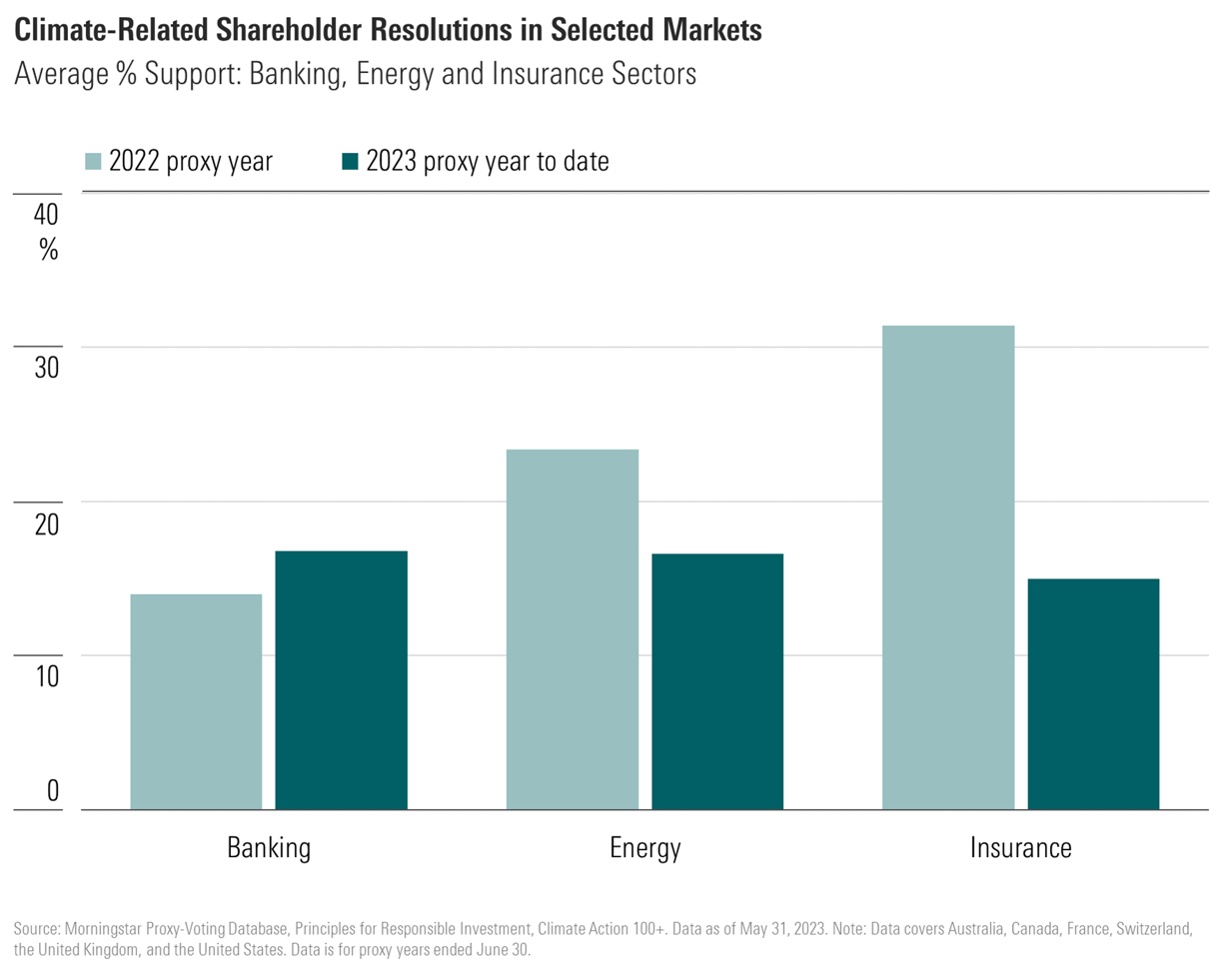

The chart below illustrates this in more detail. It shows average shareholder support for the climate resolutions we analysed in the banking, energy, and insurance sectors. These proposals make up 96 of the 102 resolutions we evaluated.

