BlackBerry BB released its third quarter earnings report on Sept. 14, after the market close. Here’s Morningstar’s take on what to look for in BlackBerry’s earnings and stock.

Key Morningstar Metrics for BlackBerry Stock

- Fair Value Estimate: $6.60

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: None

- Morningstar Uncertainty Rating: Very High

What We Thought of BlackBerry’s Q3 Earnings

- BlackBerry has no economic moat.

- We like Blackberry's decision to split into two.

- The Blackberry stock is fundamentally undervalued, but has no immediate catalysts to push it up.

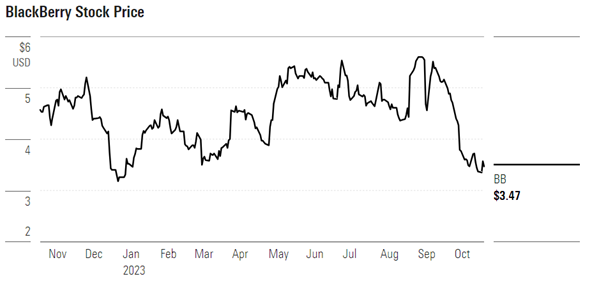

Source: Morningstar Direct. Data as of Oct 25,2023

Fair Value Estimate for BlackBerry Stock

With its 4-star rating, we believe BlackBerry’s stock is undervalued compared to our long-term fair value estimate. Our valuation implies a fiscal 2024 enterprise value/ sales ratio of 4 times and a USD to CAD conversion rate of 1.35, as of March 30, 2023.

We forecast compound annual revenue growth of 11% through fiscal 2028, with higher growth coming out of the firm’s Internet of Things business. We believe BlackBerry’s embedded software solutions for cars and industrial applications are strong and increasing software penetration in vehicles will drive growth. Moves from lower-value infotainment applications into higher-value autonomous driving and digital cockpit applications should lead to a large step function in content per vehicle.

We expect lower growth for BlackBerry’s cybersecurity business, where we believe execution is lacking. We expect the firm to lag cybersecurity competitors outside of its stronger position in regulated government customers.

We anticipate BlackBerry’s margins to improve with volume and improving value for its cybersecurity products. The company commits over 80% of sales to operating expenses, and we see this whittling down toward 70% in five years while BlackBerry keeps organic investment high to expand its customer base. Overall, we see fiscal 2028 non-GAAP operating margin reaching 17%, up from a depressed negative 14% in fiscal 2023 and -10% in fiscal 2022.

Read more about BlackBerry's fair value estimate

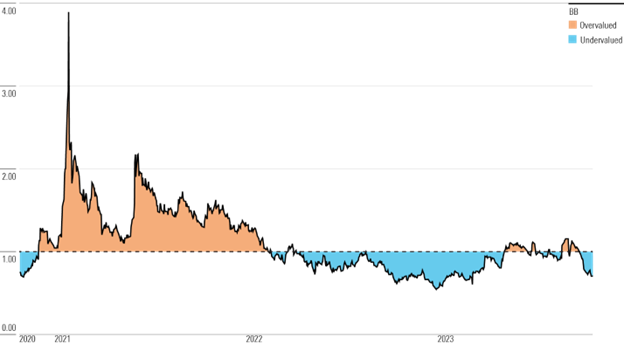

BlackBerry Stock’s Historical Price/Fair Value Ratio

Ratios over 1.00 indicate when the stock is overvalued, while ratios below 1.00 mean the stock is undervalued.

Source: Morningstar Direct. Data as of Oct 25, 2023

Blackberry Stock Economic Moat Rating

Its endpoint management, endpoint security, and embedded systems software solutions compete in highly fragmented markets. While these markets offer moats to larger competitors, we don’t believe BlackBerry’s solutions boast adequately competitive stickiness, and we view its negative historical returns on invested capital as evidence to our opinion. Thus, we do not have confidence it will earn returns in excess of its cost of capital over the next 10 years.

BlackBerry’s software and services segment comprises its flagship Spark suite and its embedded operating system, QNX. Spark combines unified endpoint management, or UEM, software with endpoint protection—what BlackBerry calls unified endpoint security.

While it is our view that switching costs occur frequently in enterprise software, given the time, cost, and effort involved in adopting a new solution and running two concurrent solutions simultaneously during the transition, we don’t think the Spark suite bears moatworthy switching costs. UEM’s selling point of a centralized solution for all devices presents low switching costs relative to other software that have longer implementation times and intertwine with more companywide operating procedures.

Competing with unique and best-of-breed services like CrowdStrike and the unmatchable breadth of Microsoft, BlackBerry is likely to struggle to keep old clients and win new ones, even with Cylance’s machine learning and AI detection abilities. Nevertheless, the UEM market is rapidly growing (with estimates ranging from 23% to 36% CAGR through 2024) and BlackBerry remains a leading player. While we anticipate healthy growth from BlackBerry’s enterprise software business, we think a relatively nascent, quickly growing market will attract many new entrants.

In the same segment, BlackBerry also sells its proprietary embedded software, QNX. We see some moatworthy characteristics of the QNX automotive business but don’t think the switching costs are steep enough to award a moat. BlackBerry must compete for every design win, even if it had sold into the prior model version. In infotainment specifically, as Apple CarPlay and Android Auto rise in popularity, automakers may find less reason to pay up for QNX in a new model over a free Linux alternative just to put the Apple or Android interface on top of it.

Read more about BlackBerry's moat ratings

Blackberry Stock Risk and Uncertainty

Since 2014, the firm has relied on M&A to pivot its business toward software. It encountered nine straight years of revenue decline, ending in 2020. BlackBerry’s ability to generate meaningful organic growth going forward will be paramount to its success.

BlackBerry competes in highly fragmented and competitive markets, against some of the largest companies out there. It may be difficult for BlackBerry to maintain or steal market share from companies such as Microsoft, IBM, and VMware with 10 or more times the revenue and R&D budget that it has. BlackBerry encounters the opposite problem with its QNX software, where it must compete with freely available Android and Linux operating systems. In these markets, it will need to continually innovate ahead of the competition to maintain pricing power, and thus market share, over these alternatives.

Finally, we think BlackBerry faces environmental, social, and governance, or ESG, risk, namely in the forms of human capital and data privacy and security. As a cybersecurity provider, any security breach of BlackBerry’s software could compromise sensitive customer data, or result in danger for cars and drivers operating with its QNX software. We think BlackBerry has established strong competencies in security that keep these risks at bay, but it must consistently stave off threats going forward.

Read more about BlackBerry's risk and uncertainty

Blackberry Stock Bulls Say

Blackberry Stock Bulls Say

- BlackBerry is the leader in embedded automotive software, with its solutions spanning most global OEMs and holding the highest security certifications.

- BlackBerry’s focus on security gives it an advantage in regulated industries, like government, healthcare, and financial services.

- BlackBerry IVY—the result of a partnership with Amazon Web Services—could create a revolutionary software ecosystem for connected vehicles, allowing OEMs to process, analyze, and monetize massive amounts of vehicle data.

Blackberry Stock Bears Say

Blackberry Stock Bears Say

- BlackBerry doesn’t have the scale, breadth, or name recognition to compete in enterprise software with giants like Microsoft and VMware.

- BlackBerry has been quickly losing share in a rapidly growing enterprise security market.

- BlackBerry has yet to prove its ability to grow organically as a software company.

-This article was compiled by Jitu A. Dribssa

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/2UWGQD7LCJCYNF3WQ5HHLP7UBE.jpg)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/F2S5UYTO5JG4FOO3S7LPAAIGO4.jpg)