Average % Support for Shareholder Resolutions on Climate: Banking, Energy, and Insurance Sectors

Source: Morningstar Proxy-Voting Database, Principles for Responsible Investment, Climate Action 100+. Data as of May 31, 2023. Note: Data covers Australia, Canada, France, Switzerland, the U.K. and the U.S.. Data is for proxy years ended June 30.

Insurance Companies and Climate

The declining trend in shareholder support is most noticeable in the insurance sector. Here, most of the resolutions filed in 2023—at companies like Chubb CB, The Hartford HIG and Travelers TRV—demanded specific time-bound reductions in insurers’ fossil fuel underwriting businesses.

This was a step too far for many asset managers, some of whom believe such proposals ignore existing policies and seek to micromanage the company. One manager noted in its rationale for voting against one such proposal that these resolutions do “not take into account the company's existing policies or sufficiently allow for the nuances and complexities associated with the energy transition.” Another explained that “a vote to establish a timebound policy should remain within the discretion of management as it could have long term impacts on the core business model.”

Banks and Climate

There was a slight uptick in support for climate resolutions in the banking sector, where our analysis includes votes at several Canadian banks, including the Bank of Montreal BMO, the Bank of Nova Scotia BNS, CIBC CM, National Bank of Canada NA, Royal Bank of Canada RY, and Toronto-Dominion Bank TD. Several of the largest U.S. banks are also included. However, in 2023 the higher average support of 16.8% (compared with 14.0% in the 2022 proxy year) incorporates a mix of very different kinds of proposals.

Out of the 23 resolutions on climate in the banking sector that we analysed, 12 requested advisory votes or reporting on the banks’ climate policies and strategies. These 12 proposals gained the support of 22.9% of shareholders on average.

The other 11 resolutions in 2023 had much more specific asks and garnered only 10.1% support on average—roughly the same as for similar proposals in 2022. These included several calls to limit lending to new fossil fuel projects, similar to the proposals in the insurance sector mentioned above. Responding to one such resolution at JPMorgan, an asset manager commented: “The company has taken several steps to manage the climate transition, making the resolution onerous… Imposing a time bound request could impede management’s ability to exercise its strategy. As a result, a vote against is appropriate.”

Oil Companies and Climate

In the energy sector, average shareholder support for the climate resolutions we looked at fell from 23.4% in the 2022 proxy year to 16.6% in 2023.

There were several well-supported resolutions relating to energy companies’ climate strategy in 2022. That year, proposals requesting emissions targets, and reports on net zero impacts and climate scenario analysis at Chevron CVX, ConocoPhillips COP, ExxonMobil XOM, Phillips 66 PSX, and Valero Energy VLO all gained the support of over one third of shareholders. Following the relative success of those proposals, this year’s resolutions in the energy sector were narrower in focus and gained lower support.

Shareholder backing for new proposals addressing “Scope 3” greenhouse gas emissions (that is, emissions in a company’s value chain) varied widely and suggested a persisting divide between U.S. and European shareholders on this issue. Resolutions on Scope 3 emissions at U.S. companies Exxon and Chevron were supported by only 10% of those company’s shareholders. Meanwhile, similar resolutions at European companies BP, Shell and TotalEnergies respectively gained 16%, 20% and 30% shareholder support.

In Canada, a proposal at Suncor SU requesting reporting on capital expenditure alignment with greenhouse reduction targets received support close to the 2023 sector average, at 17.7%. There were also two resolutions at Imperial Oil IMO, requesting adoption of greenhouse gas reduction targets and reporting on the impact of energy transition on the company’s asset retirement obligations. Both proposals achieved similar levels of support if we exclude votes cast by insider shareholders (16.0% and 18.9% respectively, according to Climate Action 100+).

What Does This Mean for Investors?

If the trends on climate resolutions read across to broader environmental and social themes in 2023, then we’re likely to see higher volumes of more prescriptive and less well-supported resolutions this year when full data is available.

That likely means greater divergence between asset managers on the resolutions they are prepared to support. For investors, that means it will be all the more important to ensure good alignment between their own views and those of their asset manager. As always, we will continue to provide the analysis to help investors make that assessment over the coming months.